7 Business Tax Planning Strategies That Keep Your Profits, Yours

Tax Jargon is a Puzzle Adventure: Business tax planning can be complex, with various forms and rates. Understanding the basics can benefit all companies, but especially small businesses and startups.

Claim What You Can, Where You Can: Even if it's small, a tax break is still a tax break. Make sure to claim everything you can, such as a home office space or startup costs to lower your return costs.

Don't Wait : Never wait till the last minute to claim your taxes. Staying on top of your finances can help you remain compliant and make the entire process smoother.

Business tax planning can be intimidating for companies of any size. There’s no single tax form or even a single tax rate that applies to all businesses, and while tax experts can help you navigate these complexities, it’s often best to equip yourself with some basic tax knowledge. This is especially true if you own a small business or startup.

In this guide, I use my extensive experience in accounting and financial operations to explain seven tax planning strategies and mistakes you should avoid in the process. By understanding these strategies, you’ll be able to make informed decisions that optimize tax efficiency, reduce liabilities, and ensure compliance, ultimately strengthening your company’s financial health.

What is Business Tax Planning?

Business tax planning is the process of strategically using tax laws to adjust taxable income. Here are some basics:

- C corporations pay a corporate tax of 21%.

- Sole proprietorships, partnerships, and S corporations are pass-through entities—their income is taxed at the owner’s personal tax rate, which can be between 10% and 37%.

- LLCs have the option to pay taxes either as a corporation or pass-through entity.

However, tax laws give you five levers to influence your tax liability:

- Tax Deductions: Deductions include business expenses you’re allowed to deduct from revenue when calculating taxable income. Operating expenses, depreciation, and insurance premiums are examples of tax deductions.

- Credits: Tax credits reduce your tax burden. Credits can be of various types, including investment tax credit (ITC), research and development credit, and disabled access credit. Deductions reduce your taxable income, while credits reduce your tax liability and have no effect on your taxable income.

- Exemptions: Exemptions reduce taxable income, like deductions. However, they’re different because deductions are expenses, while exemptions are incomes. For example, interest on municipal bonds or specific types of government grants may be exempt under specific circumstances.

- Income Shifting: You can shift your income to a lower-tax-rate entity or individual to reduce your business’s tax liability. For example, you can pay your spouse a salary for work performed in the business or transfer income from a corporation to your partnership that pays tax at a lower rate.

- Incentives: The government offers various tax benefits to encourage certain activities and behaviors. For example, the government may tax capital gains or income from exports at a lower rate than ordinary income.

Any business tax planning strategy you or a consultant develops includes a combination of the above.

