When & How to Do a Cash Flow Analysis for a Healthy Business

Imagine walking around with no real idea how much money you had in your bank account. Every transaction would be a guessing game, wondering when the card would get declined. Besides giving you tremendous anxiety, there are innumerable reasons this is a terrible idea.

Yet, somehow, company operators do this very thing with shocking frequency. If you consider yourself a part of this camp, I’m glad you’re here, reading this. I’ll go over how to do a cash flow analysis (properly) and when you should be doing it.

What is a Cash Flow Analysis?

A cash flow analysis is a method of examining a company's cash inflows and outflows during a specific period; where it comes from, where it goes, where it comes from (Cotton Eye Joe). But actually, it helps you figure out when and why your accounts are filling up and draining.

Besides giving you immense peace of mind, a cash flow analysis provides valuable insights into the company's liquidity, operational efficiency, and financial flexibility so you know just how much room you have to play with.

How to Do a Cash Flow Analysis

Here's a step-by-step guide on how to conduct a high-level cash flow analysis:

- Obtain the Cash Flow Statement: The first step in a cash flow analysis is to obtain the company's cash flow statement which can be accessed from the company's financial statements.

- Understand the Three Sections: The Statement of Cash Flows is divided into three sections: operating activities, investing activities, and financing activities:

- Cash Flow from Operations: This section shows the cash generated from the company's core business operations. It starts with net income (which flows directly from the income statement) and then adjusts for non-cash items (like depreciation) and changes in working capital (change in current assets & current liabilities, not including cash).

- Cash Flow from Investing: This section shows the cash used for investing in the company's future, such as capital expenditures for property, plant, and equipment, cash generated from selling such investments, or cash outflows from purchasing investments.

- Cash Flow from Financing: This section shows the cash transactions between the company and its owners and creditors, such as issuing dividends, repurchasing stock, or borrowing money.

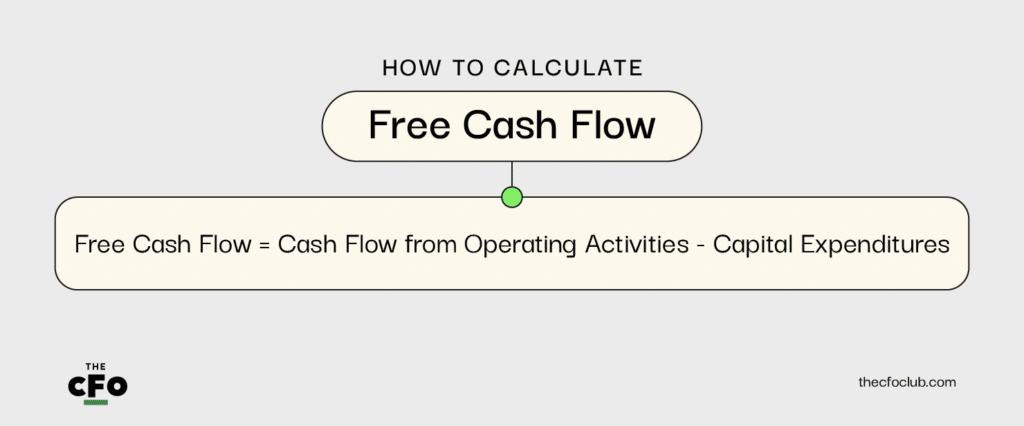

- Calculate Free Cash Flow (FCF): FCF is a key metric in cash flow analysis. It represents the cash available to the company's investors (both equity and debt) after all operating expenses and necessary capital expenditures have been paid. The most simple form of free cash flow is calculated as follows:

- Analyze the Trends: Look at the trends in the company's cash flows over time. Is operating cash flow growing? Is the company investing more in capital expenditures? Is the company generating positive free cash flow? The answers to these questions can provide valuable insights into the company's financial health and operational efficiency.

- Compare with Peers: Compare the company's cash flows with those of your peers. This can provide a benchmark for whether your company is generating a healthy amount of cash relative to your competitors, or if you’re going to be left behind when opportunities arise that need cash. When direct competitors are not available, it is good to look at the trends of similar larger-scale businesses which may have some insights for what cash flows should look like within the industry for a given period.

- Consider the Company's Life Cycle: A company's stage in its life cycle can significantly impact its cash flows. For example, a startup or growth-stage company might have negative cash flows because it's investing heavily in its growth, while a mature company might have positive cash flows.

The Analysis Part of the Cash Flow Analysis

Once you understand the areas of a cash flow and how to do the calculations, you need to make sure you can understand what the net cash flows mean to the business.

Here's how a business can achieve a complete and accurate understanding of its cash position:

Calculate Key Financial Ratios

Certain financial ratios can provide insights into a company's cash position. For example, the current ratio (current assets divided by current liabilities) can indicate whether the company has enough cash to cover its short-term liabilities. The quick ratio (cash and cash equivalents divided by current liabilities) provides a more conservative view of the company's liquidity by only considering its most liquid assets.

Prepare a Cash Flow Forecast

A cash flow forecast is a projection of the company's cash inflows and outflows over a future period. This can help the company anticipate periods of negative cash flow and take steps to manage it. Having a financial model that can determine future cash flows within a somewhat accurate level is incredibly valuable for high-level cash flow management, as forecasts can prevent issues with cash balance, whereas analysis of historical cash flows can only help understand what has already happened.

Understand the Cash Burn Rate

If you operate a business that consistently posts a negative cash flow, whether that be due to not reaching the economies of scale necessary to hit profitability or due to making significant investments within the business to expedite growth, understanding your cash burn rate is crucial to a cash flow analysis.

A cash burn rate analysis determines the length of time that a company has until its cash reserves are used up; in plain English, a cash burn rate tells you how long you can keep on your path until your business goes six feet under. The burn rate tells you how long you have to either start realizing positive cash flows or seek additional financing (whether that be equity, traditional debt, revenue-based debt, or something else entirely).

Monitor Accounts Receivable and Payable

Keeping a close eye on accounts receivable (money owed to the company) and accounts payable (money the company owes to others) can help the company manage its cash flow more effectively. By minimizing the accounts receivable and maximizing the accounts payable, you will be able to maximize the cash available to the business to return to investors or reinvest into the business.

Be wary of playing too much with your accounts payable terms though, as people generally don’t love to work with someone that doesn’t pay them.

Consider External Factors

As you’ve likely already seen, external factors, such as market conditions, industry trends, and economic indicators, can also impact a company's cash position. For example, a downturn in the economy could lead to slower sales, which could in turn impact the company's cash flow. Recent examples of events that would be important to be aware of when it comes to potential cash impacts within the US SaaS market would be the collapse of Silicon Valley Bank. This directly impacted many businesses' access to capital in the short term, and a similar event could result in a major long-term impact on cash balances.

Time to Cash Out

The most important part of doing a cash flow analysis is understanding what will happen to cash in the future based on the known information. By being able to predict the future outlook of cash within a reasonable range, you will be able to have the best information available when making decisions that impact the direction and future of a company.

To receive more step-by-step guidance and expert insights into running the finance function of a SaaS business, subscribe to The CFO Club’s newsletter today.

{kind=link}