Statement of Retained Earnings: What You Need to Know

If you aren’t overly familiar with financial statements, it can be hard to pinpoint which statement is useful for which purpose. If you find yourself wondering where your profits have gone off to, you need the statement of retained earnings.

In this guide, I’ll help you understand and interpret the statement of retained earnings, and give you my tips for extracting valuable insights from this short—but important—financial statement.

Statement of Retained Earnings Overview

The statement of retained earnings is a financial document that summarizes how the company’s retained earnings—aka the revenue they’ve kept after paying for expenses—changed during a given period.

Other Names for the Statement of Retained Earnings

While it’s sometimes referred to as the statement of stockholders’ equity, statement of owner’s equity, or equity statement, these technically aren't the same thing.

The statement of retained earnings—what we're focusing on today—tells you how much of the current year’s earnings were distributed as dividends and reinvested into the business.

On the other hand, the statement of stockholders’ equity shows how the balance of the shareholders’ equity account changed over the current accounting period.

With that said, large corporations often club the statement of retained earnings into the statement of stockholders’ equity for simplicity, which explains why people refer to this statement using the other name. Here’s an example from Apple’s latest 10K:

It’s easy to imagine how this statement helps investors and other stakeholders. If they see a business reinvesting a large portion of its earnings into themselves, it shows management’s confidence in the company’s future prospects.

Net Income vs Retained Earnings

Let’s start with the basics. Net income is the profit your company earns during a certain period. We have a comprehensive guide on the income statement where I explain how the net income is calculated.

It’s the amount your company is left with after subtracting all expenses, including operating and non-operating expenses, one-off expenses, and taxes.

Net income belongs to the company’s shareholders. There are two things a company can do with its net income:

- Declare dividends: If the company believes it has matured and doesn’t see much room for growth, it could declare dividends for equity stockholders.

- Reinvest: Companies need cash to grow. If a company has great growth prospects, it will be better off reinvesting money instead of paying it out as dividends. Money that a company reinvests becomes retained earnings.

In theory, retained earnings should keep accumulating as long as a company remains profitable and doesn’t declare dividends.

Why is the Equity Statement Important?

The equity statement is important because it indicates management’s confidence in the company's future growth. If management believes the company needs capital to fuel growth, they’ll retain earnings instead of paying them out as dividends.

Suppose you’re an investor. You want to invest in a growth asset instead of a high-dividend-yield stock. Before you put money into a company, you need to know if the company is actually growing—there are multiple ways to do this.

Revenue growth is a common and often reliable indicator of past growth. To predict growth, you need leading indicators like the management’s guidance on future plans and, of course, the amount of money the company has retained over the previous periods to support that future growth.

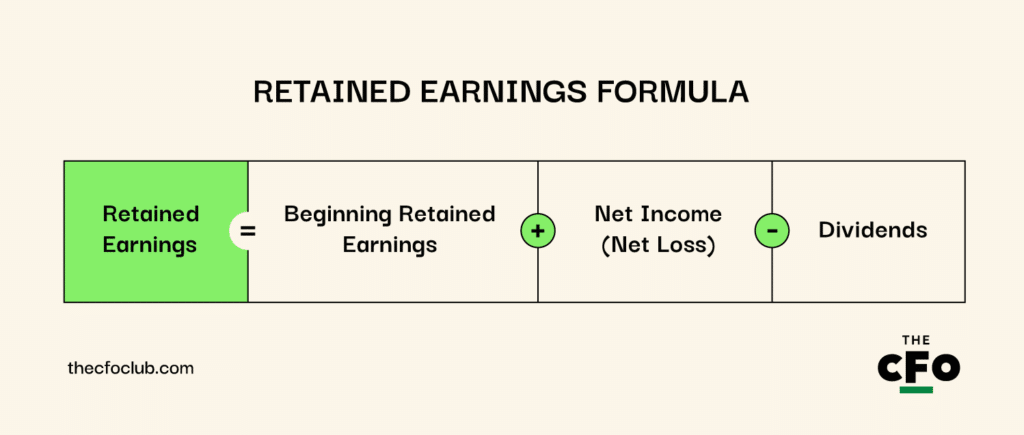

Retained Earnings Formula

Retained earnings at the end of a period are calculated as:

Note that “Dividends” include all types of dividends, including stock issuances.

Appropriated vs Unappropriated Retained Earnings

Appropriated earnings are earnings that aren’t available for distribution among shareholders. Earnings are appropriated to communicate to shareholders that the management expects a large transaction in the future. Basically, it’s management’s way of saying “buzz off, shareholders, we have plans for that money”.

A company’s board of directors may decide to appropriate earnings for various purposes, including acquisition, stock buyback, research and development, and debt reduction.

Here’s the journal entry for appropriating earnings:

| Account | Debit (Dr.) | Credit (Cr.) |

|---|---|---|

| Retained Earnings | $100,000 | - |

| Appropriated Retained Earnings | - | $100,000 |

Unappropriated earnings—as you may have guessed—are the amount of earnings not appropriated at the end of a given period. These earnings are typically also used for growth, but they’re not earmarked for a specific transaction or project.

Who Creates the Statement of Retained Earnings?

