A Step-By-Step Guide For Mastering Consolidated Financial Statements

Consolidating Made Easy: To properly consolidate your finances, you'll need to have important information, such as non-controlling interest, financial highlights, consolidated income statements and balance sheets, and changes in equity.

Steps to Consolidation: Creating a consolidated financial statement involves knowing your scope, removing intra-group connections, determining gains and losses, and combining finances.

Don't Forget!: Don't forget to double check your work. Miscounting intra-group transactions and having unaligned reporting periods can lead to inaccurate reporting and compliance issues.

Consolidated financial statements show the combined financial picture of a parent company and its subsidiaries—basically treating them as one big company on paper. It’s one thing to understand what they are, but putting them together is a whole different ballgame.

As a seasoned financial controller, I’ve worked through my fair share of tricky consolidations for multi company organizations. In this guide, I’ll break down what consolidated financial statements are, how to create them, and their added benefits. Ready to get into it?

What are Consolidated Financial Statements?

Consolidated financial statements are combined reports that present the financial position and performance of a parent company and its subsidiaries as a single entity.

Typically put together by the parent company, consolidated financial statements include a group-wide balance sheet, income statement, and cash flow statement—the three key elements of the 3-statement model.

These components also make up the three types of consolidated financial statements:

- Consolidated balance sheet

- Consolidated income statement

- Consolidated cash flow statement

For example: If a parent company loans $500,000 to a subsidiary, each would report the loan as an asset or liability, inflating the group’s financials. Consolidation cancels this out, giving a clearer picture of net worth.

Consolidated Financial Statement Requirements

To conduct consolidated financial reporting, you need to meet certain criteria as stipulated by accounting standards like the International Financial Reporting Standards (IFRS) and the Generally Accepted Accounting Principles (GAAP).

In addition, you'll need to make sure you meet all the following requirements or have the necessary information as outlined below:

Prepping for Subsidiaries vs. Parent Companies

Preparing consolidated statements is a partnership between the parent company and all its subsidiaries. The subsidiaries provide accurate and uniform fiscal figures while the parent company draws up the consolidated financial statements. Specifically:

- Subsidiaries provide individual balance sheets, income statements, and cash flow statements based on the parent company’s reporting system.

- Parent companies combine their own records (if any) and the different subsidiaries' reports according to IFRS and GAAP regulations.