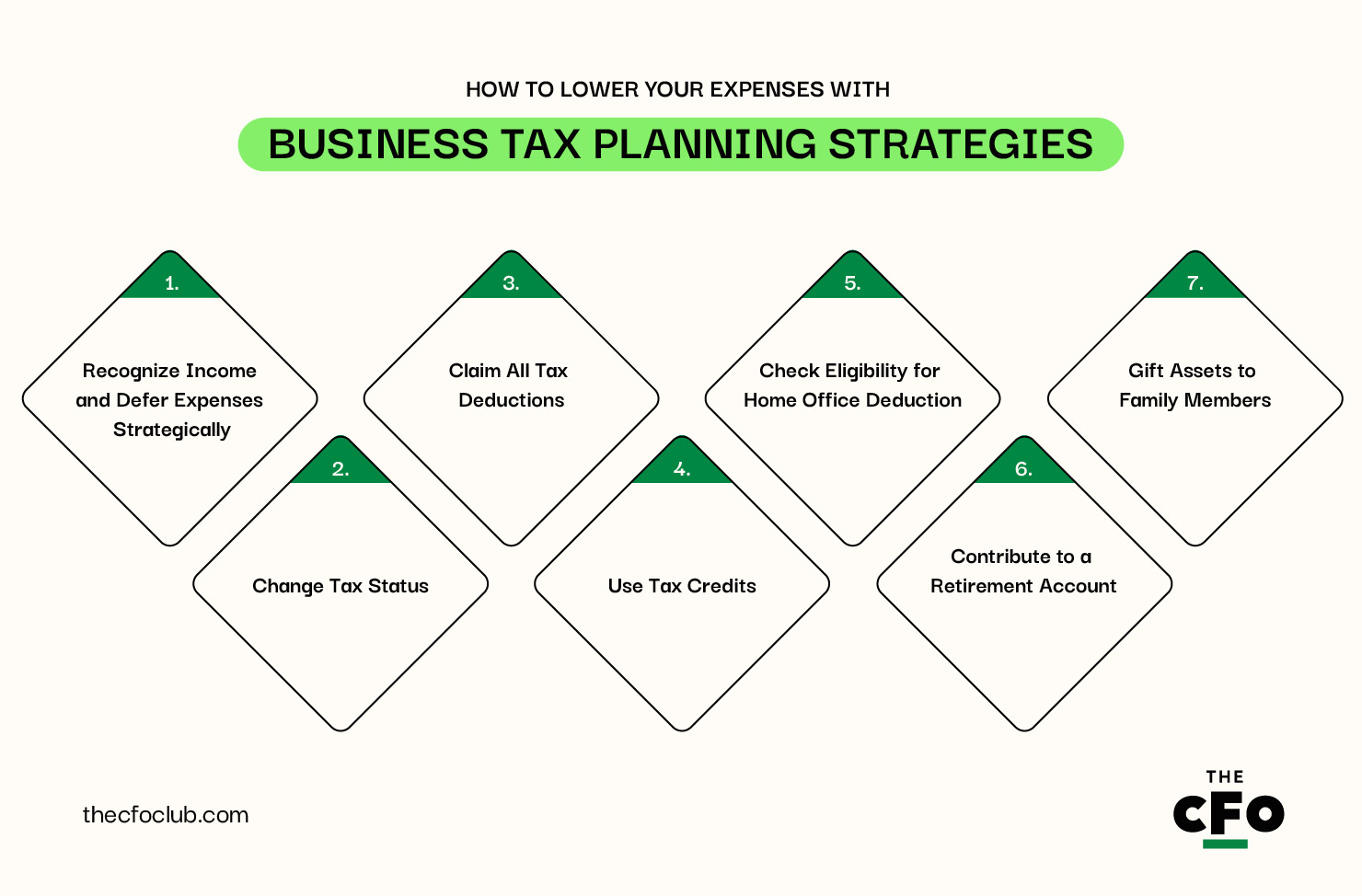

How to Lower Your Expenses with Business Tax Planning Strategies

Now that you know the types of tax benefits you can get, let’s talk about specific strategies you can implement. You can implement some of the strategies a few days before you file taxes, while others require months of planning.

1. Recognize Income and Defer Expenses Strategically

The more gross income you realize during the current year, the more tax you pay at the end of the year. Deferring income not only reduces your tax bill but also helps normalize your income between an unusually successful year and an average year.

However, this strategy isn’t always an option because:

- For Cash-Based Businesses: Transactions are recorded when an expense is paid or income is received. This means that if you want to defer income or expenses, you can just hold off on receiving or paying cash.

- For Accrual-Based Businesses: Transactions are recorded when the income or expense accrues. It’s a little more difficult for companies to control when income or expenses are recorded using accrual accounting. You’ll need to change the date of rendering the service or delivering the product. These dates are often part of the contract and are more difficult to change.

If you operate on a cash basis for tax purposes, here’s what you can do:

- During a Low-Profit Year: Suppose you’ve had a slow year, but you expect things to be a lot better next year. In that case, you can speed up collections before the year ends to avoid getting taxed in a higher tax bracket the next year. Similarly, you can delay paying expenses until the next year begins so you can lower your taxable income.

- During a High-Profit Year: On the other hand, if you’ve had a stellar year, consider deferring revenue to next year and making some advance payments towards next year’s expenses.

