Invoice Factoring: Guide + Calculator for Tech Firms

Calculate Before You Buy: An invoicing factoring calculator helps SaaS firms quickly estimate costs and benefits, simplifying the decision-making process as they navigate tight funding situations.

Navigation Made Easy: When using an invoicing factoring calculator, always make sure you input the correct information and double-check your results. Then, compare costs among providers to find the best fit for your business.

It's Not For Everyone: Before committing to invoice factoring, remember to always consider your payment terms and do your research. This way, you can be sure that invoicing factoring is right for you.

With funding still tight and interest rates high, many SaaS firms are turning to invoice factoring for liquidity. However, costs can be complex. That’s where an invoicing factoring calculator comes in handy.

To help companies estimate costs and benefits—without giving up equity or taking on more debt—I built an invoicing factoring calculator that’ll break down costs for you within seconds. In this article, not only do you get access to the calculator, but you’ll also learn key insights into how invoice factoring works in accounting, the benefits, and more.

So, let’s get started.

What is Invoice Factoring?

Invoice factoring is a form of rapid financing that allows you to get immediate cash for your unpaid invoices. Note that this is for standard outstanding invoices, not overdue receivables or questionable debts.

With invoice factoring, you essentially “sell” invoices to a factoring company, typically referred to as a factor. The factor sends you cash upfront (often within a day or two), then collects payment from your customer once the invoice is paid. The factor charges a fee, often in the range of 2-5% of the invoice value.

Factoring has long been popular in industries such as heavy transportation, but it’s now gaining steam in tech circles as well, particularly with small business inventory factoring.

For SaaS firms, factoring can improve cash flow, particularly for B2B providers who often have longer payment terms (compared to consumer SaaS tools). Plus, factoring can be cost-effective for enterprise and SMB SaaS firms, especially in today’s interest rate environment.

Invoice Factoring Calculator

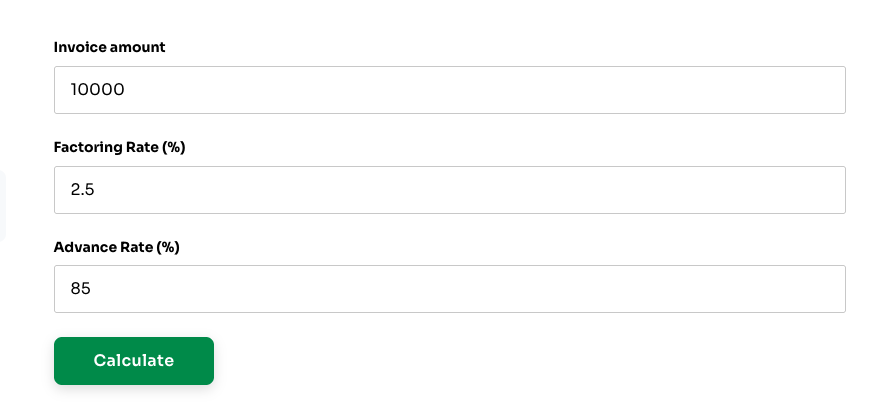

Below is my completed invoice factoring calculator. If you already know how to use one and interpret the results, continue on. If not, I created a step-by-step guide to help you through the process (see below).

How to Use the Invoice Factoring Calculator Effectively

Now that you know all about invoice factoring and how a calculator can help, here’s some practical tips you can use to get the most out of my invoice factoring calculator:

1. Input the Correct Data

Before you start using the calculator, make sure to gather all the relevant information necessary. For this calculator, you’ll need the following:

- Invoice Amount ($)

- Factoring Rate (%)

- Advance Rate (%)

It’s important to make sure the numbers you use are accurate before hitting 'Calculate'. Otherwise, you’ll get an inaccurate result.

In the example below, our invoice amount is $10,000 with a factoring rate of 2.5% and an advanced rate of 85%.

2. Interpret the Results

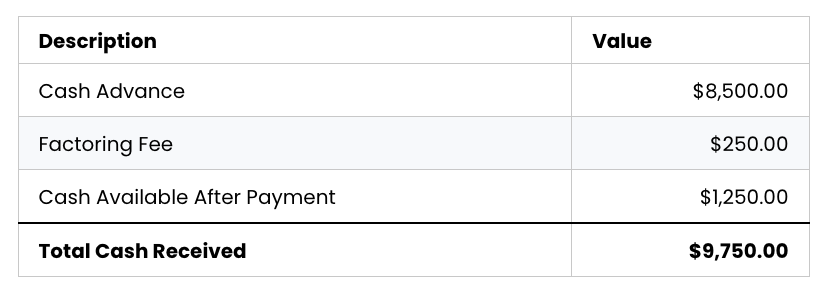

Once you run the invoice factoring calculator, you’ll get a result with the following titles. Here’s what they mean:

- Cash Advance: The upfront amount you’ll receive from the factoring company (less fees). This is often 70-95% of the invoice value.

- Factoring Fee: The amount of the invoice value held in reserve by the factoring company.

- Cash Available After Payment: The estimated cost of factoring, based on the data you’ve provided.

Using the example from before, here’s what the output would look like:

3. Compare With Other Options

Just like with anything else in life, it’s best to compare estimated factoring costs with expected costs for other forms of financing. You can also obtain direct quotes from factoring providers to ensure that you’re getting the best deal for your business.

Why an Invoice Factoring Calculator is Essential

Invoice factoring rates are based on several factors (discussed below), which makes them somewhat difficult to estimate. An invoice factoring calculator cuts out the guesswork and provides accurate estimates, without the need to formally apply for multiple factoring agreements.

Factoring is a highly responsive form of funding. Once an agreement is established, factoring takes just days to free up working capital. But it’s not always the most cost-effective option — and this calculator lets business finance leaders quickly gauge this funding method compared to other forms of financial leverage.

Say you’re facing a shortfall in your quarterly budget. You have a few options:

- Draw on an existing line of credit

- Reallocate projected spending to cover the shortfall

- Get an advance on your accounts receivable via factoring

Borrowing costs for a line of credit are crystal clear. For factoring, not so much — unless you have an accurate invoice factoring calculator. Invoice factoring calculators allow strategic CFOs to quickly and easily estimate costs to weigh the pros and cons of cash infusion via invoice factoring.

Factors that Influence Factoring Rates

Several variables go into determining factoring rates. This invoice factoring calculator uses estimates to determine an expected range of rates, but ultimately you’ll have to receive a quote to know your exact rate.

Here are the primary factors that influence factoring rates:

Invoice Value

Generally speaking, larger invoices and higher overall factoring-eligible receivables volume will result in lower factoring rates. Just like any other business, factors want to deal with fewer customers in greater magnitudes.

Customer Credit and Payment History

Factoring companies look at the credit information and payment history of your customers more than your company’s own credit. Rates will be lower for firms whose customers have good credit ratings.

Industry

Factors assign different risk levels to different industries, with “safe” industries enjoying lower overall factoring rates.

Your Credit History

Though it’s less important than customer credit, factors will also likely look at your company’s own credit history and rating as a worst-case metric.

Invoice Terms

The length and payment terms of your invoices will affect rates, with longer payment terms generally translating into higher factoring rates.

Business Metrics

Factors might also look at various business metrics, including gross sales and profitability measures. This is especially true for small businesses or startups.

Overall, factoring is less concerned with your firm’s overall creditworthiness, compared to traditional financing options. Rates are determined more by the invoice specifics, and the creditworthiness of your customers.

Key Factoring Terms & Specifics Every CFO Should Know

Invoice factoring isn’t overly complicated, but it does differ quite a bit from more traditional forms of financing. This section will break down the key terms you need to understand before factoring.

- Factoring Company (or factor): This refers to the financial services provider that offers invoice factoring as a service. Most factoring companies are specialty providers; we’re not yet seeing most big financial institutions dabbling in invoice factoring (though that could change).

- Factoring Fee (or discount rate): This is the primary fee paid to factor an invoice. It’s a flat fee, not an APR range. A 3% discount rate means that a factor would pay you $97,000 on a $100,000 invoice. For SaaS firms, typical invoice factoring rates are often in the 1-5% range, though this depends on a number of factors.

- Service Fee: A separate administrative fee that some factors charge. Some factoring companies don’t have a service fee, or include it in the discount rate.

- Advance Rate: The percentage of the invoice’s value that you can receive as a cash advance. This is often in the 70-95% range. The remaining amount (less fees) will be paid out once the factor has collected payment for the invoice.

- Reserve Amount: The amount of the invoice that’s held in reserve by the factor until the invoice is paid by the customer. In the previous example, the reserve amount was $7,000. The reserve (less fees) will be transferred to you once the factor collects final payment.

- Recourse Factoring: The most common type of factoring offered. With recourse factoring, you are ultimately responsible if your customer fails to pay the invoice. The factoring company will attempt to collect, but if it fails to do so, it can legally require you to buy the invoice back and attempt to collect payment yourself.

- Non-Recourse Factoring: The opposite of recourse factoring. In non-recourse factoring, the factor takes on the risk of non-payment by the original customer.

Making an Informed Choice: Things to Remember

Before you move forward with invoice factoring, there are a few things to consider.

- Consider Your Payment Terms: If you’re constantly running into cash flow issues, it may be wise to reconsider the payment terms you currently offer. You could even move to a cash discount model, or a 1%/10 net 30 model that rewards prompt payment (which would still be more cost-effective than factoring).

- Choose a Reliable Factor: As mentioned, major players in the financial services industry are not typically involved in factoring. Instead, a wide variety of upstart nonbank financial institutions serve the market — and they’re not all reliable. Look for a firm with a good reputation in the industry, and be sure to read the fine print before entering an agreement.

What’s Next?

Want to further your career in corporate finance? Sign up for The CFO Club newsletter.

{kind=link}