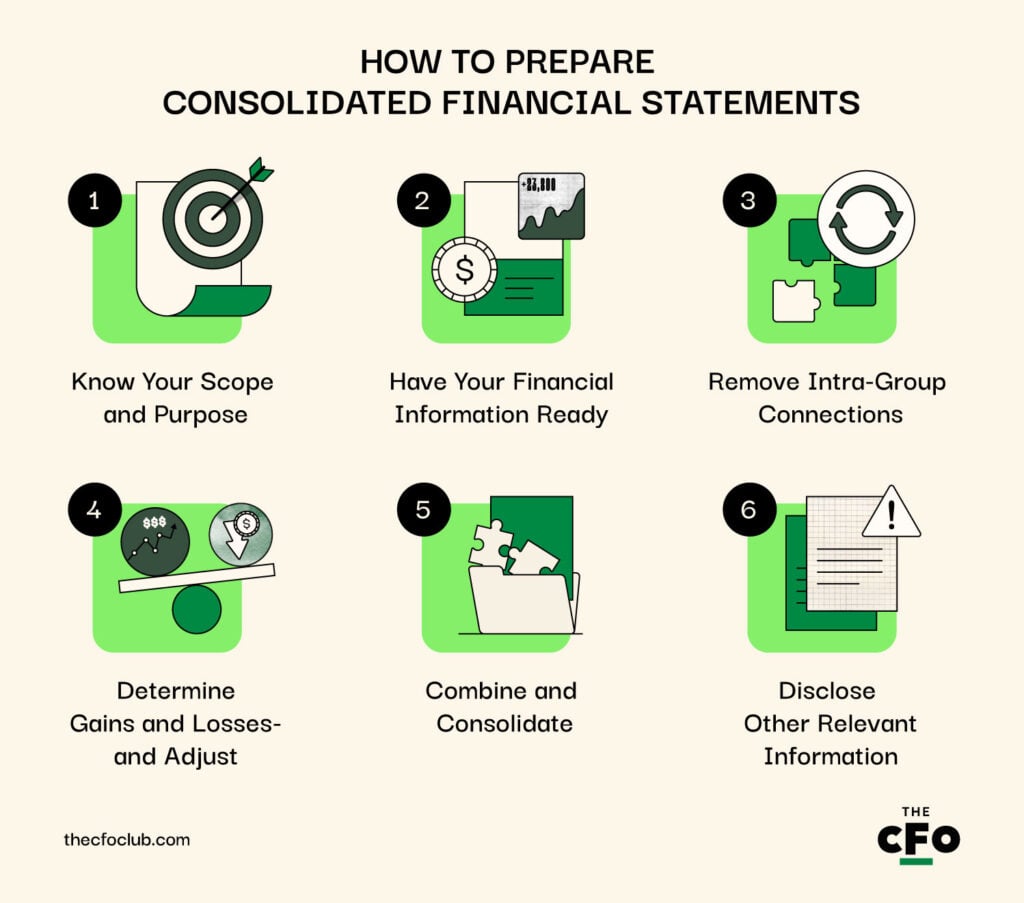

How To Prepare Consolidated Financial Statements

Preparing consolidated financial statements is complicated but possible. Simply follow the steps below to the T to create an accurate and reliable report for stakeholders.

1. Know Your Scope and Purpose

Establishing the scope and purpose of your consolidated financial statements helps you stay compliant and avoid misunderstandings during the compilation process.

So before anything else, map out your reporting entities, i.e., companies to be included in the consolidated financial statement:

- The Parent Company: The main organization that prepares the statement.

- Subsidiaries: Any company the parent controls either by possessing over 50% of voting shares or wielding decision-making powers

- Variable Interest Entities (VIEs): Companies where the parent has significant control or influence which isn’t based on equity ownership but conditions like agency relationships or contractual arrangements. If the parent has the power to direct a VIE’s activities, the company must be included in the statement. But if the parent does not control the entity (e.g., minority interests or joint ventures), it may account for that entity using the equity method, instead of consolidating it. If your company has no VIEs, then you don’t need to worry about this part at all.

