10 Best Marketplace Payment Solutions in 2026

Best Marketplace Payment Solutions Shortlist

Marketplace payment solutions are platforms that let you collect, split, and disburse funds between buyers and multiple sellers or service providers on your marketplace. If you’re managing complex payouts, handling multi-currency transactions, or want to ensure compliance across regions, you need a purpose-built marketplace payment system. This guide zeroes in on top marketplace payment providers, breaking down where each fits best so you can reduce payment headaches, minimize risk, and keep vendors paid on time. You’ll leave with practical, up-to-date options to match your business model and growth plans.

Why Trust Our Software Reviews

We’ve been testing and reviewing financial software since 2023. As finance specialists ourselves, we know how critical and difficult it is to make the right decision when selecting software.

We invest in deep research to help our audience make better software purchasing decisions. We’ve tested more than 2,000 tools for different finance use cases and written over 1,000 comprehensive software reviews. Learn how we stay transparent & our software review methodology.

Best Marketplace Payment Solutions Summary

This comparison chart summarizes pricing details for my top marketplace payment solutions selections to help you find the best one for your budget and business needs.

| Tool | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Best for high-volume mass global payouts | Free demo available | From $99/month | Website | |

| 2 | Best for local payment methods worldwide | Not available | Pricing upon request | Website | |

| 3 | Best for creator and freelancer payments | 30-day free trial + free demo available | From $2,399/year | Website | |

| 4 | Best for regulated client fund safeguarding | Not available | From €0.40 + 0.30%/transaction | Website | |

| 5 | Best for automated vendor disbursements | Not available | Pricing upon request | Website | |

| 6 | Best for flexible platform-specific payment logic | Not available | Pricing upon request | Website | |

| 7 | Best for cross-border fund management | Free plan + free demo available | From $12/user/month | Website | |

| 8 | Best for global multi-currency settlements | Not available | From $0.13 processing fee + payment method fee | Website | |

| 9 | Best for programmable multi-vendor payouts | Not available | From 2.9% + 30¢/successful card charge | Website | |

| 10 | Best for established ecosystem integrations | Not available | Pricing upon request | Website |

-

Creatio CRM

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.7 -

DealHub AI

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.7 -

LiveFlow

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.9

Best Marketplace Payment Solutions Reviews

Below are my detailed summaries of the best marketplace payment solutions that made it onto my shortlist. My reviews offer a detailed look at the features, best use cases, and integrations of each platform to help you find the best one for you.

