The Complete Guide To Preparing Financial Statements

Understanding Financial Statements: A university degree helps in understanding how financial statements work and provide a comprehensive financial picture.

Knowledge of Accounting Concepts: Preparing financial statements requires a working knowledge of accounting concepts like double-entry accounting, accrual basis accounting, and the accounting cycle.

I got a university degree to learn how financial statements work and how those numbers come together to give you a comprehensive financial picture. After all, preparing financial statements requires knowledge of accounting concepts like double-entry accounting, accrual basis accounting, and the accounting cycle.

But there’s good news: you don’t have to. You can just read this 15-minute guide to preparing the four must-have financial statements:

- Income statement

- Statement of changes in equity

- Balance sheet

- Cash flow statement

Option B: Get Robots

If you’re dreading starting on the financial statement preparation process, don’t worry — there are some great financial reporting tools out there to help you out. Now, those 15 minutes can go back into growing your business.

Clicks on the links below may earn a commission, which supports our independent testing and review of software and services. Learn more about how we stay transparent.

Financial Statements Overview

Financial statements are the business world's equivalent of a medical check-up. They provide an overview of an organization's financial condition, including profitability, cash flow, and overall worth.

There are four types of financial statements, each with a unique purpose. Together, they help paint a picture of your accounting profit:

- Income statement: An income statement summarizes your company’s financial performance, showing revenue, expenses (including taxes), and profit over a specific accounting period.

- Statement of changes in equity: The statement of changes in equity (SOCE) — also known as the statement of retained earnings or statement of owners’ equity — details how shareholders’ equity has changed over time. Equity can change for various reasons, such as adding or withdrawing capital and paying dividends.

- Balance sheet: The balance sheet shows what the company owns (assets), owes (liabilities), and the stake held by shareholders (equity). It’s a snapshot of your company’s financial condition on a given day.

- Cash flow statement: The cash flow statement summarizes cash inflow and outflow. This statement is crucial for startups since many fail due to their inability to manage cash effectively. Even if you’re profitable, you can run out of cash — profit generated during a year does not equal cash generated during a year.

These documents provide valuable insights into a business’s financial position to stakeholders such as investors, creditors, and employees.

Why Are Financial Statements Important?

Financial statements provide standardized insights into your company’s financial performance, capital structure, and cash flow. Stakeholders need this information to:

- Make informed decisions: The financial data in financial statements can guide strategic decisions. For example, the income statement shows revenue growth and operating income — two key elements to evaluate if you’re considering dropping a product line.

- Raise capital: When raising new equity or debt, lenders and investors will assess your capital structure, profitability, and other details from your financial statements.

- Comparative analysis: Financial statements help you compare your business’s performance with industry benchmarks, like how your gross margin compares to competitors.

- Compliance: For certain companies, such as publicly traded companies or private ones with public debt, filing financial statements with regulatory bodies like the SEC is compulsory.

Preparing Financial Statements

When preparing financial statements, you have two options:

- Use accounting software to manage the process. These systems automatically update financial statements in real time when you record transactions, making preparation straightforward.

- Prepare your statements manually. I’ll explain how to do this in the next section.

Large companies prepare financial statements following GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards).

Despite differences in GAAP and IFRS accounting standards, the purpose of each financial statement remains the same.

Step 1: Prepare a Trial Balance

A trial balance is a summary of open accounts in your books. Here’s how to prepare one:

1. Record Transactions

Recording transactions is the gateway for preparing financial statements. Every transaction, including sales, purchases, and returns, impacts your financial statements.

The old-school method was to record transactions in a journal. However, using accounting software means you can just enter transaction details into the system, and it takes care of the rest.

2. Post Journal Entries to Sub-Ledger Accounts

Next, post journal entries to sub-ledger accounts, which record details and provide more context than the general ledger. Sales transactions go to the sales ledger, credit sales to the accounts receivable ledger, and so on.

The sub-ledger accounts are aggregated into five general ledger categories: income, expenses, assets, liabilities, and equity.

3. Adjusting Entries

Before closing your accounts, you may need to post adjusting entries. They are for unrecognized income or expenses for the period. Here’s an example.

Suppose your company lent $20,000 to a friend’s company, ABC Corp., on December 1, 2023. According to the agreement, interest is due every 12 months at a 4% annual rate.

