How to Master the Financial Close Process: A Step-by-Step Guide

Picture this.

It’s 11:57 p.m. on the last day of the month. The finance team at a mid-sized tech firm is still hunched over spreadsheets.

They’re chasing down a missing invoice that has thrown the entire close off balance.

The deadline’s about to slip, the team’s temper is flaring, and the CFO is refreshing her inbox every 30 seconds.

If that sounds familiar, you’ve seen how financial close can sometimes feel like a crisis. In this guide, I use my knowledge as a former accountant to help you understand the basics of financial close. I’ll walk you through a structured financial close process so you can get it right and keep improving month after month.

What Is the Financial Close Process?

The financial close process is the sequence of steps a company takes at the end of a reporting period to ensure its books are complete and accurate.

It involves recording and reconciling transactions, making adjustment entries (such as accruals and depreciation), and preparing financial statements.

Once everything is reviewed and approved, the period is officially closed.

Why Is the Financial Close Process Important?

The financial close process is mission-critical to ensure accuracy of financial data, meet regulatory and audit requirements, and produce clean and accurate financial reports for internal use and external filings.

Here’s an overview of the finance professionals involved in the close process:

- Accounting Team: In charge of journal entries, reconciliations, and financial statement prep.

- FP&A Team: Reviews variances, forecasts, and budgeting alignment.

- Controllers: Oversee the process and ensure internal controls are followed.

- CFO: Reviews and signs off on final financials for internal and external reporting.

The Financial Close Process: What You Need to Reconcile

Reconciliation is a critical part of the financial close process. To reconcile, you need the right documentation in place. Start by getting your hands on the following documents:

- Bank and credit card statements

- General ledger reports

- Invoices and receipts (both AP and AR)

- Payroll reports

- Inventory counts and valuation reports

- Loan and lease statements

Here are examples of accounts you need to reconcile once you have the documentation ready:

- Bank accounts

- Accounts receivable and accounts payable

- Intercompany transactions

- Inventory

- Fixed assets

- Accrued expenses and prepaid accounts

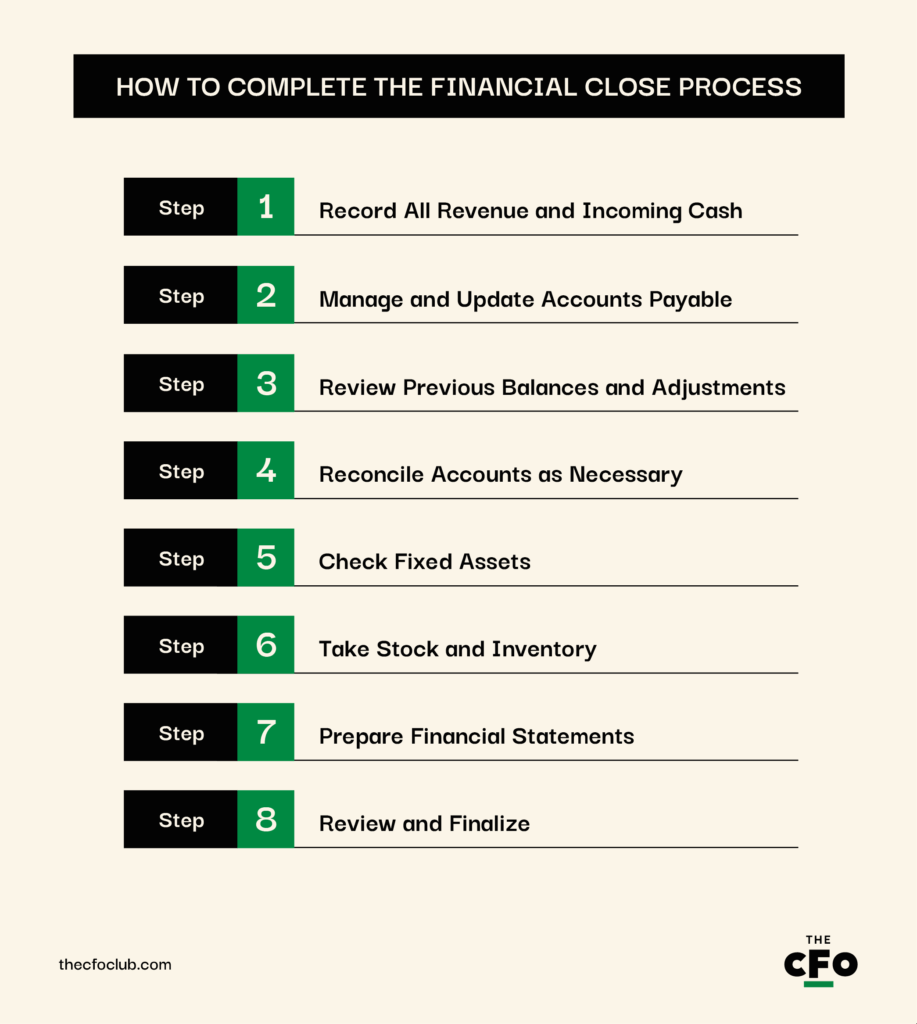

How To Complete The Financial Close Process

The financial close process differs among companies based on their business type, accounting methods, and policies.

Below, I’ll walk you through a general financial close process. Think of it as a starting point for your financial close process and make tweaks to tailor it to your company’s needs.

1. Record All Revenue and Incoming Cash

Look back through the entire accounting period. For example, if you’re preparing quarterly financial statements, go back to day one of the current quarter and verify the amount earned or received, even if it’s not yet billed or deposited.

Then use guidelines in ASC 606 or IFRS 16, as applicable, to recognize revenue. Examples of revenue and incoming cash to capture include:

- Product or service sales (invoiced and unbilled)

- Deferred revenue recognized in the current period

- Subscription renewals and usage-based fees

- Customer deposits and prepayments

- Loan proceeds or financing inflows

- Interest income or investment returns

- Refunds or rebates from vendors

2. Manage and Update Accounts Payable

If you document every purchase, service, or recurring expense as it becomes due, you can skip this step. But if you don’t, you need to have invoices and receipts:

- Enter all bills and invoices into your accounting system.

- Accrue the expense to reflect the liability towards goods or services you’ve received but haven’t been invoiced for.

- Review which invoices were paid and which remain open so you don’t overstate or understate accounts payable.

3. Review Previous Balances and Adjustments

Next, it’s time to carryover balances and prior-period adjustments. This includes prepaid expenses, accrued liabilities, deferred revenue, and amortizations—items that are recorded in one period but recognized in a different period.

For example, if your company prepaid for electricity last quarter, you need to set it off against the current quarter’s electricity bill and convert that asset (prepaid electricity bill) into an expense (electricity expense).

4. Reconcile Accounts as Necessary

Reconciliation involves matching internal records with external or independent sources to confirm accuracy. When reconciling, you need to look for mismatches, timing differences, or errors and resolve them before the close is finalized.

Common accounts reconciled during this stage include:

- Bank Accounts: Match GL cash balances to bank statements.

- Accounts Receivable: Reconcile customer invoices and payments against the AR subledger.

- Accounts Payable: Confirm vendor account balances and payment schedules.

- Credit Card Statements: Match company credit card charges to expense reports and the GL.

- Prepaid and Accrued Expenses: Verify balances against schedules and invoices.

- Fixed Assets: Verify the accuracy of additions, disposals, and depreciation entries.

- Intercompany Accounts: Ensure transactions between related entries are mirrored on both sides.

Pay attention to debits and credits. All transactions should have a corresponding and equal entry on both sides of the ledger. If something’s off—say, an expense is posted without a credit to cash or AP—it creates an imbalance that cascades into even bigger miscalculations.

If your company has multiple entities or subsidiaries, you’ll need to reconcile intercompany transactions as well. For example, if Entity A records a sale of goods to Entity B, Entity B must record a purchase of equal value.

5. Check Fixed Assets

Fixed assets aren’t purchased and sold frequently, but they impact your income statement and balance sheet every period. Most companies typically own at least a few fixed assets, such as:

- Machinery and equipment

- Office furniture

- Company vehicles

- Buildings and leasehold improvements

- Computers, servers, and IT hardware

- Capitalized software or development costs

Here’s what you should review during the financial close process for the period you’re accounting for:

- Ensure that assets purchased are recorded at a GAAP-compliant value.

- Review disposal or retirement of assets to check if associated gains and losses are booked.

- Verify if depreciation was claimed according to the depreciation schedule.

- Check if capital expenses have been misclassified as regular expenses and vice versa.

6. Take Stock and Inventory

Inventory discrepancies are common, especially for businesses with large or fast-moving stock. That’s why a monthly count—whether a full physical inventory or a cycle count—can help ensure accuracy of inventory records in your books.

An inventory audit also reveals other issues like theft, shrinkage, miscounts, and obsolete goods before you’re forced to write a significant amount off your books.