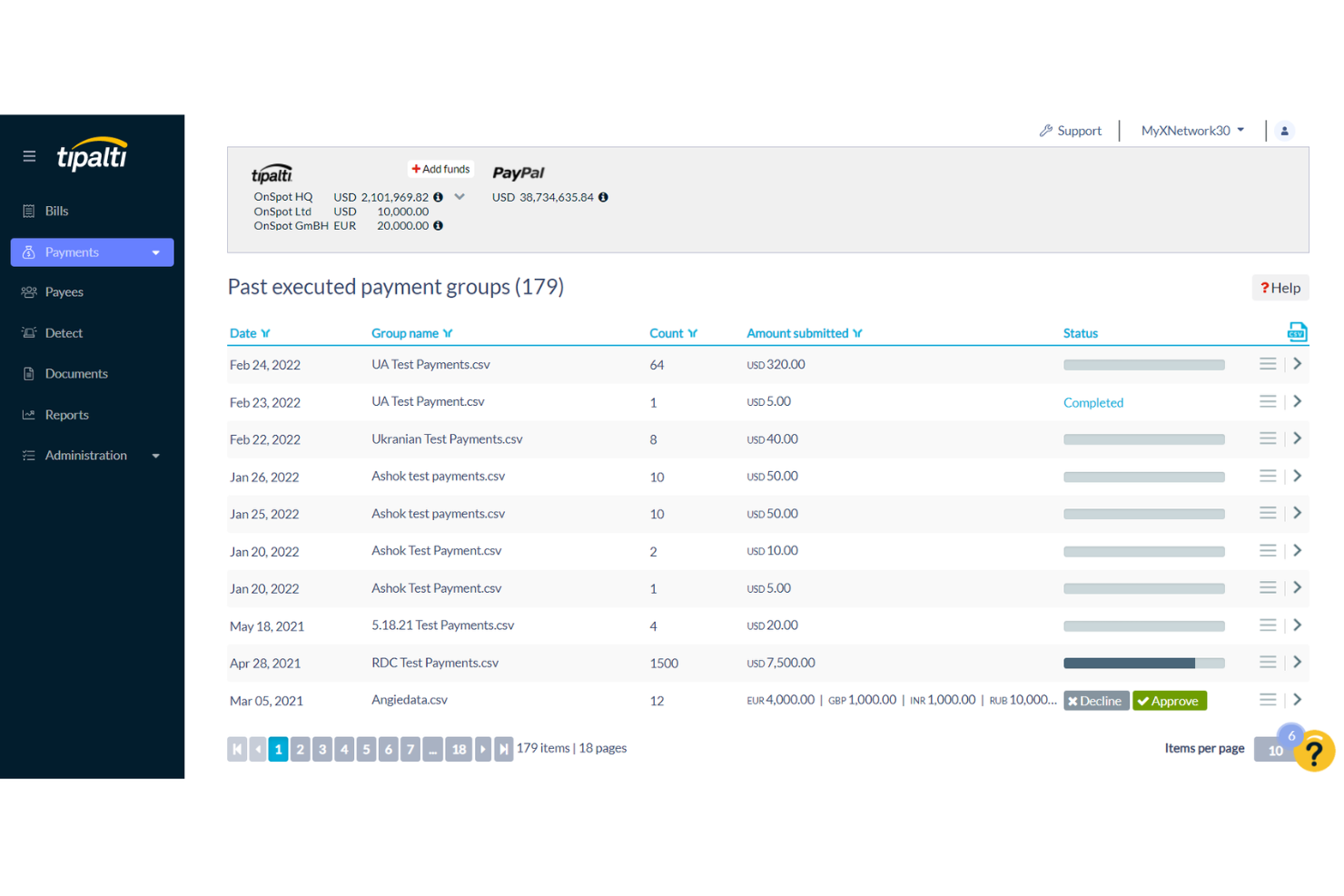

Tipalti is a payables automation platform that covers supplier onboarding, tax form collection, invoice management, and mass global payouts across 196 countries and 120 currencies.

Who Is Tipalti Best For?

Tipalti is a strong fit for mid-market and enterprise finance teams managing high volumes of cross-border payouts to creators, affiliates, or marketplace sellers.

Why I Picked Tipalti

I've included Tipalti in my top picks because its mass payment engine can process thousands of payee disbursements in a single batch across 196 countries. I particularly like its self-service payee portal, where marketplace sellers select their preferred payment method and currency during onboarding. Its automated tax form collection and 1099/1042-S preparation handle a compliance layer that most payment tools leave entirely to your finance team.

Tipalti Key Features

- Multi-entity support: Manage payables across multiple business entities from a single platform instance.

- Payment error detection: Flags invalid payee banking details before payments are processed to reduce failed transactions.

- FX management: Converts and sends payments in local currencies using mid-market exchange rates.

- Payment status tracking: Gives payees real-time visibility into their payment status through the self-service portal.

Tipalti Integrations

Tipalti offers native integrations with ERP and accounting systems, including NetSuite, Sage Intacct, Microsoft Dynamics, QuickBooks, Xero, SAP, Acumatica, and Workday. Additional connections cover Slack, BambooHR, and Okta. An API is available for custom integrations.

Pros and Cons

Pros:

- Built-in fraud detection flags suspicious activity

- Self-service payee onboarding with tax validation

- Batches cross-border payouts simultaneously

Cons:

- Reporting depth could be more granular

- Settlement takes 1-5 business days

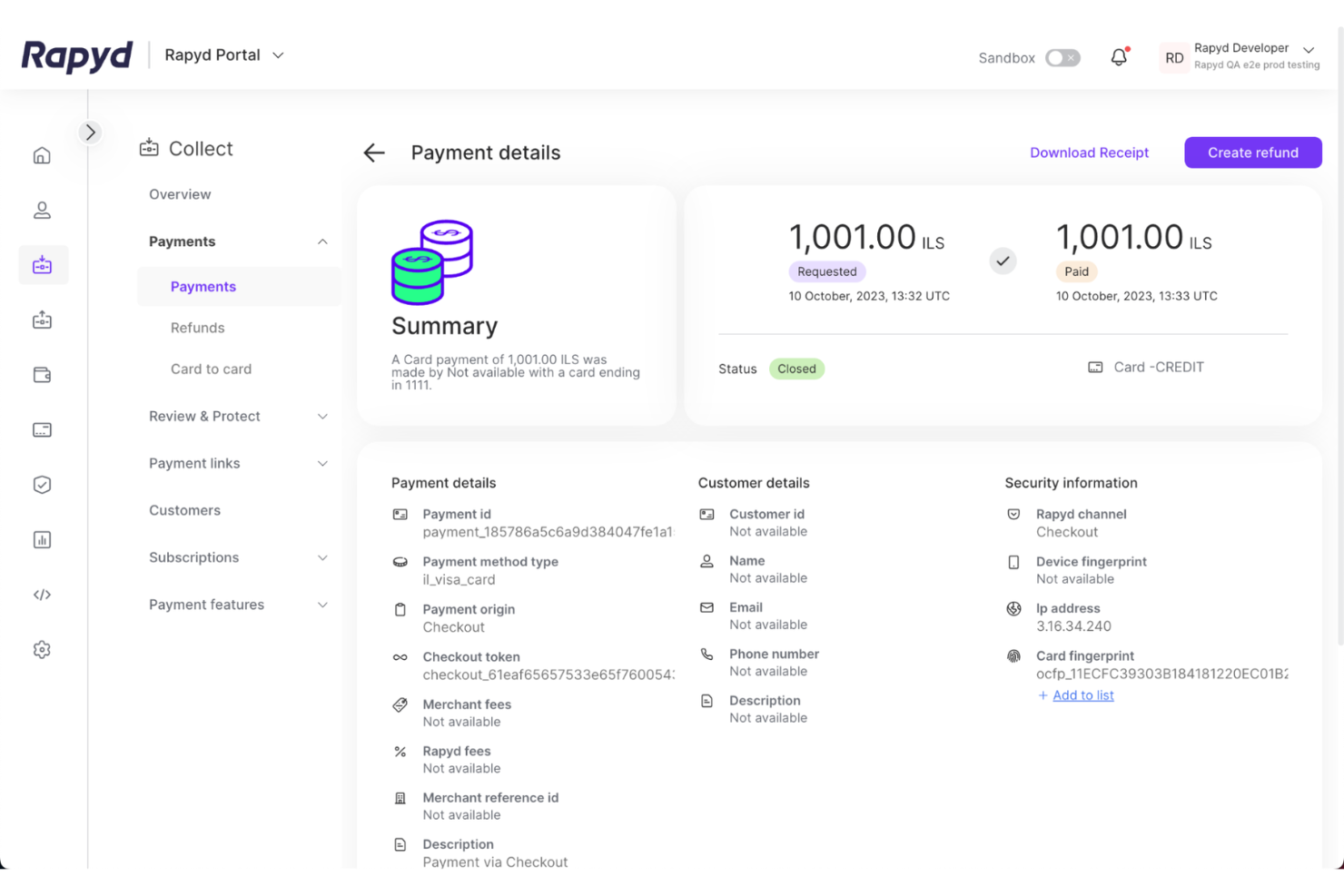

Rapyd is a fintech-as-a-service platform that lets marketplace operators accept payments, manage multi-currency wallets, and disburse funds to sellers across 190+ countries through a single API.

Who Is Rapyd Best For?

Rapyd is a strong fit for global marketplace platforms that need to accept and disburse payments across multiple regions without building separate local payment infrastructure.

Why I Picked Rapyd

Rapyd earns its spot on my shortlist because no other platform comes close to its depth of local payment method coverage, with 900+ options spanning cards, bank transfers, e-wallets, and cash-based methods across 100+ countries. I particularly like its local acquiring capabilities, which let marketplaces collect payments through in-country infrastructure rather than routing everything through international rails. That distinction matters when conversion rates in markets like Southeast Asia or Latin America are on the line.

Rapyd Key Features

- Rapyd Wallet: Lets marketplaces hold, manage, and transfer funds in multiple currencies within a digital wallet ledger.

- Mass payouts: Send batch disbursements to thousands of sellers or contractors across multiple countries simultaneously.

- Built-in FX conversion: Converts funds between currencies at the point of transaction using Rapyd's exchange rates.

- KYC/KYB verification: Verifies the identity of sellers and businesses during onboarding through built-in compliance checks.

Rapyd Integrations

Rapyd offers e-commerce plugins for Shopify, WooCommerce, Wix, Magento, Ecwid, OpenCart, and PrestaShop, making it easy to connect local payment methods to popular storefronts. An API is available for custom integrations, and Zapier support is not clearly documented.

