ASC 606 Revenue Recognition: The Complete Guide

You're running a SaaS company, and your customers are signing up for your subscription-based service. So, when can you recognize that revenue in your books?

Is it as soon as the customer signs up for your service? When they actually start using it? Or once you've provided everything they paid for?

That's where ASC 606—the new(ish) revenue recognition accounting requirement—comes into play. It's the rulebook that ensures everyone's playing fair and square in the financial reporting world, maintaining credibility and transparency with investors and stakeholders.

Here, I'll explore the ins and outs of ASC 606. I'll address the challenges that SaaS companies face with revenue recognition and provide practical solutions to navigate through the complexities of FASB’s latest revenue recognition standard.

What is ASC 606?

Accounting Standards Codification Topic 606, also known as ASC 606, is an accounting principle that standardizes revenue recognition practices. It was jointly issued by the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) in 2014 to provide an industry-neutral approach to revenue recognition that removes complexity and increases financial statement comparability.

ASC 606 supersedes all existing revenue recognition guidance required under both US GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards).

This set of guidelines replaces ASC 605 (the old revenue recognition standard) and introduces a new five-step model companies can use to analyze revenue earned from the transfer of control of goods or services.

So, what does that actually mean? Well, if you're running a business that earns revenue from contracts with customers, ASC 606 sets out guidelines on when and how you should recognize revenue from those contracts. The standard was issued with the goal of giving financial statement users more information about the nature, value, timing, and uncertainty of revenue earned through customer contracts.

Why Should You Care About ASC 606?

ASC 606 is important because it ensures accurate and consistent revenue recognition. It brings transparency to financial reporting and provides stakeholders with reliable information about a company's revenue.

ASC 606 changes the game by introducing a more consistent and accurate approach to revenue recognition. The new revenue standard was dual-purpose. First, the new revenue recognition model fixes problems and confusion in the old rules about recognizing revenue. Then, it gives a stronger and better way to deal with revenue-related issues.

Also, it makes revenue recognition practices easier to compare between different companies, industries, countries, and markets. People who analyze financial statements will get more helpful information because of better disclosure requirements.

Finally, and most beneficially for you, ASC 606 ensures that companies will find it easier to prepare financial statements, as the number of rules you need to follow is reduced.

It requires companies to allocate revenue over the contract term, recognizing it over time as the customer receives access to and benefits from the product, service, or software. This aligns revenue recognition with the actual delivery of value and provides a more accurate representation of the company's financial performance.

Pause: Still With Me?

If you’re genuinely curious about ASC 606, keep reading. If you’re just here to make sure you won’t get fined by the government, you should be looking into financial reporting software instead. It knows everything about revenue recognition — so you don’t have to.

Obviously, the implications for SaaS companies are significant. With ASC 606, you must reassess your revenue recognition practices and reporting practices to ensure compliance with the new standard.

ASC 606 compliance also requires enhanced disclosures in financial statements to provide transparency regarding revenue recognition methods and the timing of revenue recognition.

Let's look at it this way: Say you run a software-as-a-service (SaaS) company, and your business model relies on you providing access to your software platform in exchange for a recurring fee.

Under the previous revenue recognition guidelines, you might have recognized revenue upfront when the customer signed the contract or made the first payment. This method could have led to an overstatement of revenue in the early stages of the contract, creating a mismatch between revenue recognition and the delivery of value to the customer.

A 2022 study by some academic researchers on the financial-reporting effects of ASC 606 adoptions found that adopting ASC 606 is associated with improved financial-statement comparability, informativeness, and mapping of revenue accruals to cash collections.

The researchers found software firms experienced significant improvements in liquidity after implementing ASC 606, which suggests that the new standard positively impacted financial statement comparability and informativeness.

The study also analyzed the impact of ASC 606 on revenue-recognition disclosure in firms' 10-K filings. It revealed that both software and electronic computer firms increased the quantity and quality of revenue recognition disclosure. Additionally, the comparability of revenue disclosure improved in both industries after the adoption of ASC 606.

Real-World Company Example

Adobe offers a notable example of ASC 606 implementation. Adobe offers cloud-based services through its "Creative Cloud" platform, which allows creative professionals to do all sorts of things, from designing websites and making videos to creating graphics and much more. Customers pay for these services on a subscription basis.

