Cash Flow Forecasting: How It Can Make or Break a Business

Cash Flow Advances: Cash flow forecasting can be a challenge, even for seasoned professionals. A clear, accurate forecast is crucial to avoid financial surprises and keep business momentum going.

Proactivity Pays Off: Forecasting allows you to see cash issues before they occur, ensuring you can tackle them early, handle working capital, and make informed budgeting and investment decisions.

Prioritize Cash Reserves and Seasonality: Avoid overestimates and plan for seasonal fluctuations by maintaining a cash reserve, ensuring stability and preventing financial crises.

If you struggle with cash flow forecasting, you’re not the only one. Many business owners, finance managers, and even seasoned professionals find it challenging to get right.

I’ve spent years working at the intersection of finance and content creation, helping teams simplify complex processes—and cash flow forecasting is one of the most common stumbling blocks I’ve seen.

The truth is: without a clear forecast, even a thriving business can run into surprises that stall momentum. If you’ve ever found yourself second-guessing your financial projections or scrambling to make sense of your numbers, this guide is for you.

In it, I’ll walk you through what goes into a cash flow forecast, how to build one that’s actually useful, and how to sidestep the most common missteps. You’ll also get a practical examples to help you get started right away.

What Is Cash Flow Forecasting?

Cash flow forecasting is about predicting how much money your business will receive and pay out over a set period. Done right, it can help you manage cash better and make smarter decisions.

Think of cash flow projections like road trips. The money your business gets (inflows) is fuel, the money it spends (outflows) is the distance travelled, and the cash flow forecast is the GPS that helps you plan the journey.

In small businesses, cash flow forecasts are usually handled by the owner or CEO. With bigger companies, though, the finance manager or CFO typically takes charge.

Everything Included in a Cash Flow Forecast

Before you start building your cash flow forecast, you’ll need access to a few numbers:

- Opening Balance: The amount of cash your business has at the start of the forecast period.

- Cash Incoming (Receipts): All the money expected to come into your business, including customer payments, loan proceeds, and accounts receivable. This is also known as cash inflows.

- Cash Outgoing (Payments): All the money going out of your business, also known as outflows. This includes expenses like rent, salaries, loan repayments, supplier payments, and accounts payable.

- Closing Balance: The cash balance left in your bank accounts at the end of the period, after accounting for all income and expenses.

- Assumptions: The expectations or estimates you've made when creating the forecast, such as payment timings, sales growth, or seasonal changes.