Example:

Suppose Alina Inc., a retail fashion brand, wants to review inventory. Their accountant recommends a cycle count for high-turnover items like seasonal apparel, accessories, and bestsellers. The reason? These items are most likely to be misplaced, stolen, or misrecorded due to high sales velocity and frequent movement.

On the other hand, it’s fine to audit slow-moving inventory like last season’s shoes or returned merchandise quarterly. They still require periodic reconciliation, just not as frequently.

Now, why did Alina Inc.’s accountant recommend an inventory audit and why did they recommend two different approaches based on inventory type?

Because by skipping the inventory audit, Alina Inc. risks inflating reported assets, overstating profitability, and failing to detect product losses. Auditing inventory and using different approaches allows Alina Inc. to minimize these risks as well as the costs of the audit.

7. Prepare Financial Statements

Once all transactions are recorded and account reconciliations are complete, it’s time to bring the entire close together through financial statements.

This is where all your efforts from the previous steps culminate into a clear picture of your company’s financial health.

I believe most companies use financial accounting software at this point. I’ve been using one for all my businesses since I started my first business back in the 2010s. If you don’t currently use one, it’s about time. These are only some of my favorite financial management tools:

Clicks on the links below may earn a commission, which supports our independent testing and review of software and services. Learn more about how we stay transparent.

{kind=link}

The software will automatically create an income statement, balance sheet, cash flow statement, and statement of retained earnings. It also helps consolidate data from across subsidiaries, minimizes the probability of errors, and updates financial statements in real-time.

8. Review and Finalize

Reviews are critical to ensure accuracy, compliance, and accountability before you officially report any numbers.

Let the accounting team lead the initial review. During this review, the accounting team checks for outliers, verifies supporting documents, and ensures all journal entries and reconciliations are complete.

Then, request the controllers, finance directors, and the CFO to validate the financial statements, ask probing questions, and confirm that everything aligns with company policies and GAAP/IFRS.

Once reports are finalized, your financials become the official record of business performance for that period. The income statement is reset. The balance sheet is locked in. And your accounts are ready to record new transactions for the next close.

Financial Close Process Checklist

Here’s a checklist that includes key actions, required documents, and responsible parties for each step of the financial close accounting process:

When the Closing Process Is Necessary

Most companies close their books monthly, quarterly, or annually. All three closes vary in level of depth and scrutiny:

- Monthly: A month-end close helps you to stay on top of cash flow, monitor performance, and catch errors early. Monthly closes are typically not too intense but thorough enough to support tactical decision-making.

- Quarterly: Quarterly closes are more detailed. These are more aligned with internal reporting cycles and investor expectations than monthly closes.

- Annual: Year-end is the most rigorous, often tied to audits, tax filings, and external reporting. These require full documentation, reconciliations, and sign-offs across departments for all financial activities and transactions.

The time required for a financial close varies based on depth and scrutiny, so annual closes take the longest, and monthly closes are the quickest. Of course, the specific number of days you need for each close varies based on your company’s size, systems, and complexity.