On December 31, 2023, you prepared financial statements. You recorded the $20,000 loan as an asset for your company, but what about the $66.67 December interest outstanding [($20,000 x 4%) / 12]?

The interest would be an adjusting entry:

| Account | Debit | Credit |

|---|---|---|

| ABC Corp. interest receivable A/C (current asset) | $66.67 | - |

| Interest Income A/C | - | $66.67 |

4. Adjusted Trial Balance

A trial balance checks the arithmetic accuracy of accounts but doesn't find other errors like amounts posted in the wrong account. This is where detailed variance reporting becomes essential.

In double-entry accounting, all debits have corresponding credits of equal amounts. A trial balance checks if they’re equal; if the totals differ, check for arithmetic errors.

To create a trial balance, list and sum all account balances in your books. (Accounting software can do this automatically.)

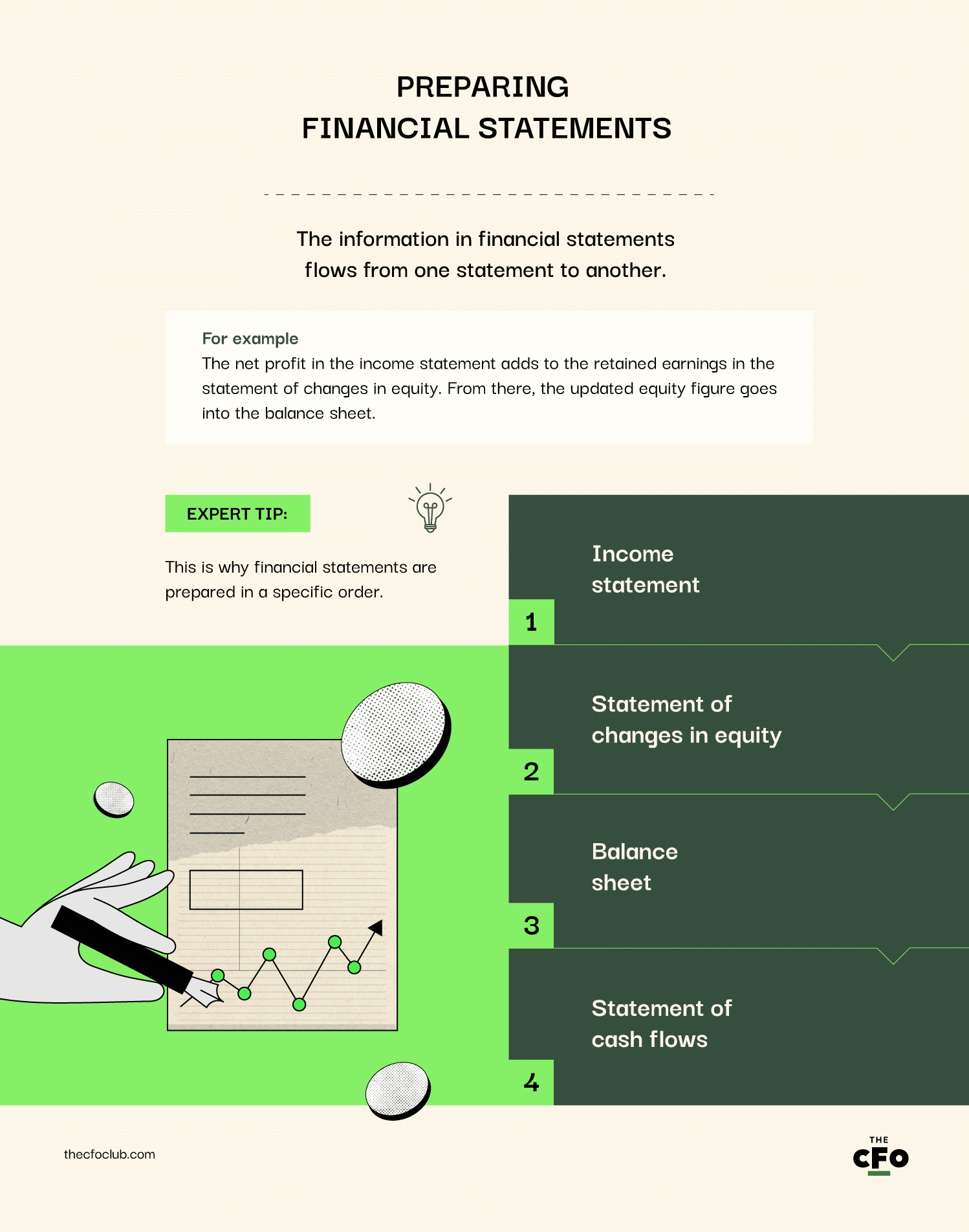

Step 2: Prepare the Income Statement

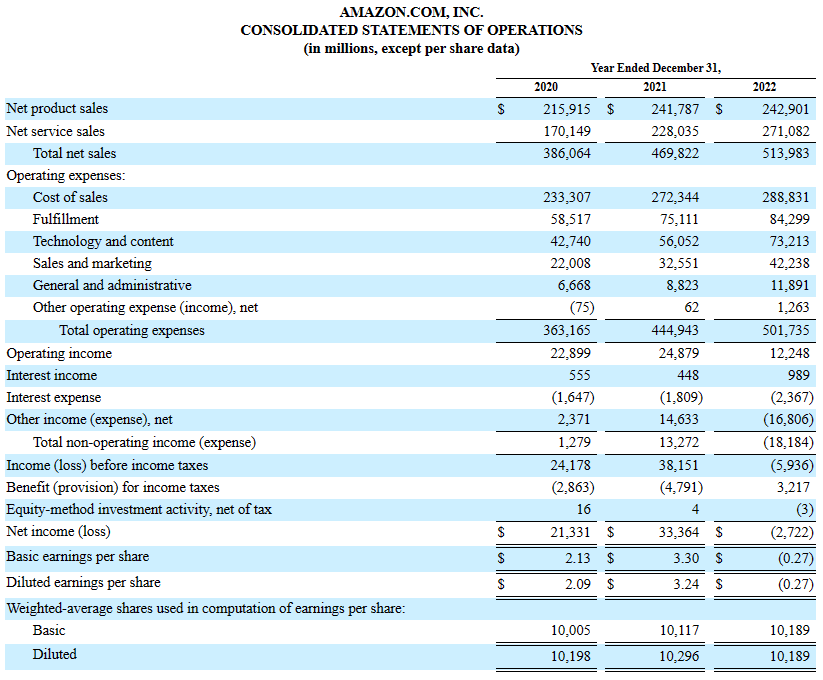

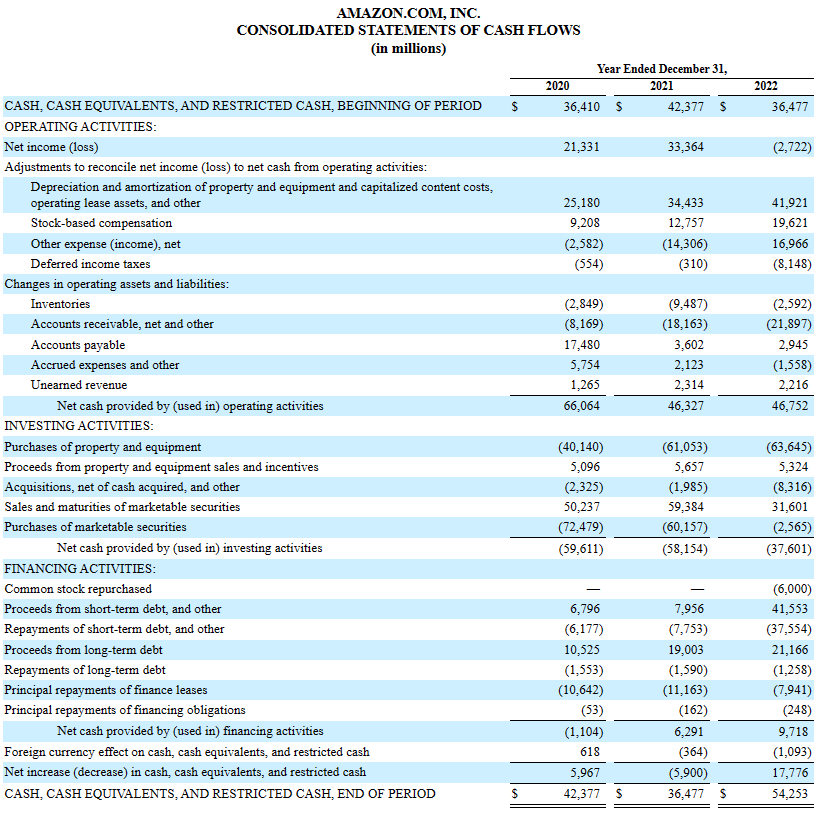

Let’s examine Amazon’s financial statements for context, starting with the income statement.