-

Workday Adaptive Planning

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.4 -

Creatio CRM

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.7 -

Rippling Spend

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.8

{kind=link}

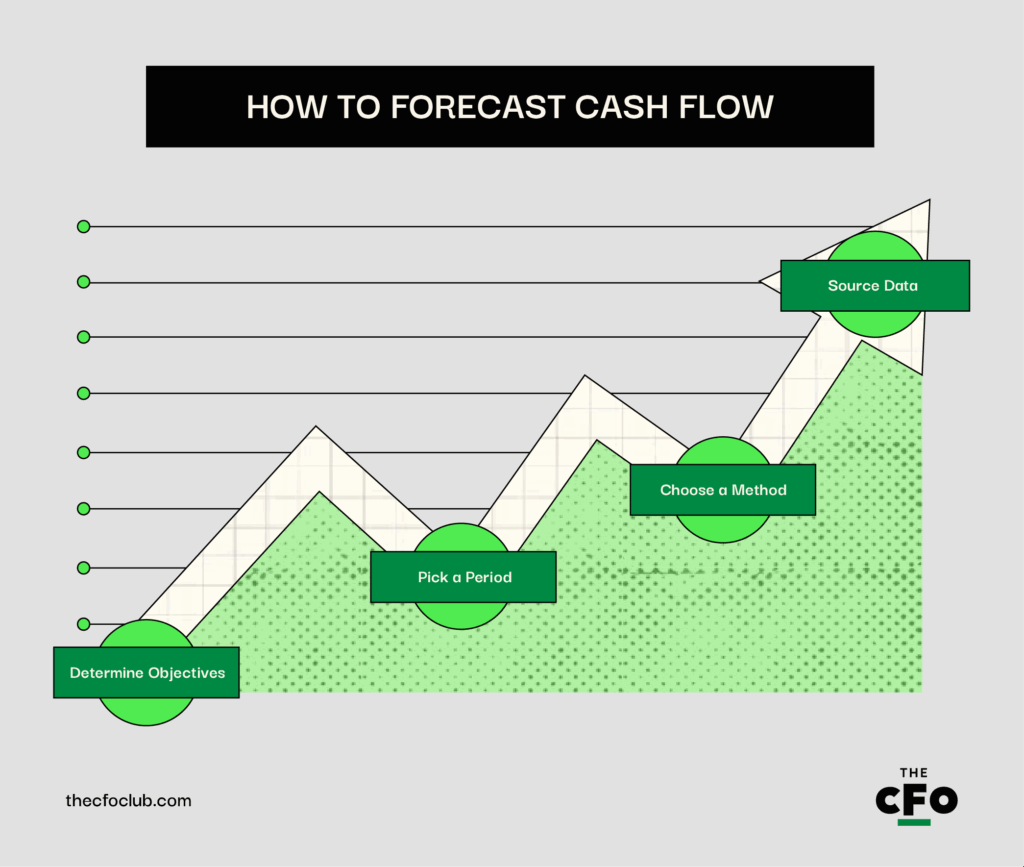

How To Forecast Cash Flow

To accurately forecast cash flow, you'll need to determine your objective, pick a reporting period, choose a method, and source your data. While it sounds simple in theory, it can get complicated. Here's a breakdown of how to get the most out of your cash flow forecast:

1. Determine Your Objectives

The first thing you need to do ahead of any financial forecasting task, is set goals. Common questions to consider are:

- Why are you making a cash flow forecast in the first place?

- Do you need it for short-term liquidity planning, interest and debt reduction, covenant and key date visibility, liquidity risk management, or growth planning?

Your reason will guide you on which forecasting models to use, what you include, and how detailed it should be.

For example, if your goal is to manage short-term liquidity, you might track metrics like operating cash flow and accounts payable turnover. If you're planning for growth, you'll likely focus on revenue projections, capital expenditure, and cash burn rate.

2. Pick a Period

The next step is to decide on your forecasting period. This can be short, medium, long, or mixed. Let’s touch on these timelines and the importance of each.

| Period | Time of Completion | Timeframe | Who It’s Best For | Use Case | Benefits |

| Short Period | Daily or Weekly | 1-13 weeks | Businesses with tight cash flow or lots of daily activity | Helps you keep a close eye on short-term cash flow | Great when you need to make sure you can pay salaries, bills, or restock inventory soon |

| Medium Period | Monthly | 3-6 months | Most small to mid-sized businesses | Gives you a clear look at your actual cash flow over the next few months | Helps you spot cash gaps early and plan for things like tax payments or slow seasons |

| Long Period | Quarterly or Annually | 6-12+ months | Strategic planning, large investments, informed decision-making, and growth | Less about daily decisions and more about big-picture planning | Useful if you’re thinking about hiring new staff, opening a new branch, or getting funding |

| Mixed Period | Mixed | Combination (e.g., weekly for 1 month, then monthly for the next 11 months) | Businesses that need both short-term control and long-term vision | Allows you to watch your cash closely now and still keep an eye on future activities | Helps you optimize resource allocation, reduce liquidity risk, or manage debt |

3. Choose a Method

Once you’ve picked the period for your forecast, it’s time to choose your forecasting process or method. There are two main ways to forecast your cash flow:

Direct Forecasting

This method uses real numbers, like your current bills, invoices, and bank statements, to figure out exactly what money will come in and go out. It shows your actual cash position and helps you see whether you’ll have enough cash for expenses.

How To Use It: You look at customer payments, salaries, rent, and other upcoming transactions and plug them into your forecast week by week. This method is best for short-term forecasting (1–13 weeks).

Indirect Forecasting:

This forecasting process uses accounting data, like your profit and loss statement, balance sheet, and changes in assets (such as accounts receivable) and liabilities, to estimate your future cash flow. It’s not based on day-to-day bills or payments, but on bigger financial trends in the business, giving you a long-term view of your cash health.

How To Use It: Take your projected sales, expenses, and changes in assets or liabilities and use that information to figure out how much cash your business will likely have over time. It’s best for medium to long-term forecasting (3 months to 12+ months).