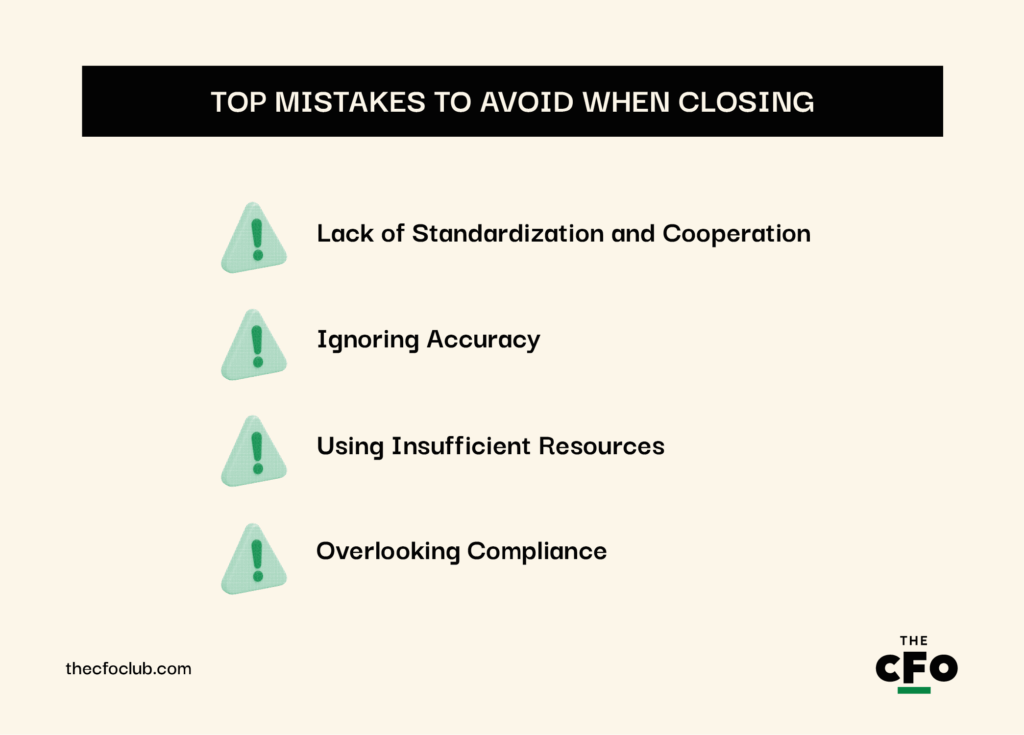

Top Mistakes to Avoid When Closing

Making mistakes delays the financial close process and, from what I’ve seen, frustrates the accounting team. Here are some top mistakes you should be mindful of during the financial close process:

Lack of Standardization and Cooperation

Financial close can quickly turn into a chaotic process when responsibilities are unclear and there’s a general lack of communication and cooperation between teams.

Departments often pull on different ends of the same string—they use conflicting templates, don’t use a shared checklist or calendar, and wait on each other with no clear owner for each task in the process.

To steer clear of this mistake:

- Standardize the close process with documented SOPs

- Use shared checklists and a centralized close calendar

- Hold regular meetings with finance, ops, and leadership to keep everyone in sync

Ignoring Accuracy

Speed is great. It helps you make a good impression and lets you move on to other more interesting tasks.

The problem? Rushing through entries and reconciliations can snowball into major reporting errors and regulatory issues. Inaccurate data doesn’t just make you look bad. It puts your company’s reputation in jeopardy and undermines trust in your numbers.

To ensure accuracy:

- Prioritize accuracy over speed

- Implement review checkpoints throughout the process

- Use automation tools to reduce manual entry errors

- Train your team to flag and escalate inconsistencies early

Using Insufficient Resources

A lean team and outdated, legacy software bottleneck your financial close process. It’s easy to see how too few hands, too much manual work, and not enough automation can lead to delays and burnout.

You can’t expect a quick and efficient financial close with low-performing resources. Equip your team with the following to avoid this issue:

- Ensure your accounting team is well-staffed and well-trained

- Offload repetitive work so your team can focus on review and analysis during end closing

- Invest in financial reporting automation software to streamline close tasks and other manual tasks

Overlooking Compliance

Most people think of compliance from a legal perspective, but failure to comply also damages your credibility, and that’s why you should never overlook compliance.

Missing tax deadlines, misreporting financials, or failing to meet regulatory requirements leads to penalties, audits, and loss of reputation.

To make sure you’re always compliant:

- Stay updated on relevant regulations (GAAP, IFRS, SOX, etc.)

- Build compliance checkpoints in your close process

- Use software with audit trails and built-in controls

- Involve legal or audit teams where necessary

Additional Financial Closing Best Practices

Here are some additional best practices that will fast-track your financial close process:

- Focus on Efficiency: The money you spend on the financial close is directly proportional to the time you spend on it. The longer the process drags, the more money it will cost you. To make sure you’re able to close quickly at the end of the month, eliminate redundancies in the process, automate low-value tasks, and reduce dependencies between departments.

- Streamline Data Access: Delays are inevitable when your teams are digging through emails, spreadsheets, business units, and legacy systems for data. Use integrated tools or ERP systems to centralize data so every stakeholder has secure, real-time data access. This accelerates the process and minimizes data integrity risks.

- Create Standard Procedures: A documented close process is non-negotiable. Define clear workflows, assign owners to each step, and establish timelines based on your reporting deadlines. Standardized procedures ensure consistency across periods, improve accountability, and make it easier to train newcomers when team members change.

Getting Better Every Close

The financial close is a messy process unless you proactively streamline it. Each month is an opportunity to improve. Find what slowed you down last month, errors you made, and tools or processes that can eliminate friction from your process. And remember—whether you’re trying to shorten the close cycle, eliminate time-consuming manual processes, or strengthen internal controls—progress compounds.

Looking for more guides to grow your career in finance? Subscribe to our free newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry.