The Ultimate Guide to Expense Accounts: Everything You Need to Know for Smarter Financial Management

Expense Tracking Simplified: Expense accounts track costs incurred by a business, reducing profit and aiding in financial reporting, part of the income statement. They provide visibility and control into a company's finances.

Know Your Expense Account Types: There are multiple types of expense accounts, like COGS, operating expenses, non-operating expenses, and non-deductible expenses.

Managing Expense Accounts: To keep expense account management simple, standardize your expense categories, automate expense tracking with software, and plan for tax deductions and compliance in advance.

Expense accounts are an accounting staple. They help track money spent for business and prepare GAAP-compliant financial reports at the end of the accounting period.

It’s a simple concept that comes with a few nuances. In this guide, I use my experience as a former accountant to help simplify the meaning and role of expense accounts, as well as address a few of their variations. Let’s dive in.

What Are Expense Accounts?

Expense accounts are temporary accounts that track the costs incurred by a business in the process of earning revenue. They are part of the income statement (or profit and loss statement) and are used to record all the spending that reduces profit.

Common expenses include rent, salaries/wages, utilities, advertising, office supplies, and travel. When a business pays for something (like travel), that amount is debited to an expense account. This increases the total expenses, which then lowers the company's profit.

Here’s what the process typically looks like:

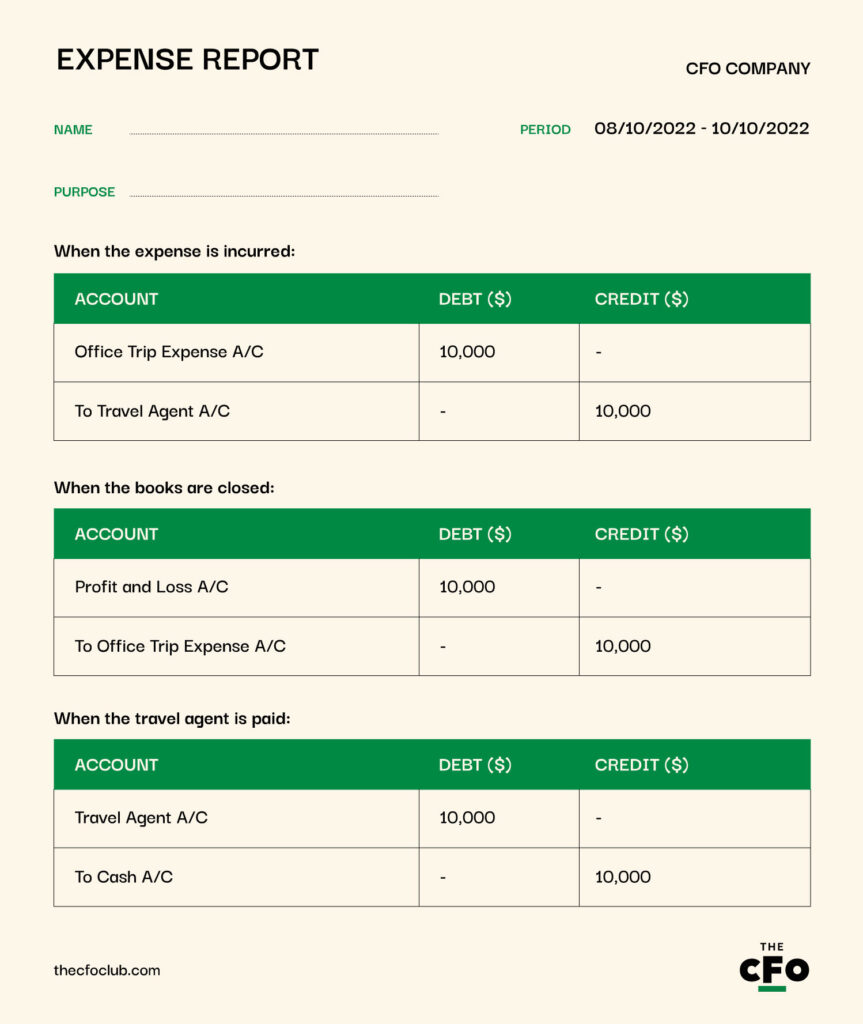

Let’s say you spent $10,000 on the annual office trip this year, including entertainment expenses. You haven’t paid the travel agent yet, and they don’t mind if you pay during the next accounting period.

The $10,000 is transferred to an “office trip expense” account, and the travel agent’s account is credited for the same amount. If you have questions about why it works this way, check out our guide on the three golden rules of accounting.

When you close your accounting books at the end of the accounting period, the balance in the expense account is closed to the profit and loss account (presented as the income statement for GAAP compliance). In your journal, the following entries are passed to record the transaction we just discussed:

Why Are Expense Accounts Important?

Expense accounts help organize and categorize expense transactions and their indirect costs. They also help monitor category-specific spending thresholds, giving you visibility, control, and insight into your business operations.

Example: Suppose you’ve budgeted to spend $50,000 on celebrations like birthdays, anniversaries, and other personal events of employees. Many of your team members had children this quarter, and you’ve already crossed the $50,000 limit before the end of Q2.

If you have an employee celebration expense account, your team will be able to flag a potential cost overrun for the current year. This gives you time to prepare and reallocate funds from another expense category or chart of accounts to employee celebration expenses to ensure you still stick to your overall expense limits.

The 4 Different Types of Expense Accounts

Did you know there’s more than one type of expense account? Different expense accounts have their own nuances, which are valuable to know in the long run. Here’s a complete breakdown of each type and what they entail:

Costs of Goods Sold

The cost of goods sold (COGS) includes the direct costs incurred to produce the goods for manufacturers. For retailers, COGS includes the cost of inventory and related expenses such as freight.

Even service companies have a COGS equivalent called the cost of sales (COS), which includes the direct costs (direct labor and overheads) of rendering the service. SaaS CFOs typically deal with cost of sales, but tech CFOs working with hardware companies still have COGS and inventory to take care of.

COS is expensed in the same year as it is incurred. They’re capitalized in some instances, but even then, they generally appear on the balance sheet as prepaid expenses. For example, if a portion of COS is prepaid for future services, it’s recorded as a prepaid expense and amortized over time.

Whenever a manufacturer spends on raw materials, labor, and overheads, the expenses are capitalized as inventory. These expenses remain on the balance sheet as inventory until they’re sold. When the retailer buys this inventory, their purchase cost appears on their balance sheet as inventory until sold further.

Say you sell t-shirts, and the per-unit cost of a t-shirt is $10. Whenever you sell one unit (one t-shirt), $10 is transferred from inventory to the COGS A/C. The cost of unsold inventory—let’s say 1,000 units worth $10,000—continues to appear on the balance sheet.

The balance in the COGS account is closed to the profit and loss A/C at the end of the year to calculate the gross profit.

Operating Expenses

Operating expenses are rarely capitalized. Most operating expense accounts, such as advertising expenses, business travel expenses, and utility expenses, are closed to the income statement at year-end.

However, there are a few exceptions. Examples include:

| Type | What It Is |

| Improvement Expenses | When you spend on repairs or overhauls that improve the functionality or efficiency of an asset or extend its lifespan, you can capitalize by adding the expenses to the asset's book value. |

| R&D Costs | Initial R&D costs are typically expensed, but specific costs post feasibility, such as coding and testing for internal-use software, may be capitalized and amortized if the conditions in ASC 350-40 and IRS §174 are fulfilled. |

| Prepaid Expenses | Expenses paid for services to be availed during a future accounting period are capitalized. Don’t forget to factor in the amortization expense when budgeting for future periods. |

| Interest on Construction Loans | Interest expenses paid during the construction of a long-term asset, such as a building, can be capitalized using an asset account until it’s ready for use and expensed through the depreciation account in future periods. |

Non-Operating Expenses

Non-operating expenses are ones that aren’t directly related to the company’s core business operations. They’re treated like any other expense. Here are examples:

- Interest: Interest is a financial expense. Interest on loans, bonds, or credit lines is categorized as a non-operating expense.

- Lawsuit Settlements and Legal Fees: Fines, penalties, and settlements from lawsuits that don’t arise from normal business activities are categorized as non-operating.