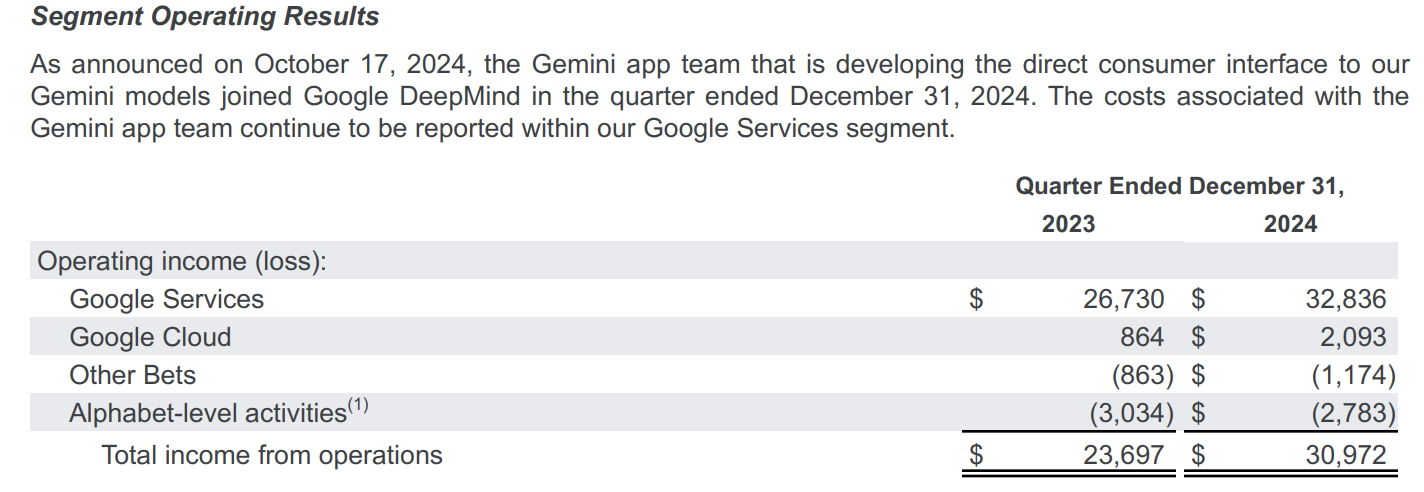

Consider Alphabet, the parent company of Google. To keep investors and other stakeholders informed, it consolidates its revenue and that of all major subsidiaries into a single record quarterly. Below is a screenshot of Alphabet’s segment operating results as displayed in its consolidated statements for Q4 2024:

Note how the subsidiaries are broken into four categories: the three major divisions that drive the most income (Google Services, Google Cloud, and Other Bets) and the parent company itself.

This means that though Alphabet owns many subsidiaries, only the first two—Google Services and Google Cloud—are significant enough to report on individually. The rest are included in the consolidated statement but lumped together into one broad category—Other Bets—due to their minimal bottom-line impact.

2. Have Your Financial Information Ready

Primed financial information makes consolidation straightforward. Prep your finances for the process by doing the following:

- Collect each entity’s recent records, from balance sheets to income statements, cash flow statements, intercompany transactions, and equity ownership percentages.

- Amend any differences in account practices, currencies, or fiscal year ends to standardize the financial information of all entities and avoid discrepancies.

- Use financial consolidation software to simplify the data collection and calculation process, and also reduce human error.

- Sync your accounting software, like QuickBooks or Xero, to your consolidation tool to quickly and accurately extract the financial data of multiple entities for the final report. The software will also help automate your bank statement reconciliation process.