Adobe recognizes the revenue from these subscriptions over the period of the contract, which means they spread it out evenly over the time customers are using the service. So, if you sign up for a one-year subscription, they'll recognize the revenue gradually throughout that year.

But what makes it a bit more interesting is that the cloud-based services are tightly integrated with their on-premise and on-device software. Because of this tight integration, Adobe considers the whole package as one continuous performance obligation. In other words, they treat the cloud services and the software as a single, complete solution. So, the revenue from the Creative Cloud subscriptions is recognized gradually over the subscription period.

ASC 606 helps Adobe ensure they recognize revenue from their subscriptions in a fair and transparent way. By considering the integrated nature of their cloud services and software, they deliver on their promise of an outstanding creative experience for all their customers.

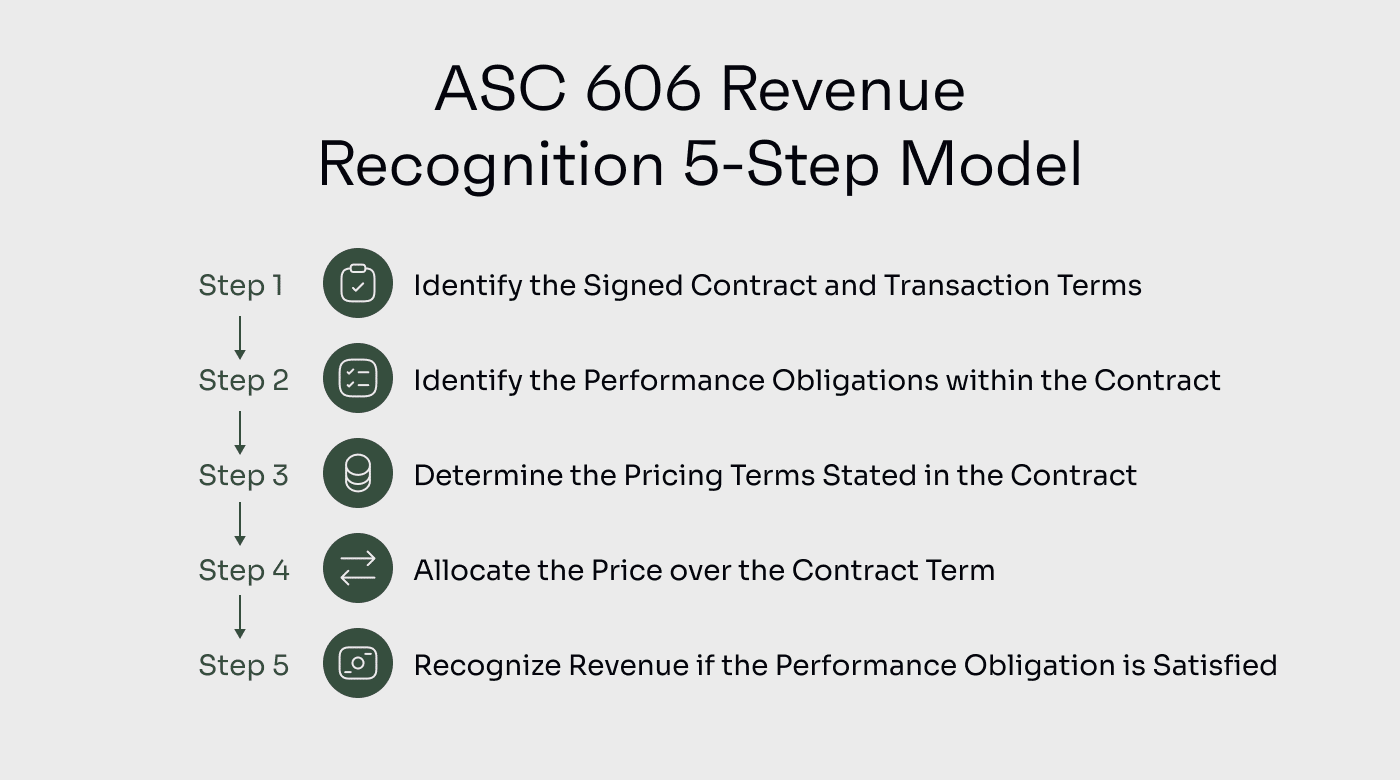

ASC 606 Revenue Recognition 5-Step Model

The core principle of the ASC 606 standard is its uniform five-step model, which can be applied across industries, including the software and Software as a Service (SaaS) sectors.

