How To Prepare An Income Statement In 8 Simple Steps

To prepare an income statement, you’ll gather your revenue and expense data, subtract costs from earnings, and organize it all to show your net profit or loss for a given period.

Simple in theory—less so in practice, especially when you’re a small business owner juggling a dozen roles and just need clear, trustworthy numbers to make smart decisions. That’s where this guide comes in.

As a digital software expert with a background in financial management, I’ve helped business owners streamline their financials using modern tools and simple logic. This guide breaks down what to collect, how to structure it, and where to look for red flags. Let’s get started.

What Is An Income Statement?

An income statement is a financial report covering a business’ income (and expenses) over a certain period of time — usually a quarter or full fiscal year. Think of it like a report card for your business, showing how much money you made (or lost).

The purpose of an income statement is to detail the company’s financial performance in the specific period. An income statement is also sometimes referred to as a profit and loss statement (or P&L statement).

Preparing financial statements is crucial to understanding the performance of your business. After preparing an income statement, you’ll understand your exact business net income or net loss — as well as other important figures such as your gross profit, operating income, and income before taxes.

An income statement is among the most important financial statements, and a crucial step in the accounting cycle. It’s also the first report that needs to be prepared in the 3-statement model of accounting, which also includes the balance sheet and cash flow statement.

What Information Do You Need To Prepare An Income Statement?

Before you start building your income statement, you'll need the following detailed financial records for your company for the given period of time:

- Revenue (how much you took in)

- Operating expenses (how much you spent)

- Cost of goods sold (the cost of actual goods sold, including merchandise you resell or the cost of components for manufacturing)

- Interest costs (like interest paid on loans)

- Tax expenses (like payroll taxes and federal/state business income taxes)

If you don’t already have these numbers prepared, compile them before starting your income statement. You can check your bookkeeping system for your records.

How To Prepare An Income Statement

I’m not an accountant, but I’ve worked with enough financial professionals to know that preparing an income statement isn't fast and easy. It requires a lot of calculations.

To help simplify the process, here's a look at how most accountants approach it, in 8 steps:

Step 0. Let Accounting Software Do It For You!

If you have good accounting software, you can create an income statement with just a few clicks. Most tools let you select a reporting period and automatically generate the report using synced transaction data. They pull income and expenses from your bank, sales platform, or POS system, saving you from manual entry and spreadsheet headaches.

For busy business owners, this automation boosts accuracy and efficiency. Still, knowing how to build one yourself is a smart backup, and a great way to understand what your software is actually doing.

The rest of this guide will walk you through it, step by step.

1. Choose Your Reporting Period

Income statements analyze your business performance over a set period of time — usually 3 to 12 months. Before you start, get clear on the time period that is most beneficial for your current analysis.

- Shorter timeframes (1 month, 3 months) are best for informing quick tweaks to your business budget and tactics.

- Longer time frames (3 months, 6 months, 12 months) are more useful for evaluating long-term trends, strategy, and capturing high-level data on your business.

2. Calculate Your Total Revenue

Next, gather your revenue records from all sources. This could include:

- Sales of goods

- Sales of services or subscriptions

- Rent revenue

- Interest revenue

- Any other revenue specific to your business

In most cases, you’ll want to look at total revenue across all aspects of your business. That said, in some situations, such as if you have a holding company, it can make sense to prepare separate income statements for different business segments or locations.

Subtracting any returns, refunds, or discounts from your revenue figures is also important for getting true revenue numbers.

3. Calculate Your Costs of Goods Sold (COGS)

Your cost of goods sold is composed of all the costs that went into creating the products or services that you sold during this reporting period. This can include:

- Direct labor costs

- Costs for goods purchased for resale

- Costs for any materials, parts, or components used in production

- Distribution costs

Importantly, COGS are only recorded for goods or services that have already been sold. For instance, say you purchased $10,000 worth of goods to resell, but only sold $3,000 in the reporting period. Your COGS for the period would then be $3,000, and your remaining inventory would be $7,000.