4. Source Necessary Data

Now it’s time to gather the information you need to build your cash flow forecast. Here’s where you can expect to find the data:

Cash Incoming (Receipts): This is the money you expect to receive. You can find this information in the following:

- Sales records (from your POS or invoicing software)

- Customer payment history

- Contracts or signed orders

- Loan disbursements or investor funds

- Tax refunds or grants

Cash Outgoing (Payments/Expenses): This is the money you expect to spend. You’ll usually include:

- Past utility bills, rent, and salaries

- Supplier invoices

- Loan repayment schedules

- Subscriptions and software costs

- Tax obligations and insurance

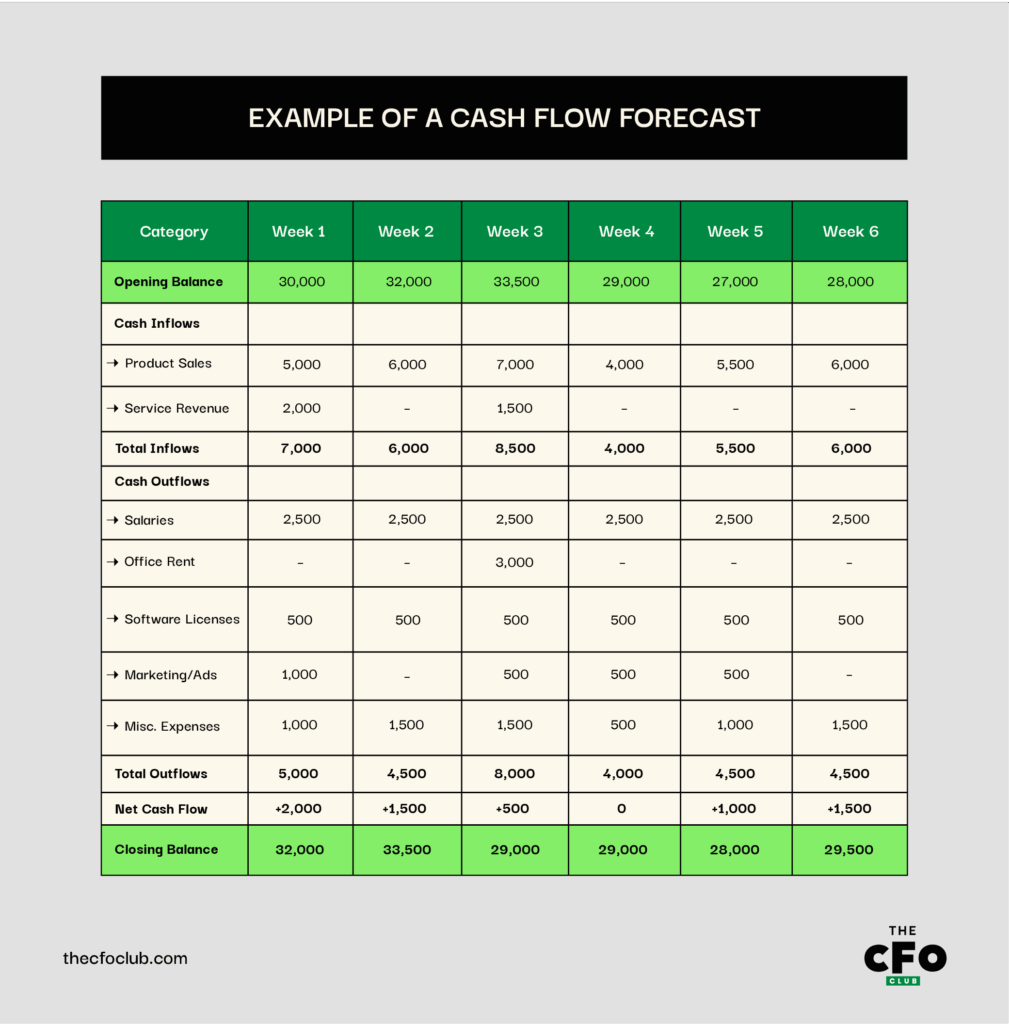

Example of a Cash Flow Forecast

Now that you know the theory, let’s put it to visual practice.

Say you’re building the cash flow forecast for a small tech company. Your business is still in its growing phase, so you opt to use the short period and forecast weekly. In addition, you choose to use the direct forecasting method. Here’s how your forecast may look:

This is a pretty standard and straightforward example. If you’re building the forecast for a larger corporation, you’d likely use the long period and indirect forecasting method, which would include more data and further explanation/rationale.