Let's delve into each step of the ASC 606 model and explore how it relates to different industries, with a focus on software and SaaS firms.

Step 1: Identifying the Contract(s) With Customers

In this initial step, companies must determine whether a valid contract exists with their customers. This applies to all industries, including software and SaaS firms.

For example, a SaaS company may enter into a contract with a customer to provide access to its cloud-based software platform for a specified period. The contract must meet specific criteria, such as having commercial substance and clear identification of the rights and obligations of both parties.

Step 2: Identifying Performance Obligations

Software and SaaS companies often offer multiple services or features bundled together. Identifying the distinct goods or services promised to the customer (performance obligations) within the contract is crucial.

In that regard, a software company may provide a software license, maintenance, and support services. Each of these obligations needs to be evaluated separately to determine the appropriate revenue recognition treatment.

Step 3: Determining the Transaction Price

In software and SaaS industries, pricing structures, such as one-time licensing fees or recurring subscription charges, can vary.

Besides these, you must consider other total factors like variable consideration, discounts, and refunds to establish the appropriate transaction price.

Step 4: Allocating the Transaction Price to Performance Obligations

Software and SaaS firms often have multiple elements within a contract.

This allocation ensures revenue is recognized appropriately based on the relative standalone selling prices of the different elements. If the standalone selling price is not directly observable, you can use estimation techniques to determine a reasonable value.

Step 5: Recognizing Revenue When Performance Obligations are Satisfied

In the software and SaaS industries, revenue recognition is typically tied to the delivery of services or access to the software.

For a SaaS company offering a project management tool with monthly subscriptions, to recognize revenue, you need to track when each performance obligation is satisfied.

Let’s assume that on February 1, a customer bought a monthly subscription for a $150 new-customer promo price. Then on March 1, they renewed their subscription at the $200 regular monthly price.

Let's say the following has taken place by March 5th:

| Criteria | $150 February 1 contract | $200 March 1 contract |

|---|---|---|

| Have risks and rewards of the service been transferred to the customer? | ✔ | |

| Has the seller given up control over the service? | ✔ | |

| Is payment reasonably assured? | ✔ | ✔ |

| Can the revenue be reasonably measured? | ✔ | |

| Can the cost of providing the service be reasonably estimated? | ✔ |

Since your company has only met its performance obligations for the February contract as of March 5th, only $150 can be recognized as revenue.

For more in-depth revenue recognition scenarios and application guidance, KPMG recently published an excellent guide for software and SaaS companies.

ASC 606 Implementation Challenges

Implementing the new revenue recognition standard can present challenges for many companies, especially those with customer contracts that include complex or combined services.

In this section, I will delve into some of the common challenges companies across different industries face when implementing ASC 606, and then I’ll get into SaaS-specific issues.

Identifying Performance Obligations

The challenge of identifying performance obligations within a contract arises when determining which goods or services are distinct and should be treated as separate obligations.

A telecommunications company that offers bundled services like voice calls, data plans, and messaging services may have challenges assessing whether these services should be treated as separate performance obligations or bundled together. This assessment has a significant impact on revenue recognition and the allocation of the transaction price.

Determining the Transaction Price

Determining the transaction price can also present challenges, particularly in industries where pricing structures are complex or subject to variability. Take the airline industry, for example. Airlines often sell tickets bundled with additional services such as baggage fees, in-flight meals, or priority boarding.

Allocating the transaction price between the ticket and these ancillary services requires careful consideration. Companies must determine the standalone selling prices of each component and allocate the transaction price accordingly to recognize revenue accurately.

Recognizing Revenue Over Time or at a Point in Time

ASC 606 provides guidelines for recognizing revenue either over time or at a point in time, depending on the transfer of control to the customer. This can pose challenges for companies, especially in industries where the delivery or transfer of control may not align with the contractual payment terms.

Let's consider a scenario involving a construction company's accounting. Construction companies often engage in long-term projects with multiple milestones. Deciding whether revenue should be recognized over time or at specific milestones requires careful evaluation of contractual terms, progress toward completion, and the transfer of control.

Impact of Contract Modifications on Revenue Recognition

Contract modifications, such as changes in scope, pricing, or duration, can pose challenges in revenue recognition under ASC 606.

