Double Entry Accounting: What It Is, Benefits, And How To Use It

Double-entry accounting is a valuable tool for bookkeepers and accountants, providing a way to accurately manage business transactions using a system of debits and credits.

While most accounting software (whether for SMBs or enterprises) can help you handle these processes, it's still important to understand how double-entry accounting operations.

That's why I built this guide. Using my experience in digital software and fintech, I made sure this article covers everything you need—from the basics to real-world examples and useful software.

Whether you’re brushing up or learning from scratch, I'm confident you’ll walk away with the knowledge (and possibly the tools) required to handle financial records with confidence. Let's get into it.

What is double-entry accounting?

Double-entry accounting is the system in which business transactions are credited and debited between two accounts — an ‘action account and a ‘reaction’ account.

In any double-entry journal entry, one amount is debited and must be reflected by an equal (and opposite) credit amount in a different account.

- Debits increase the balance of asset and expense accounts, whilst decreasing the balance of liability, income, and equity accounts.

- Credits have the opposite effect on each of these accounts.

This is an effective way of maintaining checks and balances, clearly mapping how financial resources are being allocated throughout business operations.

You don't have to become a CPA to master accounting systems like this; accounting software makes the process simple.

Single-entry vs. Double-entry Accounting

Single-entry accounting is the most basic way to document business expenses. Under this accounting method, purchases and sources of income are consolidated into one simple list, much like a checkbook.

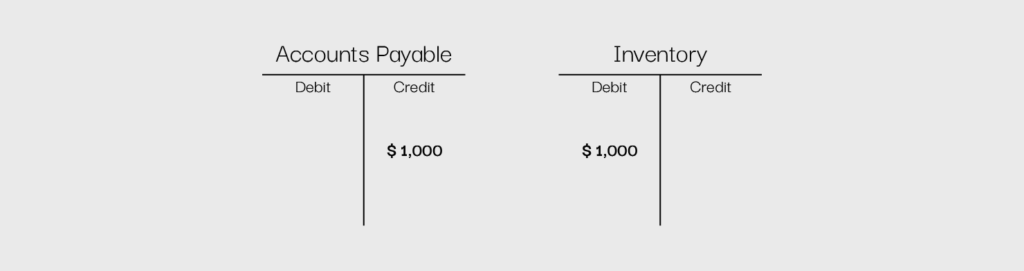

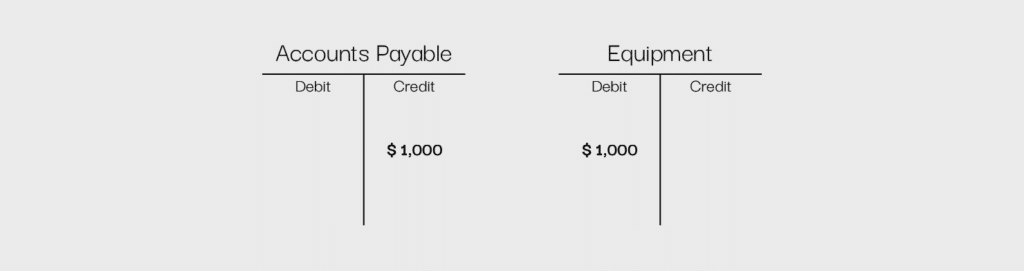

Double-entry accounting, on the other hand, acknowledges both sides of a transaction — the ins and outs, so to speak. For example, if you buy a new computer for your business, an account used to make business purchases, such as "accounts payable," would be debited, and an account related to assets, such as "equipment," would be credited. This shows that business resources were used to purchase an asset — in this case, a computer.

In a single-entry system, there would only be one line item: the cost of the computer.

T-Accounts (T-Charts)

A T-account, also known as a T-chart, is a simple way to visualize a double-entry bookkeeping system. A large T can be drawn on a sheet of paper, with one side labeled debit and the other labeled credit.

Debit entries are recorded on the left side of the T, and credits are recorded on the right side. This way, all accounting entries can be clearly marked and separated by type.