4. Calculate Your Gross Profit

Your gross profit refers to profits before operating expenses (like rent and utilities) are taken into account. Gross profit is useful to calculate your gross margin and can inform your pricing strategy.

To find your gross profit, subtract COGS from total revenue.

5. Calculate Your Operating Expenses

Next, add up all your operating expenses (OPEX). Operating expenses are all other business expenses that are not directly related to producing your goods or services for sale. This could include:

- Certain salaries (labor unrelated to your sales, like an accountant or janitor)

- Rent

- Utilities

- Legal fees

- Insurance

- Office supplies

Add up all your operating expenses to find your total OPEX figures.

6. Calculate Your Pre-Tax Income

Now you have all your revenue and expenses, except for taxes. Subtract your total operating expenses from your gross profit to arrive at your total earnings before taxes and interest (EBIT).

7. Calculate Your Interest and Tax Expenses

Now you know how much your business actually earned, but you still have to pay the IRS (and local tax authorities) — and potentially your lender, too. This next step tallies up all your:

- Interest expenses (interest paid on credit cards, business loans, etc.)

- Tax expenses (taxes paid to local, state, and federal governments)

For interest costs, check your bank statements, credit card statements, and loan documents to see how much interest you’ve been charged in the reporting period. Or, of course, reference your records in your accounting software.

For tax expenses, you should ideally reference your tax returns for the reporting period. However, you may not yet have filed a tax return. In this case, do your best to estimate your tax burden by using a previous year’s records and adjusting for your increased (or decreased) revenue figures. If you know your estimated tax rate, use this to get a rough idea of the amount of money you’ll owe in taxes.

8. Calculate Your Net Income

Finally, you have every figure necessary to calculate your net profit or net income. Simply subtract your interest and tax expenses from your pre-tax income to arrive at your net income — or your true “bottom line”.