Companies need to assess the impact of these modifications on the existing performance obligations and determine if they represent separate contracts or modifications of the original contract. Such modifications may influence the timing and extent of revenue recognition and require careful evaluation to ensure compliance.

Specific Challenges SaaS and Software Companies Face with ASC 606

SaaS and software companies tend to encounter unique complexities when implementing ASC 606, as compared to the issues faced by companies selling tangible goods. Let's dive into some of these challenges and explore how they impact revenue recognition.

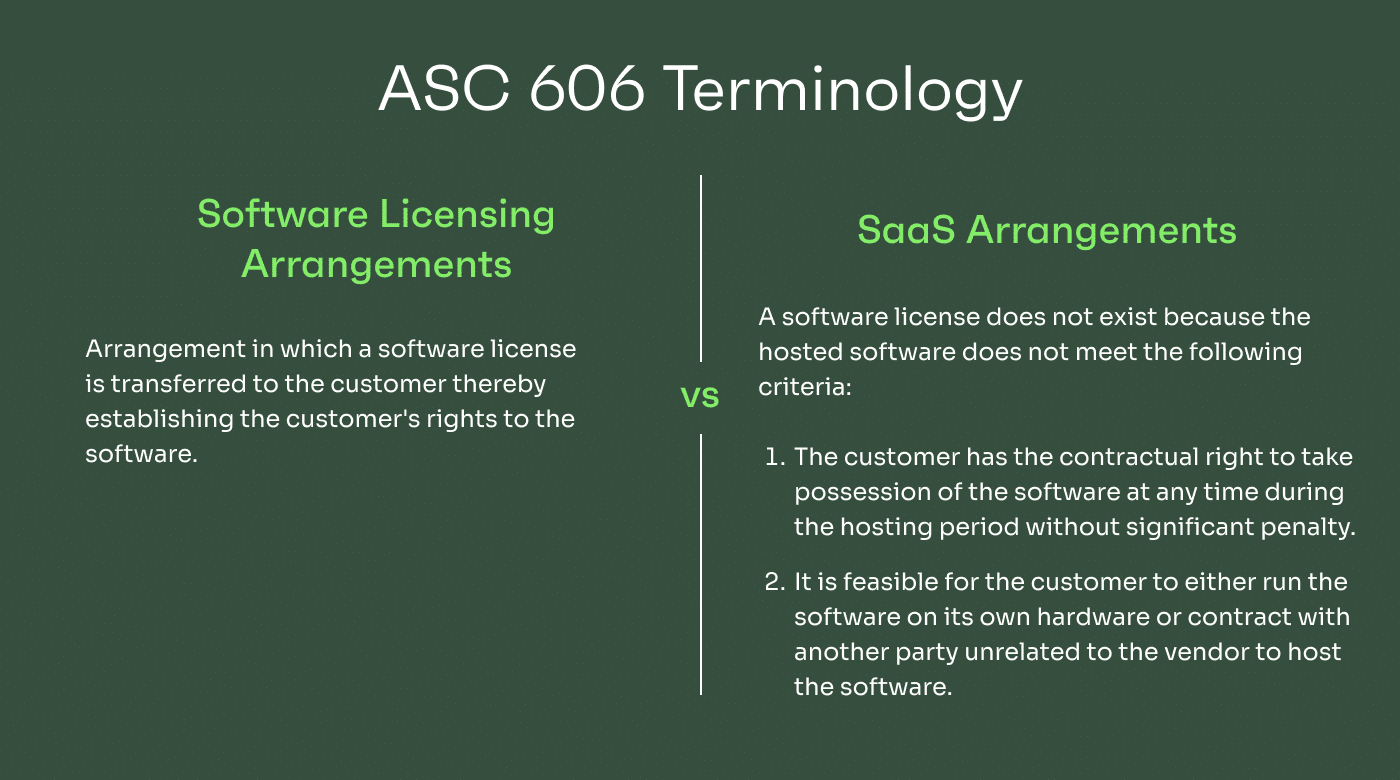

ASC 606 Terminology: Software Licensing Arrangement vs. SaaS Arrangement

One of the key challenges for SaaS and software companies lies in understanding the terminology used in ASC 606. ASC 606 distinguishes between software licensing arrangements and SaaS arrangements, each having its own set of guidelines for revenue recognition.