Using the computer purchase example above, a common setup for a T-account is as follows:

Using T-accounts separates each aspect of a transaction, creating a simple and, straightforward visual representation of the expenditure.

Account Types

There are five basic kinds of accounts that a double-entry accounting system can make use of. These accounts are assets, liabilities, income, expenses, and equity. Each has a slightly different role in the course of business. Using proper accounts can help bookkeepers organize basic accounting activities for a more comprehensive overview of transactions.

Assets

Asset accounts represent the items or intangibles owned by a company, which are expected to have future benefits for said company. This includes items such as cash, equipment, and inventory, as well as goodwill and intellectual property.

To reflect increases in asset accounts, you debit them. For example, if I receive more cash as a business, I will debit the cash account.

Liabilities

Liability accounts represent forms of debt a business holds, such as explicit debt via short- and long-term loans, or implied debt such as accounts payable or unearned revenue.

To reflect increases in liability accounts, you credit them. For example, if I take on a short-term loan, I will credit the short-term loan account.

Income

Income accounts contain all sources of income a business earns, such as interest income or product sales.

To reflect increases in income accounts, you credit them. For example, if I earn additional income through a new sale, I will credit the business revenue account.

Expenses

Expense accounts include all costs associated with running a business, such as utility bills, salaries, taxes, and rent.

To reflect increases in expense accounts, you debit them. For example, if I pay my employees, I will debit the payroll account.

Equity

Equity accounts represent total shareholders’ equity in a business and include accounts such as common stock and preferred stock, as well as retained income — the difference between money invested in the business and any profit left over after expenses are accounted for.

The equity accounts “retained income” or “deficit” on an income statement are a great way to see, at a glance, how much a company has earned or lost over time. If there is a retained income account, then this business has earned more money than it has spent over time; if there’s a deficit account, the opposite is true.

To reflect increases in equity accounts, you credit them. For example, if I sell new common stock, I will credit the common stock account.

Summary

- For an asset account, you debit to increase it and credit to decrease it

- For a liability account, you credit to increase it and debit to decrease it

- For an income account, you credit to increase it and debit to decrease it

- For an expense account, you debit to increase it and credit to decrease it

- For an equity account, you credit to increase it and debit to decrease it

-

Fulfil

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.1 -

BlackLine

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.5 -

Joiin

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.7

How double-entry accounting works

The following steps can help you successfully establish a double-entry accounting framework for your business.

Step 1: Set up a chart of accounts

First, you'll need to set up a chart of accounts. This means creating a master list of all the accounts that apply to doing business in your particular company, using all of the above types of accounts. For example, if you own business tools, such as computers or servers, you'll need an equipment account.

This process can be done manually by going step by step through all the elements that keep your business operational, or it can be easily completed through the use of software.

It may be necessary to create new accounts if the course of business changes or new income sources or expenses become relevant. This can be more complicated to handle without accounting software.

Step 2: Use debits and credits for all transactions

Once you have your chart of accounts, you can start recording debit and credit entries for your transactions.

Here's an example of how you can delineate which accounts are being debited and which accounts are being credited when you buy a new computer with cash:

Pay rent to a landlord:

Or pay tax on income from normal business operations:

Using this simple system, you can easily see where your money is flowing and where it’s ending up.

While you can manage this process through a hand-drawn T-chart or a software program, such as Microsoft Excel, most companies use accounting software, as it allows them to keep specific, accurate records. Accounting software can minimize the likelihood of errors, as these systems are designed to ensure entries are booked properly.

For example, many programs won't allow an entry to be posted if it isn't balanced. You can also create and update financial statements simply using any type of accounting software.

Step 3: Make sure every financial transaction has two components

In double entry accounting, the most important thing to remember is that every transaction has two sides, and to maintain a balanced business, both sides must be equal. If the idea of a double entry for every transaction is a little confusing, remember Newton's third law of motion: every action has an equal and opposite reaction. If you bring your leg back to kick a ball, the energy generated by that action will cause the ball to move.