2. Change Tax Status

Changing your business tax status can offer various benefits. For example, you can convert to an LLC and file Form 8832 with the IRS to choose to be taxed as a C corp, which is taxed at the top corporate income tax rate of 21%. This can translate to significant savings if your personal tax rate is near the top rate of 37%.

Similarly, you can choose to be taxed as a passthrough entity (PTE). Doing this allows you to claim a tax deduction on your federal return and reduce the owners’ or partners’ taxable income on the federal K1. This will also generate a tax credit to owners or partners, allowing them to reduce their personal state income tax, subject to state-wise limitations on using PTE credits.

3. Claim All Tax Deductions

Many businesses overlook many tax deductions, either due to a lack of awareness or because they’re not sure what they qualify for when filing tax returns. Here are some of the most underutilized deductions you should be claiming:

- Startup Costs: New businesses can deduct up to $5,000 in startup costs and $5,000 in organizational costs incurred before the company starts operations. Market research expenses, legal fees, and other startup costs are deductible under Section 195 of the Internal Revenue Code.

- Charitable Contributions: If you’ve made charitable contributions to qualifying organizations, including money, property, or even inventory, you can claim that as a deduction from your taxable income. Charitable contributions are deductible under Section 170 of the Internal Revenue Code.

- Qualified Business Income Deduction (QBI): QBI is available under Section 199A of the Tax Cuts and Jobs Act (TCJA), 2017 if you have qualified business income from a domestic business operated as a pass-through entity. This includes sole proprietorships, partnerships, S corporations, and some trusts and estates. Ask your tax consultant if you’re eligible to claim this benefit.

4. Use Tax Credits

Corporate taxpayers have various options when it comes to tax credits. Depending on your eligibility, here are some types of credits you may be able to claim:

- Small Employer Pension Plan Startup Cost Credit: If you’re a small business owner and your business didn’t have a pension plan for the previous three tax years, you can claim a nonrefundable tax credit for money spent on creating an employee retirement plan.

- Research and Development Credit: Did you spend money on developing a new product, process, or technology? You may be eligible for an R&D tax credit.

- Energy Investment Credit: If you’ve made investments in alternative and renewable energy properties or production facilities, you may be eligible for a tax credit.

- Employer-Provided Child Care Credit: You may claim up to $150,000 of credit for providing childcare facilities or assistance to employees.

There are many tax credits available to U.S. businesses, but the eligibility requirements differ for each one. Seek your tax consultant’s help to identify tax credits you may be eligible for.

5. Check Eligibility for Home Office Deduction

If you work from home frequently or run your business out of a home office, you can claim eligible home office-related expenses as deductions when you file business tax returns.

However, there are a few conditions to fulfill before you claim these deductions. For example, the space must be used regularly and exclusively for business purposes. So if you’re using a desk in your bedroom as a home office, only that portion of the room qualifies as a home office.

Ultimately, there are two methods used to calculate home office deductions:

- Simplified Method: The simplified method involves determining the home office’s square footage and multiplying that by $5/square foot as prescribed by the IRS. The maximum deduction here is $1,500, which means you can claim this deduction for your home office up to 300 square feet.

- Actual Expense Method: This method can help you claim a larger deduction but requires a more detailed calculation. The first step is to calculate the percentage of the square footage of your home office in relation to the entire home.

Suppose that’s 40% for company A. Next, sum up all the eligible expenses (such as mortgage rent, property taxes, and repairs). Assume the total expenses are $1,000. Finally, calculate the deduction by multiplying total eligible expenses by the percentage of home area used for business. In case of company A, the deductible expenses would be $400.

6. Contribute to a Retirement Account

Contributions made to retirement savings plans like IRAs and 401(k) for yourself or your employees may be tax-deductible. When you match the employee contribution to a retirement plan, you don’t pay payroll taxes.

This makes retirement plans a more tax-efficient way to compensate your employees. In addition to a deduction, contributions to a 401(k) or simplified employee pension (SEP) plan also earn you tax-free credits, provided you meet the conditions in the federal tax code.