Pros and Cons

Pros:

- Escrow and split payment API support

- Automates international compliance protocols

- Supports cash and e-wallet local rails

Cons:

- Ledger export features remain limited

- KYB onboarding process can take months

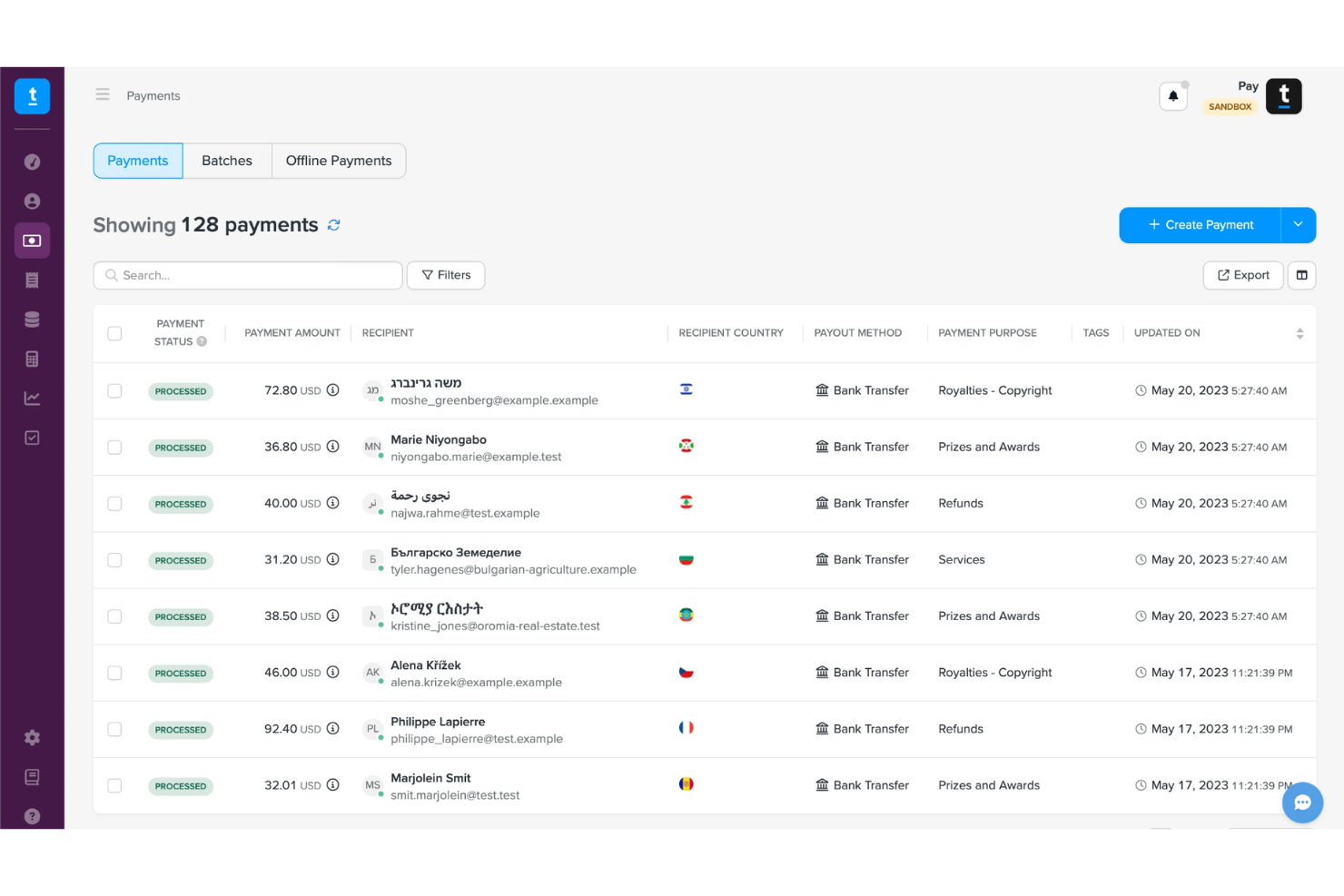

Trolley is a mass payout platform built for digital marketplaces and creator-economy businesses, covering recipient onboarding, tax compliance, global payment disbursement, and payment reconciliation in a single workflow.