-

Workday Adaptive Planning

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.4 -

Creatio CRM

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.7 -

Rippling Spend

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.8

Benefits of Cash Flow Forecasting

Proactive Financial Management

Cash flow forecasting helps you see money issues before they happen, so you can fix them early. Instead of being surprised by a low bank balance, you’ll know what’s coming and can plan for it.

It works hand-in-hand with your cash flow statement, giving you both a historical view (what’s happened) and a forward view (what’s likely to happen).

Better Working Capital Management

Cash flow forecasting helps you manage the money you need to run your business every day, like paying bills, buying supplies, and covering wages. It makes sure you always have enough cash to keep things moving.

In a recent conversation I had with Chris Ortega, CEO and Fractional CFO of Fresh FP&A, he stated the following:

Profits are a dream but cash is a reality.

And he’s absolutely right. What you have in the bank is more important than what you want to achieve. An accurate forecast helps you plan when to pay suppliers so you don’t run out of money for the things you need to make that profit dream come true.

Smarter Budgeting and Planning

When you understand how much money is coming in and going out, it’s easier to budget and plan smartly. You know how much to spend, when to invest, or when to cut back.

For instance, if you check your cash forecast and see that you can afford a marketing campaign in May, but not in April, you wait until the right time to avoid going over budget.

Stronger Finance to Business Partnerships

With accurate forecasts, finance teams can offer timely insights that help leaders make confident, well-informed decisions about hiring, investments, or operational changes.

This helps build trust and shifts finance from being seen as just a reporting function to a true strategic partner. It also encourages more regular, collaborative conversations between departments, aligning financial realities with business goals.

Common Cash Flow Forecasting Mistakes (+ Tips)

Everyone makes mistakes. Here are a few common cash flow forecasting errors that can occur, and tips on how to avoid them:

Overestimation

It’s easy to get too hopeful and think all your customers will pay on time or expect higher sales than usual. This is an overestimation. It makes your forecast look better than it really is, and can lead to overspending, missed bills, or even not having enough cash to cover payroll.

Here’s how you can avoid it:

- Be realistic. Use past data, not just hopes.

- If a customer usually pays late, plan for that delay.

- Lower your expected income slightly to stay on the safe side.

- Build in a “buffer” just in case cash comes in slower than expected.

Remember, it’s better to be pleasantly surprised by extra income than to be caught off guard by a shortage.

Ignoring Cash Reserves

Focusing only on what’s coming in and going out and forgetting to set aside a cash reserve is risky. Without a cash cushion, even small problems can throw the business off track. You might struggle to pay bills, miss out on new opportunities, or damage your reputation with suppliers.

To avoid this mistake, try these tips:

- Always keep a “safety net” of cash, enough to cover at least 1–3 months of expenses.

- Include this reserve in your forecast as a non-negotiable item.

- Don’t dip into your reserve unless it’s a real emergency, and if you do, rebuild it quickly.

Cash reserves are like a life jacket. Most of the time, you won’t need it, but when you do, it can save the business.

Not Accounting For Seasonality

For many industries, income and expenses change with the seasons. If you don’t plan for seasonal highs and lows, you might spend too much during busy times and struggle during slow months. This can lead to cash shortages, unpaid bills, or even needing emergency loans.

Here’s how to play safe:

- Save extra cash during busy months to help you through slower periods.

- Look at past years to spot patterns, like sales dropping in January or rising in December (a good look at your Excel sheets would help).

- Adjust your forecast to reflect those ups and downs.

Streamline Cash Flow Forecasting With Software

Nowadays, automation is your best friend. While it can't replace the human element necessary for financial planning processes, it can help streamline operations, so you can focus on better decision-making initiatives.

Most financial reporting software offers built-in cash flow forecasting features, allowing you to track income, expenses, and balances all in one place. This makes it highly beneficial for mid-sized businesses to larger enterprises, who often require additional support for manual tasks.

Here are a few of my favorites on the market:

But I know not everyone works for a larger corporation. That's why I've also gathered my top free forecasting software options available. They're perfect for small businesses working with tight budgets.

Stay in the Know

For more financial topics, expert tips, and latest updates, subscribe to our free newsletter.