- Depreciation (sometimes Non-Operating): Depreciation expense on assets not used in core business (such as rental properties) may be classified as non-operating.

Non-Deductible Expenses

Non-deductible expenses are recorded just like any other expense, but they’re not adjusted for tax reporting purposes. While a non-deductible income still reduces your net profit, it doesn’t reduce your tax liability because the IRS disallows it.

Examples of non-deductible expenses include fines and penalties (such as IRS penalties and OSHA fines), political contributions and lobbying expenses, certain life insurance premiums (if the business is the beneficiary)

-

FreshBooks

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.5 -

BlackLine

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.5 -

Xledger

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.5

Benefits Of Expense Accounts

Expense accounts are a non-negotiable part of financial accounting because you can’t prepare financial reports without them. However, they also offer various other benefits, such as:

- Accurate Financial Tracking: Separating expenses into dedicated accounts prevents financial chaos. It ensures clean records for reporting, budgeting, and analysis.

- Tax Optimization and Compliance: Properly categorized expenses help maximize deductions while keeping the IRS happy—nobody likes an audit.

- Easier Audits and Financial Reviews: Whether internal or external, well-organized expense accounts speed up audits and reduce headaches when reconciling financials.

- Cost Control and Budgeting: Tracking different expense categories makes it easier to set budgets and identify areas of overspending before they become a problem.

Disadvantages Of Expense Accounts

There’s no good reason, or even an option, to ignore expense accounts. However, they still do have a few disadvantages, including:

- Complexity and Administrative Burden: Managing multiple expense categories can become overwhelming, especially for businesses with high transaction volumes. Too much granularity often translates to an administrative nightmare.

- Risk of Misclassification: Employees or accountants may misclassify expenses, leading to inaccurate financial statements and potential tax compliance issues.

- Inconsistent Categorization Across Departments: If different teams use different expense tracking methods, it can lead to reporting inconsistencies and reconciliation headaches.

How to Manage Expense Accounts

Managing expense accounts is more than just about bookkeeping. It’s about financial control, tax optimization, and strategic decision-making. Here are a few ways to effectively manage expense accounts:

1. Standardize Expense Categories

Categorize expenses and define what each category covers. However, avoid excessive granularity. Too many categories make reporting unnecessarily complex.

2. Automate Expense Tracking

Use cloud-based accounting software like QuickBooks, Xero, or NetSuite to categorize and track expenses automatically. Also, consider investing in expense management tools like Expensify, Brex, or Ramp to allow employees to submit receipts digitally.

3. Set Clear Policies and Expense Reporting

Define allowable expenses, clarify what employees can and can’t expense, and use a standard expense report template. Require receipts for expenses above a certain amount and establish expense approval workflows. For example, you could require manager approval for expense report reimbursements over $500.

4. Reconcile Accounts Regularly

Monthly reconciliations to ensure recorded expenses match bank statements and credit card transactions are an excellent strategy to avoid last-minute fuss over missing or questionable transactions.

5. Monitor Spending and Set Budgets

Analyze expense trends to see where a large chunk of money is spent. If costs are silently creeping up, regular reviews help catch them early. You can also control costs by establishing spending limits for each department and with performance review tools like budget variance analysis.

6. Plan For Tax Deductions and Compliance

To maximize tax benefits, keep detailed records of deductible expenses, such as subscription fees for business software and business trip expenses. Work with an accountant to stay compliant with IRS regulations.

7. Review and Optimize Accounts Periodically

Consolidate redundant expense categories to simplify financial reporting. Identify underutilized subscriptions or services that can be canceled and review historical spending trends to make data-driven budgeting decisions.

Expense Account Management Tools

Expense management can become too complex to handle manually as business grows. That’s where expense management software helps. With the help of expense management tools, you can automate most processes, streamline reporting, and make data-driven decisions.

If you’re looking for an expense management solution, here are some of our top picks:

Software and Simplicity Are Mission-Critical

Expense accounts can turn into a complex web of transactions. The best way to manage them? Simple categorization and expense management software that make things easier by eliminating chaos, errors, and manual effort out of the expense management process.

Ready to compound your abilities as a finance professional? Subscribe to our free newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry.

{kind=link}