Differentiating between the two is crucial because it determines how revenue should be recognized. Software licensing arrangements typically involve the transfer of a license to the customer, while SaaS arrangements focus on providing ongoing services. Companies need to classify their arrangements accurately to ensure proper revenue recognition.

Managing Revenue Recognition for Recurring Subscription Models, Software Licensing, and SaaS Arrangements

SaaS companies often operate on recurring revenue models, where customers pay a subscription fee for ongoing access to their services.

The challenge arises in determining the appropriate timing and method of recognizing revenue from these recurring subscription models. Under ASC 606, revenue needs to be recognized over time as the customer receives access to and benefits from the services.

Identifying Distinct Elements and Performance Obligations Within Contracts

ASC 606 requires companies to identify a contract’s distinct elements and allocate the transaction price to each based on standalone selling prices. This can be challenging for SaaS and software companies due to the complexity of their offerings and bundled packages.

Let's say a software company offers a package that includes software licenses, training services, and ongoing technical support. They must carefully identify each distinct element and allocate the transaction price based on their standalone selling prices. If those elements don’t have standalone selling prices, they must be estimated. This requires careful consideration of market prices, customer preferences, and other factors to accurately determine the value of each component.

Recognizing Revenue Over Time for Long-Term Contracts or Ongoing Services

SaaS and software companies often enter into long-term contracts or provide ongoing services to customers. ASC 606 requires you to recognize revenue over time as control of goods or services is transferred to the customer. Determining the appropriate method to measure progress and allocate revenue over time becomes crucial.

For instance, imagine a software company that offers comprehensive enterprise resource planning (ERP) system implementation and support services over a two-year period. They must establish a reliable method to measure the progress of the implementation project and allocate revenue accordingly throughout the duration of the contract.

Managing Revenue Recognition Complexities for Tiered Pricing and Usage-Based Models

SaaS and software companies frequently employ tiered pricing models or usage-based pricing, where the fees charged to customers vary based on factors such as usage levels, user counts, or additional features. These complexities can pose challenges in accurately determining the transaction price and allocating revenue accordingly.

Practical Strategies for Successful ASC 606 Implementation

Now, to the crux of the matter: How can you position your company to implement ASC 606 successfully? What strategies can you deploy to ensure a smooth transition and effective adoption of the new standard? Let's explore practical approaches that can help you confidently navigate this process and achieve successful implementation.

Encouraging Cross-functional Collaboration

Implementing ASC 606 requires collaboration across departments within your organization, including sales, legal, operations, and finance teams. Encouraging cross-functional collaboration can ease implementation hiccups and shorten your timeline to launch.

Adopting Contract Management Systems

Contract management software and ERP systems can help automate contract reviews, identify key terms and conditions, and generate reports for revenue recognition.

Enhancing Data Collection and Analysis

ASC 606 implementation requires robust data collection and analysis capabilities. Ensure that your company has access to accurate and reliable data related to contracts, pricing, performance obligations, and customer information.

Conducting Regular Training and Education

Promote a culture of continuous learning and awareness regarding ASC 606 within your accounting department by providing regular training and education to employees involved in the revenue recognition process.

Training can cover the key provisions of ASC 606 and provide practical examples and guidance on applying the standard to specific scenarios.

Engaging External Experts for Guidance

Consider engaging external experts, such as consultants or auditors with expertise in ASC 606, to provide guidance and support throughout the implementation process.

These professionals can offer insights into industry best practices, help interpret complex provisions, and assist in developing implementation strategies tailored to your company's specific needs.

ASC 606 Compliance and Audit Considerations

It is crucial to understand the key considerations when it comes to internal controls, audit trails, disclosures, and working with auditors. These are the most important components:

Internal Controls and Documentation Requirements

Implementing robust internal controls is essential for ASC 606 compliance. Think of it as laying a solid foundation to ensure accurate revenue recognition.

Internal controls help ensure that revenue recognition processes are accurately executed and financial information is reliable. It involves designing and implementing procedures to monitor contract inception, performance obligations, transaction price allocation, and revenue recognition.

When you document and maintain records of contract terms, performance obligations, transaction prices, and the allocation of revenue, you are safeguarding evidence of revenue recognition—which can help facilitate audits and provide transparency to stakeholders. Once you have this in place, you can input your controls into your audit management software of choice and let it control your transaction classification for you.