If you’ve already missed the cutoff date for the 401(k) plan for the current year and want to be able to claim a deduction in the new year, speak to your tax consultant about SEP. You can make contributions to SEP until the due date of your return and claim them as deductions.

7. Gift Assets to Family Members

The increased estate and gift tax exemption, which is currently $13.61 million per person, is about to be cut roughly in half by the end of 2025. If you’ve been considering transferring any wealth or assets to beneficiaries, now is a good time. Of course, you’ll need to discuss with your tax consultant the exact method to execute this strategy.

For example, you may transfer shares without voting rights to your children to move assets out of your estate, but reserve all decision-making power with yourself until your children come of age. These strategies require time to execute, so ask your tax consultant about what makes sense in your case as early as possible.

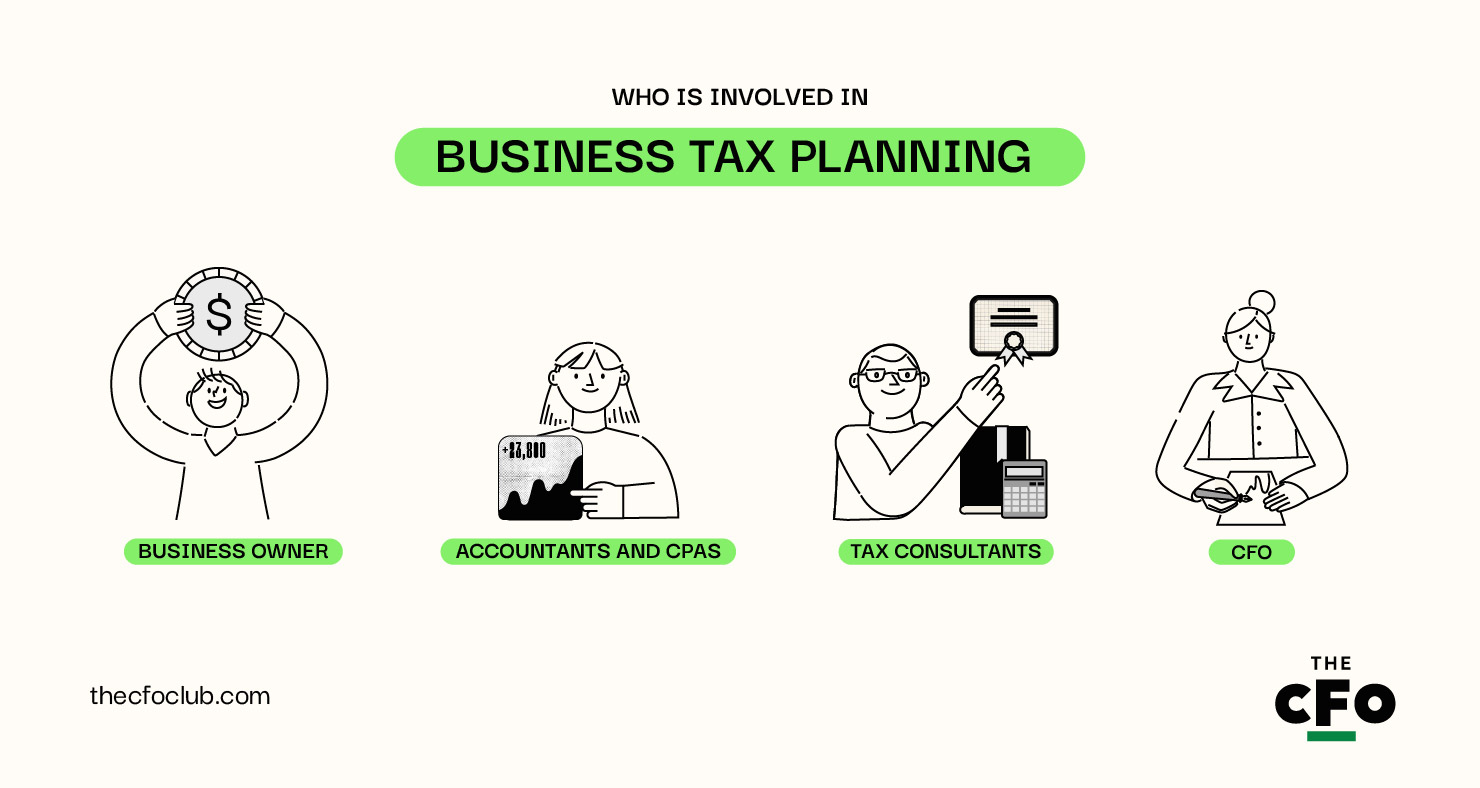

Who is Involved in Business Tax Planning?

Business tax planning involves several individuals and entities. They collectively devise tax strategies that minimize tax liability while ensuring compliance. Here are the main participants involved in business tax planning implementation:

Business Owners

Business owners actively participate in the company’s tax planning strategy, especially in the case of a sole proprietor, partnership firm, or LLC. Owners or promoters of large corporations may not be as involved—they rely on the expertise of their in-house tax experts, the CFO, and the CEO to make tax-related decisions.

Accountants and CPAs

Accountants and CPAs are experts in tax law, financial planning, and small business accounting. Our extensive knowledge allows us to devise optimum tax strategies while considering other aspects of business.

CPAs that offer tax consulting services can be excellent partners who help not just with tax planning but also offer valuable insights about other financial aspects of your business.

Tax Consultants

Tax consultants specialize in tax planning and can provide advanced strategies to minimize your tax liability. They attend tax conferences and stay current with tax law changes, which enables them to offer advice on the implications of those changes for your business.

Some tax professionals specialize in a specific area, such as international tax or estate planning. If you’re looking for guidance on the most complex topics, partnering with a specialist can yield great results.

CFO

The CFO is responsible for the company’s long-term tax strategy. The CFO works with tax consultants and other executives to develop a tax strategy for the long term and ensures the strategy aligns with the company’s financial goals.

For example, the CFO might be involved in discussions related to tax-efficient business structures, mergers and acquisitions, and international operations.

Best Business Tax Planning Tools

Tax software makes the process of preparing tax returns faster and easier. You still need input from tax experts, but different software can help you skip some of the legwork. Here are some of the best tax tools on the market:

Tips to Avoid Business Tax Planning Mistakes

Having the right people on board for tax planning is mission-critical. However, there are a few inherent pitfalls in the tax planning process. Make sure to avoid the following mistakes when developing your tax strategy:

1. Steer Clear of Analysis Paralysis

Lack of direction can lead to indecision. Analysis paralysis is common in tax planning because tax laws often require calculating tax liability under various circumstances to identify the best option. Instead of navigating through these complexities yourself, seek help from a tax consultant who has experience in tax planning for businesses in your industry. A tax planner’s fee may seem steep if you’re a startup, but it will pay dividends in the long term.

2. Don’t Wait Until the Last Minute

Tax planning is an extensive process. You’re more likely to plan poorly or fail to meet the deadline if you don’t plan and implement your tax strategy throughout the year. Spend a few hours with your tax advisor every month instead of pulling all-nighters during the tax season.

However, if you expect to miss the deadline, submit Form 4868 with the IRS before the deadline or make an electric extension payment online. It’s best to also make a partial tax payment based on your estimated tax liability when asking for an extension. If you don’t give the IRS notice, be prepared to pay a penalty of 5% of unpaid taxes per month.

3. Prepare Yourself Before Meeting the Tax Planner

If you’re just following your tax advisor blindly, you’re doing it wrong. Take charge of your tax strategy and invest time in understanding how things work. When you meet with your tax planner, go with a list of questions. Spend a few hours before the meeting to prepare questions regarding your current tax strategy.

Are there any changes in the tax law you need help understanding? Do you have suggestions on how to optimize the current tax strategy? Maybe a friend shared some advice and you’d like to explore that further. Have these details and questions in a document so you can ask the right questions.

What’s Next?

Looking for more tax-related advice? Subscribe to our free newsletter to receive weekly insights from industry leaders and finance experts in your mailbox.

{kind=link}