When preparing financial statements manually, start with the income statement. The sequence doesn’t matter with an accounting system.

Why? The net income at the end of the income statement is added to retained earnings, required to complete the statement of changes in equity. The equity figure is needed to prepare the balance sheet.

Doing this out of order will result in repeated work.

1. Start with Revenue

Sum up all net sales during the period. Don’t include other income types like rent or interest — that’s not revenue. If you own multiple businesses, make sure to consolidate your finances beforehand.

2. Subtract Expenses

Once you’ve added revenue to the top line:

- To compute the gross profit, subtract the cost of sales (or cost of goods sold) from revenue.

- To compute the operating income, subtract selling, general, and administrative expenses (or operating expenses) from the gross profit.

- To compute income before taxes, add non-operating income (like interest and gains on financial instruments) and subtract non-operating losses.

- To calculate the net income, subtract income tax.

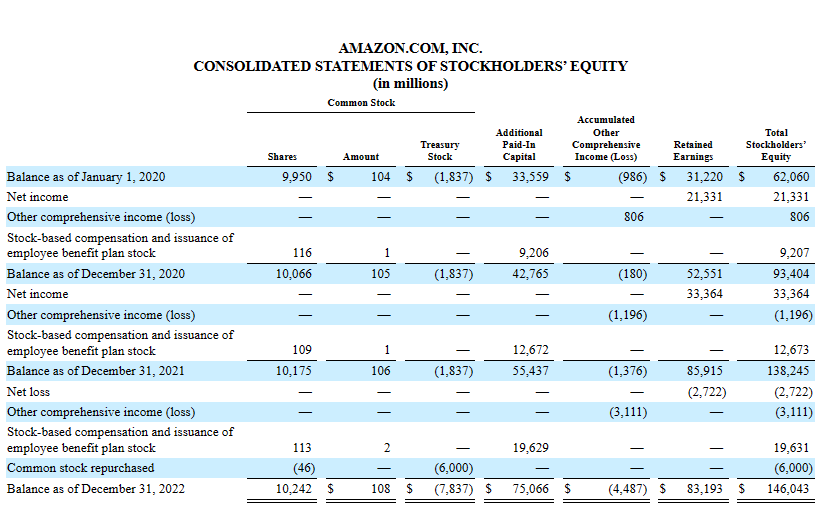

Step 3: Prepare the Statement of Changes in Equity

Your SOCE starts with the opening balance in the shareholders’ equity (total of common and preferred stock) from the beginning of the period (i.e., last year’s SOCE).

From here, make the following adjustments:

1. Add Retained Earnings

Retained earnings are the portion of net income not distributed as dividends.

To calculate retained earnings:

- Subtract the dividends distributed (debit them to the retained earnings account).

- Add net income to retained earnings (credit net income or debit net loss).

Once you have the closing balance for retained earnings, add it to the opening balance of owners’ equity.

2. Add/Subtract Other Comprehensive Income/Losses

Other comprehensive income refers to unrealized gains and losses that don’t appear on the income statement.

If the company revalues an asset and it’s worth less, it’s the company’s loss. However, the loss is only realized when it sells that asset.

Items such as foreign currency translation adjustments and changes in pension liabilities appear here.

3. Record Changes in Capital

If the company issues new shares, add them here. If it repurchases shares, subtract them.

4. Calculate Closing Balance

Calculate the closing balance in stockholders’ equity and input it into the balance sheet.

