How to Create a Lasting Business Budget in 7 Steps

Is your business budget feeling more like a New Year’s Resolution — set with the best of intentions, only to be forgotten in a few weeks? This guide will help you craft a business budget that sticks (unlike my 2025 meal planning aspirations)...

Business Budget Basics

A business budget is an earning-and-spending plan for your business. On the revenue side, it includes your best-guess estimate of gross revenue (how much money is coming in). On the expenses side, it includes fixed costs, variable costs, capital costs, and non-operating expenses (all the places your business is spending money).

Larger organizations use budgeting and forecasting software to create and maintain budgets, overseen by the CFO. At smaller companies, budgeting might be tackled by the owner and/or accountant.

If you don’t think getting serious about your budget is a big deal, consider this:

- ½ of all small businesses fail to create an overarching operational budget

- ½ of all small businesses fail within the first 2 years

I’ll let you decide if those things are related…

Budgeting’s 5 Main Benefits

Sure, budgeting helps you plan for expenses, shifts in revenue, and more. But beyond the obvious, what are the key budgeting benefits for business owners?

1 - Proactive Staffing

Staffing is one of the biggest stressors for small business owners. I think back to my own experience running a business and how pitiful I used to be at predicting when we’d need to bring on additional help.

This led to myself and my early employees being overworked then, due to an overcorrection, a group of new employees who didn’t have enough to do when things slowed down.

It was rough and lost me a lot of goodwill with some great employees. Learn from my mistakes and get ahead of budgeting early.

2 - Preparing for Financing

Any traditional bank loan will require a detailed business plan, complete with a well-thought-out budget.

While investors may be a bit more lenient, chances are, they’ll want to see a comprehensive operating budget and profitability forecast before handing over their cash.

3 - Lower Financing Costs

If you’ve budgeted effectively, you can also determine the type of financing that’ll save you the most money.

For example, say you have some substantial unexpected costs pop up. You could tap your line of credit, use a credit card, or perhaps even utilize invoice factoring. You check your budget and realize you’re projecting an influx of cash next month with 90% certainty — meaning you need only a short-term funding source.

In this case, rather than going for a loan, you could probably just use a credit card, taking advantage of your grace period to pay no interest for anywhere from 21-50+ days (depending on when in your billing cycle you made the purchase).

4 - Less Stress

Running a business can be stressful. So much so that a survey from Xero found that small business owners had lower “well-being” scores than the general population.

That sucks to see… and is part of why I’m here, writing this kind of thing.

Budgeting can reduce your stress as a business owner and operator by helping you be more prepared for business shifts. I know you already have less time than you’d like but by sitting down and preparing a budget, you can put your mind at ease and prevent backtracking.

5 - More Informed Decision Making

The average small business owner makes over 6 million decisions per year… Okay, maybe not actually but there are a ton of things to decide, which quickly leads to decision fatigue.

Your budget can automate some basic financial decisions — like how much to set aside for your next payroll cycle or whether you can pursue a new opportunity this quarter.

Best Practices for Business Budgeting

A quality business budget should be as accurate and comprehensive as possible. Use these best practices to ensure you’re hitting the mark — and avoiding common budgeting mistakes.

Build a Buffer

Budgets use your best estimates (guesstimates, in some cases) to project figures. It’s a good idea to build a buffer in one of two ways.

1. Inflate Variable Expenses

The first is to simply assume that your variable expenses will run slightly higher (5-10%) than your projections and to build that into your budget.

2. Write a Cash Buffer In

The alternative is to simply keep a cash buffer as a line item on your budget (and an actual cash-equivalent account somewhere) to cover unexpected expenses or revenue shortfalls. I prefer this method, so I’ve included it in my step-by-step process later on in this article.

Use the Right Tools

An Excel spreadsheet is a safe bet for creating your first budget but there are better options out there.

Most accounting software has some assortment of budgeting features if you aren’t ready to spring for specific forecasting software just yet.

Bring In the Experts

If you’re outsourcing your accounting and other finance tasks, it may make sense to draw on expert help to put your business budget together.

If you have any semblance of an internal accounting department, they should 100% be involved here. They’ve been trained on this exact sort of thing, so the best thing you can do is trust them and bring them in.