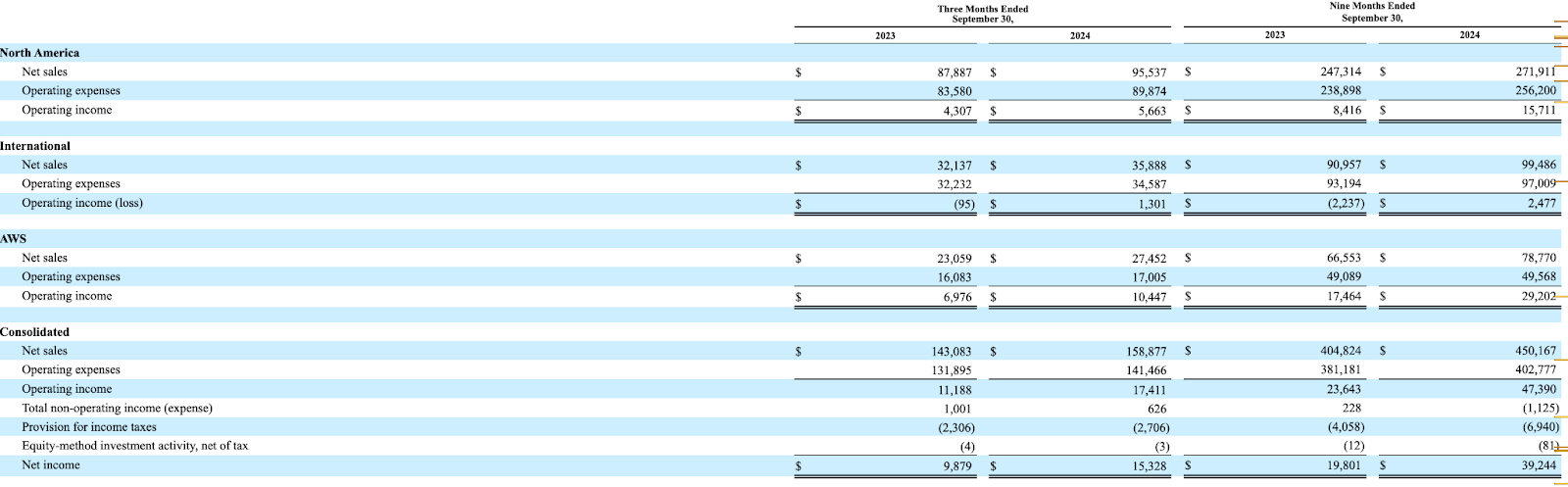

Take Amazon for example. As an online retailer, cloud service provider, and multinational corporation, its total revenue draws from multiple sources, regions, and currencies.

So, in consolidating its finances, the firm segments its operations into three major categories—North America, International, and AWS—and pulls financial data from each one. It also converts all its foreign currency income to USD and ensures reporting period uniformity.

But unlike Alphabet, Amazon’s consolidated statement (at least as of Q3 2024 as shown above) does not include specific parent-level numbers, though I suspect they were merged into the North American figures.

4. Remove Intra-Group Connections

Removing intra-group transactions—like asset or service exchanges between subsidiaries— from your consolidated statement prevents double counting and misstatements.

Say you handle accounting for a multinational with two main subsidiaries: A and B. During the reporting period, subsidiary A sells inventory to subsidiary B. The revenue from those sales simultaneously becomes income for subsidiary A but a cost for subsidiary B.

For accuracy, exclude all records of this transaction from the consolidated dataset. Why exactly? Because the money merely moves between subsidiaries and has zero impact on the group’s bottom line.

Situations like this are why many companies rely on financial consolidation software which automatically filters and deletes intra-group transactions. Alternatively, manual consolidation can lead to intra-group transaction oversights and inflated numbers, falsely indicating financial stability to stakeholders.

5. Determine Gains and Losses—And Adjust

After excluding intra-group transactions, remove gains and losses too as these can also skew profit numbers. They also impact tax payments and investment decisions so your consolidated finances must provide true and fair reflections of profit.

Here, gains and losses mostly apply in these two scenarios:

- Foreign Exchange Rates: Say your parent company in the United States makes purchases from an overseas supplier. Exchange rate fluctuations may lead to unrealized gains or losses, so you need to adjust the consolidated statements to accurately reflect currency conversion effects.

- Value of Intangible Assets: Suppose your company holds a patent that appreciates or depreciates over time. You may need to modify your records to show its current fair value in the consolidated statement.

6. Combine and Consolidate

Once you’ve removed all intra-group dealings and accounted for gains and losses, it’s time to combine and consolidate.

This stage involves unifying financial statements across divisions by compiling intercompany income statements, balance sheets, and cash flow statements into one coherent report. It also involves providing other quantitative summaries—like financial highlights and segment information—as well as qualitative context to make the presented figures easy to grasp.

For example, Unilever has many subsidiaries across the globe. But for investor relation purposes, it creates one combined financial statement periodically instead of publishing stand-alone reports for individual entities.

This consolidation saves investors time and energy as it gives them granular insight into the firm’s financial performance without requiring separate readings of each subsidiary’s report.

7. Disclose Other Relevant Information

When preparing consolidated financial statements, you need to disclose additional information that would otherwise affect the company’s consolidated position. This disclosure gives an additional view on several issues that are too complex to address in the primary document, like:

- Accounting policies adopted during the consolidation process.

- Liabilities that are likely but do not appear in the balance sheet.

- Non-controlling interest breakdowns, revealing the percentage ownership of the minority stakeholders.