Example Income Statement

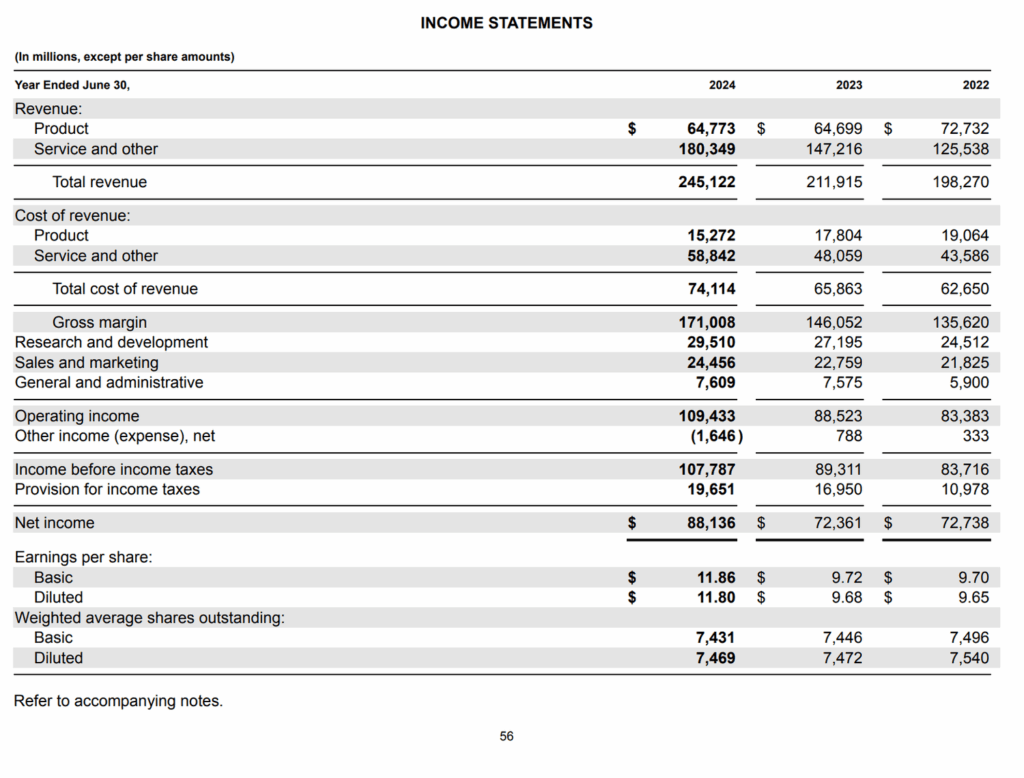

Sometimes, a visual example is all you need. Take Microsoft's income statement for the fiscal year ending on June 30, 2024, for example:

The reporting period for Microsoft's income statement was July 1, 2023 to June 30, 2024. In this period, they reported the following amounts:

- Total Revenue: $245.1 billion

- Cost of Goods Sold: $74.1 billion

- Gross Profit: $171 billion

- Operating Expenses: $64.4 billion

- Operating Income: $109.4 billion

- Interest Costs: $-1.6 billion (earning more interest than they paid)

- Pre-Tax Income: $107.8 billion

- Tax Expense: $19.7 billion in FY 2024

- Net Income: $88.1 billion

Together, these numbers provide a clear picture of Microsoft's financial performance at a glance.

Operating vs. Non-Operating Revenue: Why The Difference Matters

Not all income is created equal. When preparing your income statement, it’s important to separate operating revenue from non-operating revenue. Why? Because they tell two very different stories about your business.

- Operating revenue is what your business earns from its core activities (i.e. what you actually sell). If you run a software company, it’s your subscriptions or licensing fees. This is the bread-and-butter income that shows how well your day-to-day operations are performing.

- Non-operating revenue, on the other hand, comes from sources outside your main business. Think interest earned from a business savings account, money from selling old equipment, or even legal settlements. These aren’t bad: they’re just extra. But since they’re irregular or not tied to your main offerings, they shouldn’t be used to gauge operational health.

Mixing these two can give you a distorted view of how your business is doing. For example, if you show a spike in income because you sold a company vehicle, it might look like you’re growing, when really, that’s just a one-time event. Separating them keeps your income statement honest and useful.

Tips For Preparing Your First Income Statement

There are a number of things to keep in mind when putting together an income statement. Prepare everything according to the book, of course, but also make sure to…

1. Stay Consistent with Reporting Periods

A common mistake when first learning how to prepare an income statement is using inconsistent reporting periods. For instance, you might record your sales revenue for Q1 (Jan, Feb, Mar) but accidentally include some expenses from December of the previous quarter.

Make sure all your reporting periods are consistent!

2. Dial In Your COGS Calculations

Calculating cost of goods sold is a common stumbling block for entrepreneurs. Remember, COGS includes all expenses incurred directly relating to the cost of goods you sell.

If you’re a service provider, COGS is still relevant to you, but it may be called cost of sales (COS) instead. If you’re preparing your financial statements according to GAAP, you may want to look into the differences between GAAP & non-GAAP COGS as well.

3. Use Accurate and Timely Data

Manually preparing income statements doesn’t do you much good if the underlying data isn’t accurate. Make sure you’re following proper accounting standards like GAAP or IFRS and, if you can, consider bringing on a formal accounting department and/or good accounting software.

4. Track Changes Over Time

An income statement looks at a specific period in time, like Q2 of 2024 or FY2025. But to inform financial analysis, it’s beneficial to regularly prepare income statements and track trends over time. This can help influence your strategy, pricing, and expense management for the future.

Sign Up For More Accounting Insights

Learning how to prepare financial reports like the income statement is absolutely essential for business leaders. Income statements can be useful tools to analyze the financial health of your business, identify weaknesses, and tweak your strategy moving forward.

Ready to sharpen your skills as a small business owner? Subscribe to The CFO Club Newsletter for the best insights on operational finance, business intelligence, accounting and more.

{kind=link}