Learn and Adapt

Your initial business budget may not be right on the money, and that’s okay.

Compare your budget vs. actual financials after the fact, you can draw insights that will help improve future budgeting cycles. This is also a good time to brush up on your financial forecasting skills, learn the golden rules of accounting, or read some beginner-friendly accounting books.

4 Common Budgeting Methods

There’s more than one way to budget — here’s an overview of the best business budgeting frameworks.

Zero-based Budgeting

In zero-based budgeting, your total revenue minus total expenses/allocated savings will equal (you guessed it!) zero.

Does that mean you’re not making any profit? No, it just means that you’re giving each dollar a specific task. A zero-based budget might include line items for “owner draw”, “rainy day fund”, or “holiday office party”. The idea is to allocate each dollar to a specific purpose.

In a business context, these budgets also start from zero — meaning you start from scratch, and you/department managers need to justify each cost, even if it’s recurring. Most early organizations utilize this method.

Incremental Budgeting

Incremental budgeting takes past years’ financial results, and then adds or subtracts as needed to reach the current year’s budget.

For instance, if you’re building a 2025 budget, you’d use actual 2024 data for revenue and expenses. From there, you’d add incremental changes — a projected increase in revenue here, an eliminated expense here — to reach your new budget.

Activity-based Budgeting

Activity-based budgeting analyzes any business activities that have financial costs, recording and researching each expense line-by-line.

It’s a more rigorous process than other business budgeting methods, but it can make sense in circumstances where a company wants to slash costs or uncover inefficiencies in spending.

Participative Budgeting

Participative budgeting involves input from more people than just you and your accountant, such as lower-level managers and department heads.

This gives various stakeholders more ownership in the budgeting process, while still leaving final approval to the higher-ups.

If you have a team that’s been around for a minute now, this method typically proves fruitful, despite taking a bit more time.

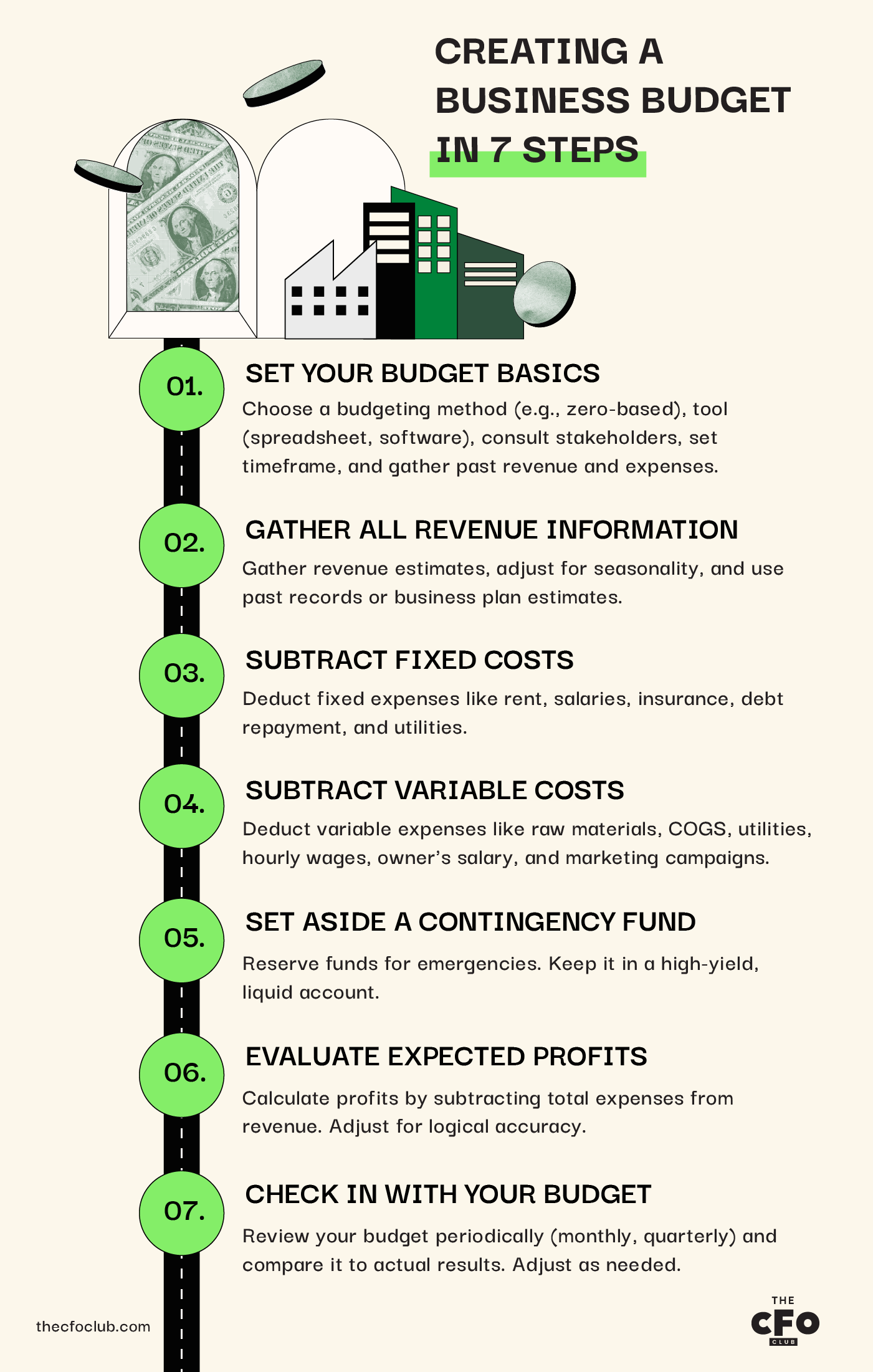

Creating a Business Budget in 7 Steps

Here’s an actionable plan to build your business budget from scratch.

1. Set Your Budget Basics

Before you get started, make sure to:

- Select the budgeting method you’d like to use; as I mentioned, I’ll be covering a zero-based budgeting approach

- Choose a budgeting tool, whether that’s a spreadsheet, software tool, or pen-and-paper (if you want to drive tech-enabled people like me crazy)

- Consult with any relevant stakeholders (your accountant, department heads, etc.)

- Choose the timeframe for your budget planning (quarterly, yearly, etc.)

- Gather past year(s) records for both revenue and expenses

Once you’ve done these, you’re ready to build your budget.

2. Gather All Revenue Information

Your budget should start with an estimate of revenue from all sources you can reasonably anticipate over the period you’re budgeting for (quarter or fiscal year). This is the total revenue generated by your business from all sources, before expenditures.

Word to the wise: Now isn’t the time to be optimistic about new client acquisition. I can’t even count the amount of times I’ve had verbal commitments fall through on me.

For an established business, you can cite revenue from your existing records. For a new business, you can cite estimates from your business plan or industry comparables… but you’ll want to return to this often to see how you’re pacing against the plan.

Make sure to adjust for any seasonality of your business. For instance, if you’re building a Q1 budget for 2025, it might make more sense to use Q1 2024 records, rather than average revenue records for your entire fiscal year.

3. Subtract Fixed Costs

Fixed costs are expenses that stay the same regardless of how much revenue you’re producing. This includes:

- Rent

- Monthly salaries* (*hourly wages can be a variable cost, but paychecks for long-term salaried employees are considered a fixed cost)

- Insurance

- Debt repayment

- Fixed utilities and SaaS tools (WiFi, POS system monthly fees, bookkeeping software, etc.)

Total up your actual fixed costs based on data from past months. Remember to include any fixed but less frequent expenses, like an insurance bill that you pay quarterly or annual property taxes.

Once you have everything together, subtract these fixed costs from your revenue.

4. Subtract Variable Costs

Variable costs are expenses that change from month to month, generally alongside your business’ shifting production or output. This includes:

- Raw materials

- Cost of goods sold

- Variable utility costs like power

- Hourly employee wages

- Your owner’s salary or draw (if it varies with profits)

- Marketing campaigns

Variable costs can be estimated using formulas within your budget (if you’re using a spreadsheet or an advanced budgeting tool).

As variable costs scale up with the output of your business (i.e. the total number of units produced), you can use the total variable costs to define a variable cost per unit and have your cells dynamically update alongside this figure.

5. Set Aside a Contingency Fund

A contingency fund is essentially an emergency fund for your business. It’s there to cover unforeseen expenses, or even routine expenses should your revenue fall short of forecasts.

The amount you keep in your contingency fund depends on the nature of your business, the stability of your revenue, and the quick financing options available to you.

Keep in mind that, once established, you don’t need to repeat this step unless you draw down from the fund. You don’t have to budget for a new contingency fund each quarter or year — you just want to make sure you have some funds set aside for this purpose.

Likewise, the contingency fund isn’t an “expense”, and does not technically reduce your profitability, though I advise calculating it at this stage so you aren’t tempted to use your buffer elsewhere.

What to Do With Your Contingency Fund

Just because you aren’t actively using your emergency fund to grow your business doesn’t mean you should let it sit in a zero-interest bank account.

You should always keep your contingency fund in a highly liquid asset but you may as well earn some yield — so choosing a high-yield business savings account or a money market fund can be a good option.

Just make sure you can access the money quickly, at any time, without hassle or fees.

6. Evaluate Expected Profits

You can calculate your expected profits now that you have your total estimated revenue and expenses.

If the number is positive, you’re in the black and are projecting a profitable year! If it’s negative, you’re in the red. Don’t worry — it’s quite common for businesses to experience periods of net losses.

Why “in the black”?

As we’re talking about money, you might assume that “in the green” makes more sense, and you’d be right… if the term came to be recently. “In the red” is short for “in the red ink”, referring to a time when companies marked down losses in pen.

If it was red, it was bad. If black, it’s still good.

Before you accept this figure as law, make sure the number present makes logical sense. It’s a quick way to check your work and make sure you didn’t leave anything out.

If you draw a variable owner’s salary, you could also wait until this step to determine what that figure is. Just make sure you don’t double up — if you’ve already included an owner’s salary in your variable costs, don’t count it again here.

7. Check In With Your Budget

Budgets should be examined at relevant intervals, such as the end of each month, quarter, or fiscal year. If your business is early-stage and/or rapidly growing, you’ll want to conduct budget checks more frequently.

If you’re creating a business budget for the first time, you should check in at least once per quarter and compare it to your actual revenues and expenses. This can also help you build better forecasts: an accurate budget = more accurate forecasts

If you find that your actuals are substantially off from your estimates, it may be time to reexamine your budget or use a different forecasting model to improve your estimates.

5 Types of Business Budgets

Now you know the business budgeting basics. For a deeper dive, here are the different types of budgets that might be relevant to your company.

Master Budget

A master budget is an overview of projected revenue and expenses from all departments at a company — and what I’ve prepared you to make in this article.

At larger firms, it’s common to have operating budgets for each department or project, plus a master budget that brings it all together.

Operating Budget

Operating budgets are used to estimate expenses and revenues based on the specific operations in question, hence the name.

When your organization is small and you’re pursuing one central goal, the operating budget is the same as the master budget. However, once you grow, you’ll prepare operating budgets for each specific project or department you pursue.

Capital Budget

A capital budget is used to evaluate potential major investments, projects, or purchases. For instance, a company may compile a capital budget to explore opening a second manufacturing facility.

The capital budget would look at the projected expenses and revenues from that specific potential project to gauge its profitability and determine if it’s a good use of the firm’s capital.

Cash Budget

A cash flow budget is an estimation of the cash flow of a business over a specific period (which could be weekly, monthly, quarterly, or annually).

It’s a useful starting point for cash flow analysis and helps ensure a company has adequate cash to continue operations.

Labor Budget

A labor budget is a touch different; it’s a blended finance and human resources tool used to estimate the number of employee or contractor hours required to fulfill a projected output requirement or to hit revenue targets.

It can be useful for estimating labor costs, estimating revenue (if billing clients hourly, for example), and helping HR make more informed staffing decisions.

Better Budget, Better Business

While a budget is just a component of your overall business strategy, it’s a very important one. Running a business without a budget is a bit like baking a cake without a recipe. Sure, it could work — but are you willing to bet on that? Play it safe and bake better cakes achieve better business outcomes with a well-structured business budget.

Ready to compound your abilities as a finance leader? Subscribe to our newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry.

{kind=link}