Modern companies use accounting software to prepare financial statements, including this one. Typically, the software automatically populates and updates the statement as part of the accounting cycle throughout the reporting period. However, you need an accountant to verify that the statement of retained earnings is ready for reporting.

Decisions related to dividend distribution and appropriation of earnings are in the hands of management and the board. Accountants need this information and management’s guidance before signing off on the statement of retained earnings.

How to Prepare a Retained Earnings Statement

Preparing a statement of retained earnings is fairly simple because there are only a few transactions to factor in. Remember, you don’t have to prepare a retained earnings statement manually. A small business accounting software can automatically prepare one for you. However, if you’re curious, here’s a quick step-by-step guide:

1. Enter the Opening Balance

The first figure on a statement of retained earnings is last year’s ending retained earnings balance. Look at the retained earnings on your balance sheet or search through your general ledger, find the retained earnings account, and note down the closing balance.

2. Add Net Income

If you haven’t already done so, prepare the income statement. Take the net income figure from the income statement and add (or subtract in case of a net loss) it to the statement of retained earnings.

3. Deduct Dividend Payments

Dividends are the most common line item here, but you can deduct anything else you use earnings for.

For example, any common stock you buy back during the year should be deducted from the earnings. Similarly, if you’ve decided to pay dividends, subtract dividends from the retained earnings.

Note that the amount of dividends reported in the statement of retained earnings doesn’t include dividends on preferred stock. They’re reported on the income statement as a subtraction from net income and not as an expense because they’re not tax-deductible.

4. Calculate the Closing Balance

Sum up the figures added to the statement of retained earnings to calculate the closing balance. This will be the amount of retained earnings reported on the current period’s balance sheet in the shareholders’ equity section.

Statement of Retained Earnings Example

Suppose you’re preparing an equity statement for ABC Corp., which has the following numbers to report:

- Opening balance in the retained earnings account: $5,000,000

- Net income: $1,000,000

- Dividends for the current year: $250,000

Here’s what the statement of retained earnings would look like:

ABC Corporation

Retained Earnings Statement for the year ending 31 December, 2024

| Beginning Balance | $5,000,000 | |

| Add: Net Income | $1,000,000 | |

| Subtotal | $6,000,000 | |

| Less: Dividends Declared and Paid | ($250,000) | |

| Closing Balance | $5,750,000 |

The closing balance of the retained earnings is added to the equity section of the balance sheet. This is why you need to calculate retained earnings when building a three-statement model, even though you don’t necessarily need to model the entire statement separately.

How to Analyze the Statement of Retained Earnings

The statement of retained earnings is primarily used to assess the management’s future outlook for the business.

Consistently higher dividends in the statement indicate that the company is maturing and doesn’t need capital for growth, whereas younger, high-growth companies are less likely to declare dividends.

Let’s talk about a few metrics that can help you assess a statement of retained earnings.

Retention Ratio and Dividend Payout Ratio

The retention and dividend payout ratios represent the percentage of earnings retained or paid as dividends, respectively. A company’s retention and dividend payout ratios always equal up to 1. Here are the formulas:

- Retention ratio: (Net Income - Dividends) / Net Income

- Dividend payout ratio: Dividends / Net Income

Let’s use an example. Suppose a company’s net profit for the current accounting period is $500,000. The company decides to pay $100,000 as dividends. Here’s what the retention and payout ratios would look like:

- Retention ratio = 0.8: Calculated as [500,000 - 100,000) / $500,000]

- Dividend payout ratio = 0.2: Calculated as [100,000 / 500,000]

Note that a high dividend payout ratio isn’t bad. If you’re an investor who likes consistent income, investing in mature companies is a great way to benefit from potential long-term capital appreciation and consistent dividends.

With that said, a high dividend payout ratio isn’t always good, either. A company that doesn’t pay dividends could multiply an investor’s capital, provided things go well. It’s all up to what you want your investments to do.

Retained Earnings to Market Value

Retained earnings to market value isn’t as commonly used as retention and payout ratios, but it does provide insights into how effectively a company is using its retained earnings. After all, an investor only benefits when you use retained earnings effectively.

To calculate retained earnings to market value, divide the share price by the retained earnings per share. For example, suppose your company’s share price increased from $10 to $60 over the past five years and the total earnings retained per share over the same five years is $5.

This means the company was able to generate $5 in market value for each dollar of earnings it retained. Had the company used debt capital instead, they’d have generated less value because of the interest payment; internally generated capital helps profitable companies create value more efficiently.

Statement of Retained Earnings is One Piece of the Puzzle

The statement of retained earnings is a great way to assess a company’s growth prospects, but there’s plenty more information shareholders and management need to make smart decisions.

For example, even if you retain earnings to invest in a major marketing campaign, you need enough cash on hand to execute your plan. That’s where you need to bring in your cash flow statement.

On the other hand, investors should look at more than just high retained earnings when looking for a high-growth investment. An overleveraged company may avoid paying dividends, but that doesn’t make the company a high-growth asset for the investor. Investors need to look at the company’s balance sheet to see the big picture.

Like what you just read? Subscribe to The CFO Club newsletter to receive expert advice, guides, and insights from finance professionals every week.

{kind=link}