Audit Trail and Evidence of Revenue Recognition

An audit trail is a chronological record that traces the flow of transactions related to revenue recognition. Your company can maintain an audit trail that includes customer contract details, billing records, evidence of customer usage or access to services, and revenue recognition calculations over time.

A clear audit trail also documents key milestones and evidence supporting revenue recognition. This might include signed contracts, delivery confirmations, customer acceptance records, or other documentation that reflects the transfer of control.

This trail provides a comprehensive overview of revenue recognition, supports the company's assertions during the audit process, and validates the accuracy and appropriateness of your revenue recognition practices.

Reviewing Disclosures and Financial Statements

Imagine you're preparing your company's financial statements and disclosures in accordance with ASC 606. It's not just about crunching numbers, but also ensuring the information is transparent and informative for stakeholders.

In view of that, your company may need to disclose significant judgments made in allocating transaction prices, the nature and timing of performance obligations, and changes in contract balances. Financial statement footnote disclosures should include meaningful and detailed disclosures regarding revenue recognition policies and estimates applied.

This level of transparency enhances the understanding of revenue recognition practices, increases comparability across companies, and affirms the credibility of your financial statements.

Working With External Advisors and Consultants

Companies can ensure that their revenue recognition processes align with ASC 606 requirements by working closely with external advisors and consultants. They can provide guidance on internal controls and documentation standards and assist in identifying potential issues or areas of improvement.

Be sure to seek out advice from external experts early to gain their insights and expertise. You shouldn’t use the same public accounting firm that performs your financial statement audit, as that would require them to audit their own work.

It’s important that an external consultant or advisor understands your company's business model, revenue streams, industry-specific nuances, and the impact of ASC 606 on financial reporting so they can provide you with appropriate insights.

Importance of Automation and Technology in ASC 606 Compliance

Manual processes and spreadsheets have long been the traditional approach to managing revenue recognition, but this can be a daunting task for businesses, especially in the dynamic and fast-paced software industry.

This is where automation and technology play a crucial role. By leveraging software solutions, companies can streamline their revenue recognition processes, thereby enhancing their compliance with ASC 606—all while improving data management, reporting efficiency, and reducing the risk of errors and non-compliance.

Leveraging Software Solutions for Revenue Recognition

Imagine a software company grappling with numerous customer contracts, each containing multiple performance obligations and complex billing arrangements. Manual calculations and tracking become time-consuming and error-prone.

Companies can automate the complex processes involved in ASC 606 compliance by implementing specialized revenue recognition software. These solutions automate the process and can accurately identify performance obligations, allocate transaction prices, and handle bundle arrangements and contract modifications, reducing manual effort and ensuring accuracy.

Enhancing Data Management and Reporting Efficiency

The software industry thrives on data-driven insights, making efficient data management critical for success.

Software solutions can centralize and organize contract data, making it easily accessible for auditors and stakeholders. Using technology, companies can integrate data from various systems and automate data consolidation, ensuring a single source of truth. This streamlines reporting processes, reduces the risk of errors, and provides a holistic view of revenue across the organization.

Real-time Monitoring and Analytics for Revenue Insights

The software industry moves at a lightning pace, and revenue recognition delays are not an option. Automation enables real-time monitoring of revenue streams, giving companies immediate visibility into their financial performance.

Advanced data analytics tools can provide valuable revenue insights, such as revenue trends, contract profitability, and customer behavior. Armed with this information, software companies can make data-driven decisions, identify growth opportunities, and proactively address potential issues.

Mitigating Risks and Improving Compliance Controls

Non-compliance with ASC 606 can lead to serious consequences, including reputational damage and legal liabilities. Software solutions can introduce robust compliance controls, flagging potential discrepancies and ensuring adherence to the standard.

Automated internal controls can identify irregularities and minimize the risk of revenue leakage or misstatements. By mitigating risks, software companies can confidently navigate the complexities of ASC 606 compliance and focus on driving innovation and growth.

Embracing ASC 606 for Revenue Recognition

ASC 606 holds immense significance in financial reporting. By adhering to the five-step model businesses can more accurately identify performance obligations in their contracts with customers and recognize revenue appropriately.

While implementing ASC 606 may present challenges, practical strategies like collaboration, contract management systems, data analysis, and leveraging automation can help.

Subscribe to The CFO Club's newsletter for weekly articles, podcasts, industry insights, and must-have resources for finance leaders.

{kind=link}