The same is true in business; every expense you pay gains you something, and every kind of income you make takes away from somewhere else, such as inventory.

In a non-business sense, purchasing a new computer to manage accounting and payroll for your company may seem as easy as pulling out your credit card, completing a purchase, and walking out of an electronics store.

However, from a business sense, there's a little more nuance. To make your purchase, you're crediting a liability account — accounts payable, in this case. However, that money used isn't vanishing into thin air; it's being used to obtain an asset for your business, which means debiting an asset account.

Now that you've read through how double-entry accounting works and seen examples, it's time to test your knowledge!

3 Advantages of Double-Entry Accounting

Double-entry accounting is a reliable way to track finances with several benefits. Here are three key advantages that make double-entry accounting essential for any business:

1. Accuracy and error detection

Double-entry accounting keeps your records accurate by making sure every transaction is recorded in two places—once as a debit and once as a credit.

Say you buy a new laptop for $5,000. You record a debit in your “Equipment” account and a credit in “Cash” or “Accounts Payable.” If you accidentally forget to record one side, your numbers won’t add up, and you’ll know something’s off.

Without double-entry accounting, small errors could go unnoticed and cause bigger issues down the road. Keeping everything balanced helps you stay on top of your finances, avoid costly miscalculations, and keep your records in check.

2. Financial transparency

With double-entry accounting, you always have a clear picture of where your money is going and coming from. Since every transaction is recorded in two accounts, you can easily track assets, debts, revenue, and expenses.

For example, if your business takes out a loan, you’ll record an increase in cash but also a liability to show what you owe. This way, your financial reports always tell the full story—no surprises, no missing information.

Having a transparent system like this helps with budgeting, tracking growth, and planning ahead. Instead of guessing where your money is going, you’ll have solid data to back up your decisions and keep your business financially healthy.

3. Better fraud prevention

Double-entry accounting doesn’t just keep your records accurate—it also helps protect your business from fraud. Since every transaction affects two accounts, sneaky changes or missing money become much easier to spot. It’s like having an automatic security system for your finances.

Imagine an employee tries to pocket company money by altering an expense record. With double-entry accounting, the numbers won’t add up, and the mismatch will raise a red flag. Auditors or finance teams can quickly step in, review the records, and catch any suspicious activity before it gets out of hand.

Not only does this system help uncover fraud, but it also discourages people from trying anything shady in the first place. When every transaction leaves a paper trail, businesses can feel more secure knowing their financial data is protected.

3 Disadvantages of Double-Entry Accounting

Now that you know about the advantages, here are some the common disadvantages associated with double-entry accounting:

1. Complexity

Unlike single-entry accounting, where transactions are recorded once, double-entry involves debits and credits, different account categories, and balancing the books. For entry-level financial professionals or small business owners, this accounting learning curve can be steep, leading to mistakes if not properly understood.

2. Time consuming

Recording every financial transaction twice takes significantly more time than a single-entry system. Every purchase, sale, and expense must be categorized correctly, with matching debits and credits. This can slow down bookkeeping, especially for businesses with a high volume of transactions.

To help streamline these processes, consider investing in a business accounting software. While it can't take away all of the manual tasks, it can make life a little easier. Here's some of my top picks to convince you of their value:

3. Can be overkill for smaller businesses

For very small businesses, freelancers, or individuals managing personal finances, double-entry accounting can feel like overkill. If a business has only a few transactions per month, the time and effort required to maintain a double-entry system may not be justified. A simpler single-entry system might be more practical for basic income and expense tracking.

Deciding if double-entry accounting is right for your business

Double-entry bookkeeping may sound, at times, needlessly complex, but it's a valuable tool used by companies around the world. Rather than simply listing expenses and income, businesses can break things down on a detailed level, helping decision-makers better understand how money is being used.

Ready to compound your abilities as a finance leader? Subscribe to our newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry.

{kind=link}