- Invoice factoring transactions and rates.

Not only does this information boost investor trust and empower stakeholders to make data-driven decisions, but it also keeps your company compliant with regulatory standards.

For example, here is a “disclosures” excerpt screenshot from Berkshire Hathaway’s 2024 annual report.

It introduces several market risks the company is susceptible to due to some of its strategic decisions, from equity price risks to interest rate risks, foreign currency risks, and commodity price risks. This information is of utmost importance to investors and regulators alike as it reflects the firm’s overall financial strategy and risk exposure, increasing financial transparency.

When To Consolidate Financial Statements

Companies typically consolidate financial statements quarterly, annually, or at the close of each fiscal period (whenever that is for them).

However, when a new subsidiary is acquired, consolidation for its finances starts on the date control is gained, and the acquisition is reflected in subsequent financial statements to indicate ownership changes.

Consolidated Financial Statements vs. Unconsolidated Financial Statements

Consolidated financial statements combine the finances of a parent company and its subsidiaries, eliminating intra-group transactions, to present the group as a single entity.

Meanwhile, unconsolidated (or individual) financial statements show the financials of a single economic entity, excluding its subsidiaries, or parent company as the case may be, from the consolidation process.

While it is more beneficial to consolidate financial statements, there are some cases where it is acceptable to not do so. Specifically, unconsolidated financial statements are acceptable in the following cases:

- Lack of Control Over Subsidiaries: If a parent company has less than 50% voting shares in a subsidiary or lacks decision-making powers over it, consolidation is not required.

- Minority Interests: When a company has a minority interest in another firm and lacks significant influence or control over it, it may account for the investment using the equity method instead of fully consolidating.

- Held-for-Sale Entities: If a firm intends to sell one of its subsidiaries soon, it can classify it as held-for-sale and choose not to consolidate it.

- Investment Entities: Investment entities, like venture capital or private equity firms, may not need to consolidate their subsidiaries if their primary engagement involves holding investments and measuring them at fair value, not controlling their operations.

- Temporary Control: If the parent’s control over a subsidiary is temporary (e.g., the parent intends to sell or liquidate it soon, or was merely contracted to run its operations), consolidation might not be necessary.

For subsidiaries excluded from the consolidation process, their financial statements will be presented separately from the parent company’s consolidated statements.

Things to Avoid When Consolidating Financial Statements

Even one slight error or oversight during consolidation can lead to inaccurate financial reporting, compliance issues, and potential investor exit. Avoid these challenges by watching out for three key mistakes:

1. Miscounting Intra-Group Transactions

Failing to fully cancel intra-group transactions, like a parent company lending funds to a subsidiary, can lead to a misleading balance sheet. Prevent this scenario and create accurate reports by using financial software or the best statistical software to identify and remove duplicate entries.

2. Unaligned Reporting Periods

If subsidiaries use different fiscal year-ends than the parent company, it can cause misalignment in financial reports. For consistency, consolidate all entities under the same reporting period.

For example, Nestle operates in several countries and is prone to having subsidiaries with differing fiscal year-ends. To offset any differences and keep records aligned, the multinational consolidates all its divisions with a uniform 31 December reporting date.

3. Not Making Minority Interest Adjustments

Companies with subsidiaries in which they don't have full ownership must account for minority interests, even if that means recording them as distinct line items, as shown earlier. Failing to do so can misrepresent revenue and mislead investors.

Consolidate With Software

The consolidation of financial statements is complex, but using the right tools can enhance and speed up the process. Most companies use financial statement software to automate reporting compliance, intercompany eliminations, and data consolidation.

These systems allow CFOs to make financial statements compliant with regulatory requirements, less manual effort and human errors. Here are some of my top picks to help you get started:

Subscribe for More Financial Insights

I trust that this guide will make your job as a finance pro easier. But to help even more, I’m inviting you to subscribe to our free newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry. Join the community and start compounding your abilities today!

{kind=link}