The 3 Golden Rules of Accounting & How to Use Them

The three golden rules of accounting are fundamental to double-entry bookkeeping.

Luca Pacioli, the father of accounting, codified double-entry bookkeeping and the three golden rules in his mathematics textbook called Summa de arithmetica.

These rules provide the basis for the modern accounting system. In this guide, I help you understand the three golden rules of accounting from scratch.

Types of Accounts

The three golden accounting rules differ based on the type of account you’re dealing with and your overall policies. Luckily, there are only three categories of accounts. They are the:

Nominal Account

Nominal accounts are temporary accounts from which balances are transferred to a permanent account at the end of the accounting period. Think of them as a holding pen for your flock of balances, before they move to their forever pasture.

Income and expense accounts are nominal accounts. Other examples of nominal accounts include rent, interest, and salary accounts.

At the end of the accounting period, nominal accounts are closed by transferring the balances to a general ledger account. The balances in the general ledger account include expenses and incomes, which are then transferred to the profit and loss account (i.e., the income statement).

Real Account

Real accounts typically remain open for longer than one accounting period. They carry balances at the end of the fiscal year and appear on the balance sheet. All assets and liabilities are recorded on the books as real accounts.

Furniture, land, and accounts receivable are examples of real accounts. Here are more examples of the types of entries you might find in a real account:

- Asset-related expenses that must be capitalized, such as freight paid for transporting a new asset to your location.

- Depreciation on tangible assets and amortization or impairment on intangible assets.

- Purchase and sale of assets.

- Money borrowed or repaid.

Personal Account

Personal accounts are the accounts of a real person or an artificial person aka, a business entity (not an imaginary friend). For example, suppose your business borrows money from a friend’s business. You’ll need to record your friend’s company as a lender in your books by creating a personal account for his company.

The Golden Rules of Accounting

With types of accounts out of the way, we can talk about the three golden rules of accounting. There’s one golden rule for each type of account.

According to double-entry bookkeeping, each business transaction impacts at least two accounts. Accounts are either debited or credited based on the transaction and account type, but the amount of debit is always equal to the amount of credit.

A debit entry is made on the left side of an account. Debit entries increase asset and expense account balances and reduce equity, liability, or revenue account balances.

On the other hand, a credit entry is made on the right side of an account. Credits increase revenue, equity, and liability account balances and decrease asset and expense account balances.

Even though accounting software can make accounting entries for you, learning them is important so you understand the logic behind how transactions are recorded.

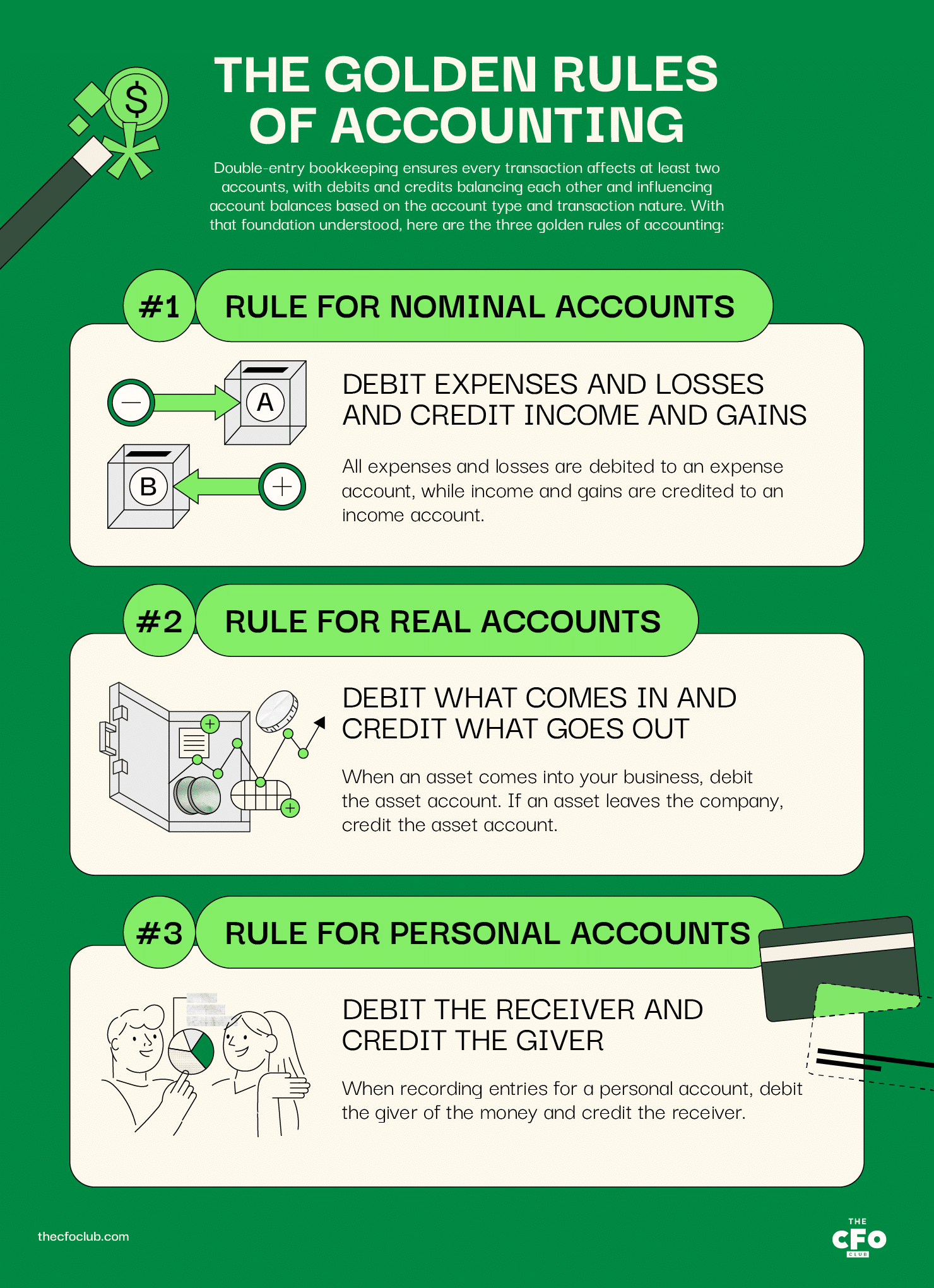

With that foundation understood, here are the three golden rules of accounting:

Rule for Nominal Accounts: Debit Expenses and Losses and Credit Income and Gains

All expenses and losses are debited to an expense account, while income and gains are credited to an income account.

Here are some examples:

- Debit the stationery account when you spend $50 on stationery for your business

- Debit the asset account to record depreciation expense

- Credit the interest account when you receive $100 in interest on the company’s bank deposit

- Credit the sales account when a customer signs up for an annual subscription

Rule for Real Accounts: Debit What Comes in and Credit What Goes Out

When an asset comes into your business, debit the asset account. If an asset leaves the company, credit the asset account.

For example, suppose your business (Company X) borrows money from your friend’s business (Company Y).

Cash is coming into your business, so you’d debit the cash account with the amount of borrowed money.

Here are some more examples:

- Debit the asset account when you spend $5,000 on an asset to improve its efficiency

- Debit the creditor when you repay the money borrowed from them

- Credit the asset account when you sell said asset

- Credit the line of credit account when you borrow money using your line of credit

Rule for Personal Accounts: Debit the Receiver and Credit the Giver

When recording entries for a personal account, debit the giver of the money and credit the receiver.

Let’s use the same example as before.

Company Y has loaned money to your business. To record this, open a new account in your books for Company Y and credit the account with the amount of borrowed money.

Company Y’s account will now have a credit balance and appear as a liability on your balance sheet.

Here are more examples:

- Debit Company Y’s account when your business sells an asset to Company Y and Company Y promises to pay the next year

- Credit Company Y’s account when you borrow additional money from Company Y

- (In the case of a business partnership) Credit your own account in the partnership firm when you lend additional capital to the business

- (In the case of a business partnership) Debit your account in the partnership firm when you withdraw capital from the business

Example of the Three Golden Rules of Accounting

Let’s see an example where we apply all three rules together.

Suppose your friend’s company (Company Y) owes your company $20,000. You’ve decided to acquire used furniture from Company Y to settle the account. The furniture’s current market value is $19,750.

Company Y offers marketing services. Since you need help running ads, you’ve decided to do a $500 pilot project with Company Y to run ads.

After acquiring the furniture and using Company Y’s advertising services, you pay Company Y $250 ($20,000 - $19,750 - $500) in cash.

Here’s what the journal entry should look like:

| Account Type | Account | Debit ($) | Credit ($) | Applicable Rule |

|---|---|---|---|---|

| Real account | Furniture | 19,750 | Debit what comes in | |

| Nominal account | Advertisement expense | $500 | Debit expenses and losses | |

| Real account | Cash | $250 | Credit what goes out | |

| Personal account | Company Y | $20,000 | Credit the giver |

The furniture account, a real account, will appear on the balance sheet.

The advertising expense will appear on the income statement.

Cash will be reduced by $250 on your balance sheet.

And, lastly, company Y will no longer appear as a debtor on your balance sheet.

Advantages of Accounting Rules

In addition to providing a logical framework for the double-entry system, the three golden rules of accounting offer the following benefits:

- Universal structure for recording financial transactions: Every business in every country around the world uses the dual-entry accounting system to maintain their books of accounts; thus, understanding the golden rules of accounting helps financial professionals around the globe understand and interpret financial information.

- Consistent interpretation: Consistency in accounting processes and logic eliminates ambiguity. Adherence to the golden rules ensures that any person who reads the accounting entries clearly understands the transaction.

- Comparability: The golden rules of accounting make the financial statements of the same company over time and the financial statements of other companies comparable.

- Accurate financial statements: The balance sheet needs to tally and the income statement needs an accurate net income figure. The accounting rules help pass accurate entries, so your financial statements are more likely to be accurate as well.

Though not every country around the world follows GAAP (I’m looking at you, U.S.), the golden rules have a lot of similarities in intended effect, helping shrink the differences in global financial reporting.

Who is Required to Adhere to Accounting Rules?

The accounting rules apply to any business that maintains books of accounts… aka, all of them. This differs from other accounting requirements, which typically require less stringent reporting from small businesses than from publicly listed companies.

For example, the IRS allows a corporation or partnership with an average annual gross receipt of less than $27 million in the past three years to use cash-based accounting. Based on your business size, you might need to follow cash, modified cash, or accrual basis accounting.

However, all businesses must still record transactions following the financial accounting rules of the double-entry bookkeeping system.

FAQ

How do you apply the golden rules of accounting?

What are the three types of accounts?

Three Golden Rules Simplified

The three golden rules of accounting are just a simplified framework for accurately recording transactions. You might need some practice to learn these rules but once you’re comfortable with them, you’ll be ready to learn more advanced accounting concepts.

If you want more accounting concepts and insightful articles about finance for SaaS CFOs delivered to your inbox, subscribe to The CFO Club’s newsletter.

{kind=link}