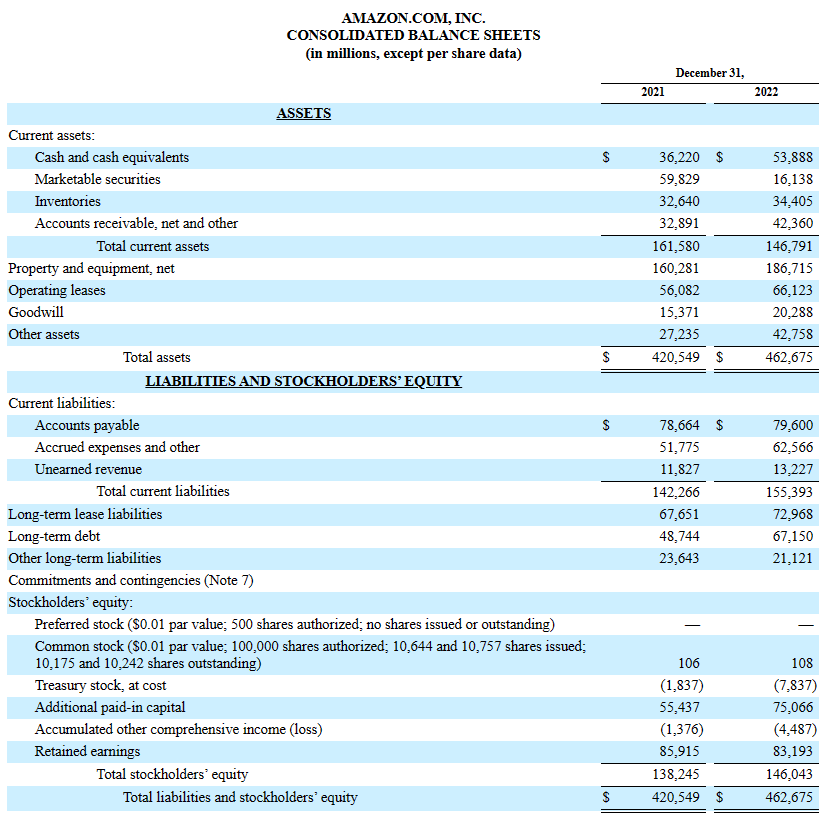

Step 4: Prepare the Balance Sheet

I have good news.

You don’t have to compute most items in the balance sheet. This statement lists your account balances, which you would have calculated before preparing your trial balance.

1. Assets

Assets appear on the left side of the balance sheet. Here, balances of fixed asset accounts like land, current accounts like cash, and intangible accounts like goodwill appear.

2. Liabilities

Liabilities are money the company owes. Here, balances of current liabilities like accounts payable and long-term liabilities like bonds appear.

3. Shareholders’ Equity (Business Net Worth)

Shareholders’ equity is money that belongs to the company’s owners (equity shareholders) and preference shareholders.

Here’s a more intuitive way to view it: Shareholders’ equity is the difference between assets (what the company owns) and liabilities (what it owes).

This section includes the equity figure from the statement of changes in equity.

Step 5: Prepare the Cash Flow Statement

Cash flow reveals your business’s cash sources and uses. Maintaining a healthy balance — enough but not too much — is mission-critical.

Most startups struggle with running out of cash. Monitoring the cash flow statement helps predict and prepare for issues before they worsen.

Preparing a cash flow statement depends on whether you’re using the direct or indirect method.

Both types of cash flow statements have three categories, which I’ll explain below. Summing the inflows and outflows from these categories gives you the net cash inflow or outflow during the reporting period.

1. Cash Flow from Operating Activities

Cash flow from operating activities is the sum of cash inflow and outflow from activities like collection from debtors, payment to creditors, and taxes paid.

In the indirect method of preparing the cash flow statement, non-cash items like depreciation and amortization will also appear here.

2. Cash Flow from Investing Activities

Cash flow from investing activities includes cash received from selling securities and cash paid to buy new assets like land and equipment.

If you’re using the indirect method, there are additional line items in this section as well. You’ll need to subtract asset sale gains and add back losses.

3. Cash Flow from Financing Activities

This section includes activities like raising new capital, paying off debt, and paying dividends.

If using the indirect method, subtract financing gains (like interest received) and add back financing expenses or losses (like interest paid).

The Bottom Line

Grasping this information can be overwhelming without accounting knowledge, so here’s a recap:

- The income statement shows if your business is profitable, guiding decisions on pricing, cost structure, or discontinuing a product line.

- The statement of changes in equity informs interested parties about ownership changes over the period and any payouts to owners.

- The balance sheet summarizes your financial position. If you have too much debt in an industry with shrinking profit margins and low growth, the business might lose its ability to service the debt over time.

- Finally, the cash flow statement shows how efficiently you’re generating and using cash. If your business doesn’t generate enough cash, how will you pay salaries, debt installments, or accounts payable?

Understand what each financial statement tells you and where the information comes from. Accounting software handles tasks like preparing the trial balance, calculating net income, and drawing the cash flow statement.

Ready to compound your abilities as a finance leader? Subscribe to our newsletter for expert advice, guides, and recommendations from finance leaders shaping the tech industry.

{kind=link}