Who Is Trolley Best For?

Trolley is a strong fit for digital media platforms, content marketplaces, and creator networks that pay large volumes of freelancers or contributors across multiple countries.

Why I Picked Trolley

Trolley earns its spot on my shortlist because of how well it handles the specific complexity of paying creators and freelancers at scale. I like that it combines self-serve recipient onboarding with W-9/W-8 tax form collection, so payees manage their own banking and tax details rather than routing requests through your finance team. The built-in 1099/1042-S filing means tax season doesn't require a separate workflow or third-party tool.

Trolley Key Features

- Batch payment processing: Send payments to thousands of recipients simultaneously via a single bulk upload or API call.

- Multi-currency disbursement: Pay recipients in their local currency across 200+ countries using multiple rails, including ACH, wire, and PayPal.

- Recipient payment portal: Give payees a branded self-serve portal to track payment history and manage their payout preferences.

- Sanctions and fraud screening: Automatically screen recipients against global watchlists before payments are processed.

Trolley Integrations

Trolley offers native integrations with QuickBooks Online, Xero, Oracle NetSuite, and Microsoft Dynamics 365, along with additional app connections including Salesforce, Slack, HubSpot, Shopify, Google Sheets, and Expensify. It connects with Zapier and provides an API for custom integrations.

Pros and Cons

Pros:

- White-labeled recipient onboarding widget available

- Handles batch payouts up to 20,000 recipients

- Built-in W-9/W-8 and 1099 tax automation

Cons:

- Payment status tracking lacks granular detail

- No real-time payment rails like PIX

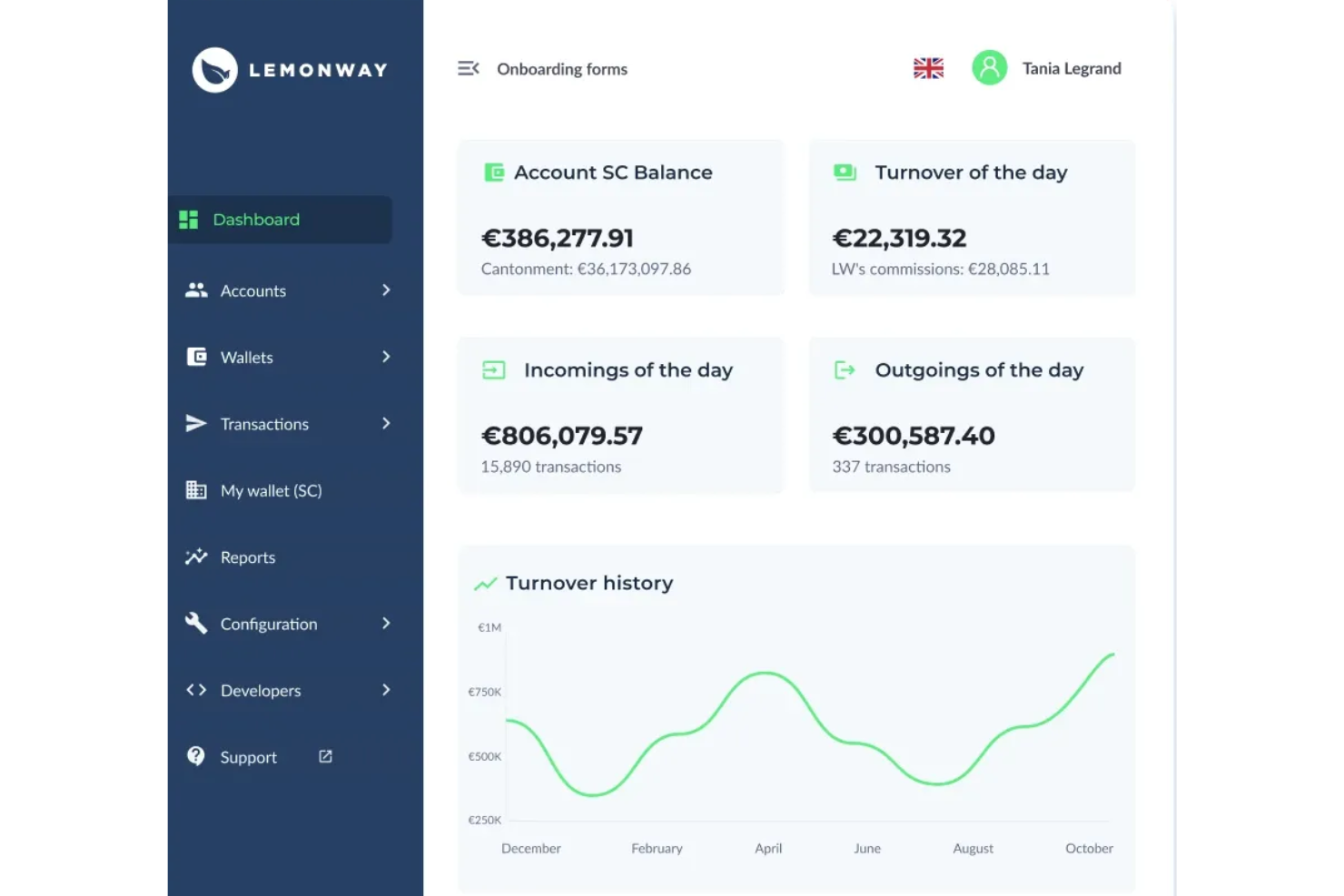

Lemonway is a marketplace-focused payment institution, licensed and regulated since 2012, that covers pay-in, digital wallet management, KYC-based seller onboarding, and pay-out through a modular API built specifically for marketplaces and platforms.

Who Is Lemonway Best For?

Lemonway is a strong fit for European marketplaces and crowdfunding platforms that need a licensed payment institution to handle regulated fund safeguarding, seller onboarding, and wallet management under ACPR supervision.

Why I Picked Lemonway

Lemonway earns its spot on my shortlist because its approach to client fund safeguarding goes beyond a policy checkbox. As an ACPR-licensed payment institution, it ringfences marketplace funds at the account level under PSD2, meaning your sellers' money is legally isolated from your operating funds at all times. I also like the wallet reconciliation layer, which matches Pay-In and Pay-Out flows per merchant automatically, making it much easier to audit fund movements across a platform with hundreds of sellers.

Lemonway Key Features

- KYC online onboarding: Validates individual seller identities in under two minutes and processes legal entities within 48 hours, with automated document collection across 150+ countries.

- Multi-method Pay-In support: Accepts card payments, SEPA direct debit, bank transfers (including virtual IBAN), BNPL, PayPal, Apple Pay, and local payment methods like MB WAY.

- AML and PEP screening: Combines AI and human review to flag politically exposed persons and individuals under sanctions during the onboarding and transaction flow.

- Real-time transaction dashboard: Lets you monitor all marketplace payment flows, track KPIs, and manage user accounts from a single back-office view.

Lemonway Integrations

Lemonway offers plugins for Mirakl and Magento (Adobe Commerce), along with a hosted card payment fields SDK and a customizable payment page. An API is available for custom integrations, and Lemonway also partners with PayPal for marketplace pay-ins.

Pros and Cons

Pros:

- Virtual IBAN provisioning for seller accounts

- Multicapture support for mixed-cart checkouts

- Licensed payment institution with EU passport

Cons:

- Service uptime can affect platform operations

- Infrastructure relies on constant maintenance

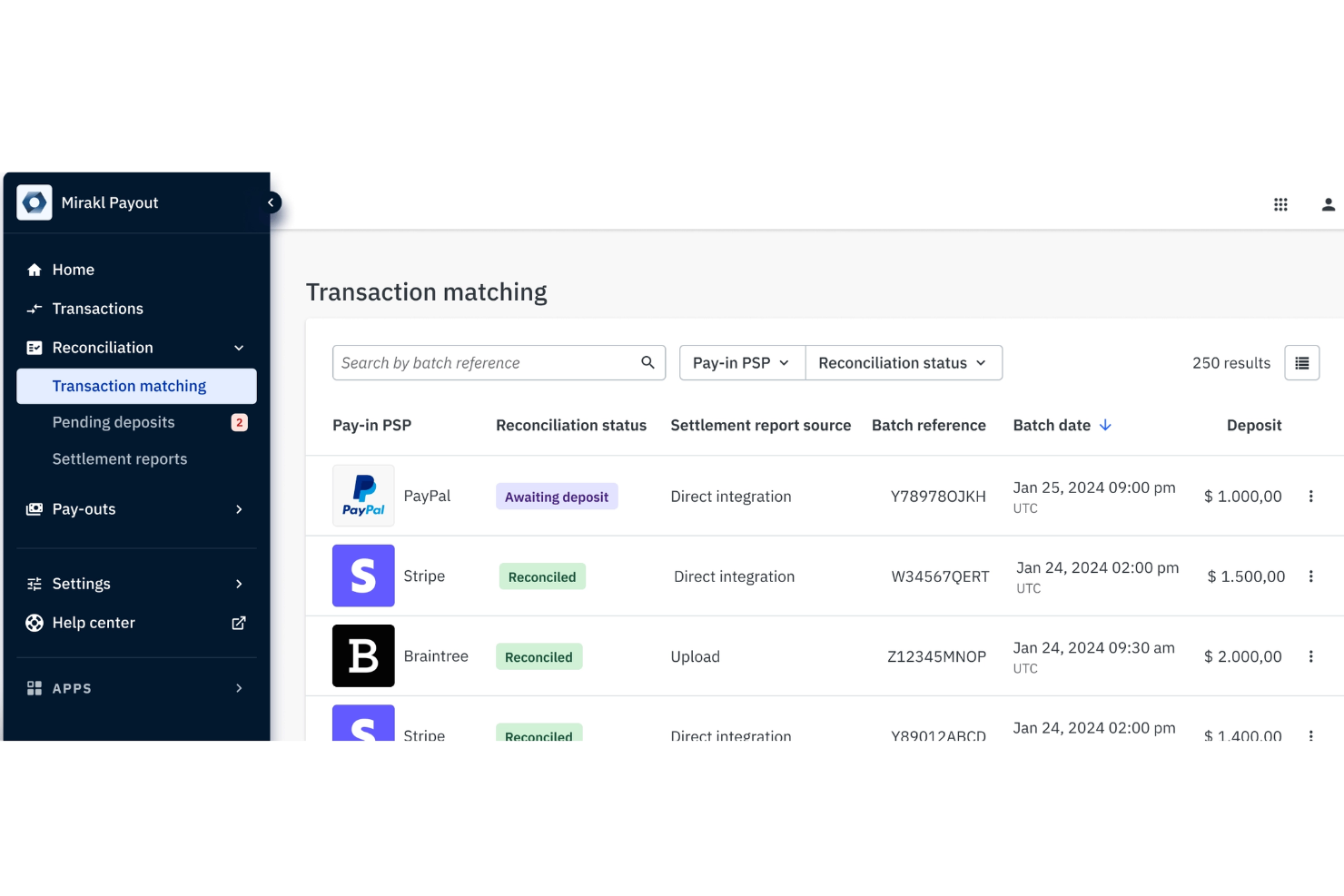

Mirakl Payout is a marketplace payout platform that handles automated vendor disbursements, seller KYC onboarding, multi-currency foreign exchange, and first- and third-party fund reconciliation across U.S. and EU regulatory frameworks.

Who Is Mirakl Payout Best For?

Mirakl Payout is built for enterprise marketplace operators already running on the Mirakl platform who need to manage cross-border vendor disbursements under both U.S. and EU regulatory frameworks.

Why I Picked Mirakl Payout

I picked Mirakl Payout as one of the best because its disbursement automation is native to the Mirakl back-office, so there's no middleware to manage between your marketplace order data and your vendor payment runs. I like that it handles first-party and third-party fund reconciliation in a single workflow, which removes a significant manual step in the close cycle. Its automated KYC layer also runs within the same disbursement flow, so seller onboarding doesn't create a bottleneck before payouts can begin.

Mirakl Payout Key Features

- Multi-currency foreign exchange: Automatically handles currency conversion across seller payment runs while maintaining regional regulatory compliance.

- Regulated escrow management: Holds and manages funds in a regulated escrow environment as part of the seller payment workflow.

- Centralized administrative workflows: Manage end-to-end payments from a single administrative interface regardless of seller location.

- Preserved pay-in provider relationships: Lets you add pay-out capabilities without replacing your existing pay-in PSP setup.

Mirakl Payout Integrations

Mirakl Payout integrates with Mangopay and offers connectivity to major ecommerce platforms including Adobe Commerce, SAP, Salesforce, Oracle, and BigCommerce. APIs and pre-built connectors are also available for custom integration requirements.

Pros and Cons

Pros:

- Supports multi-currency seller payouts natively

- Handles U.S. and EU regulatory compliance

- Native KYC built into the disbursement workflow

Cons:

- API documentation gaps slow custom implementations

- Only available to Mirakl platform customers

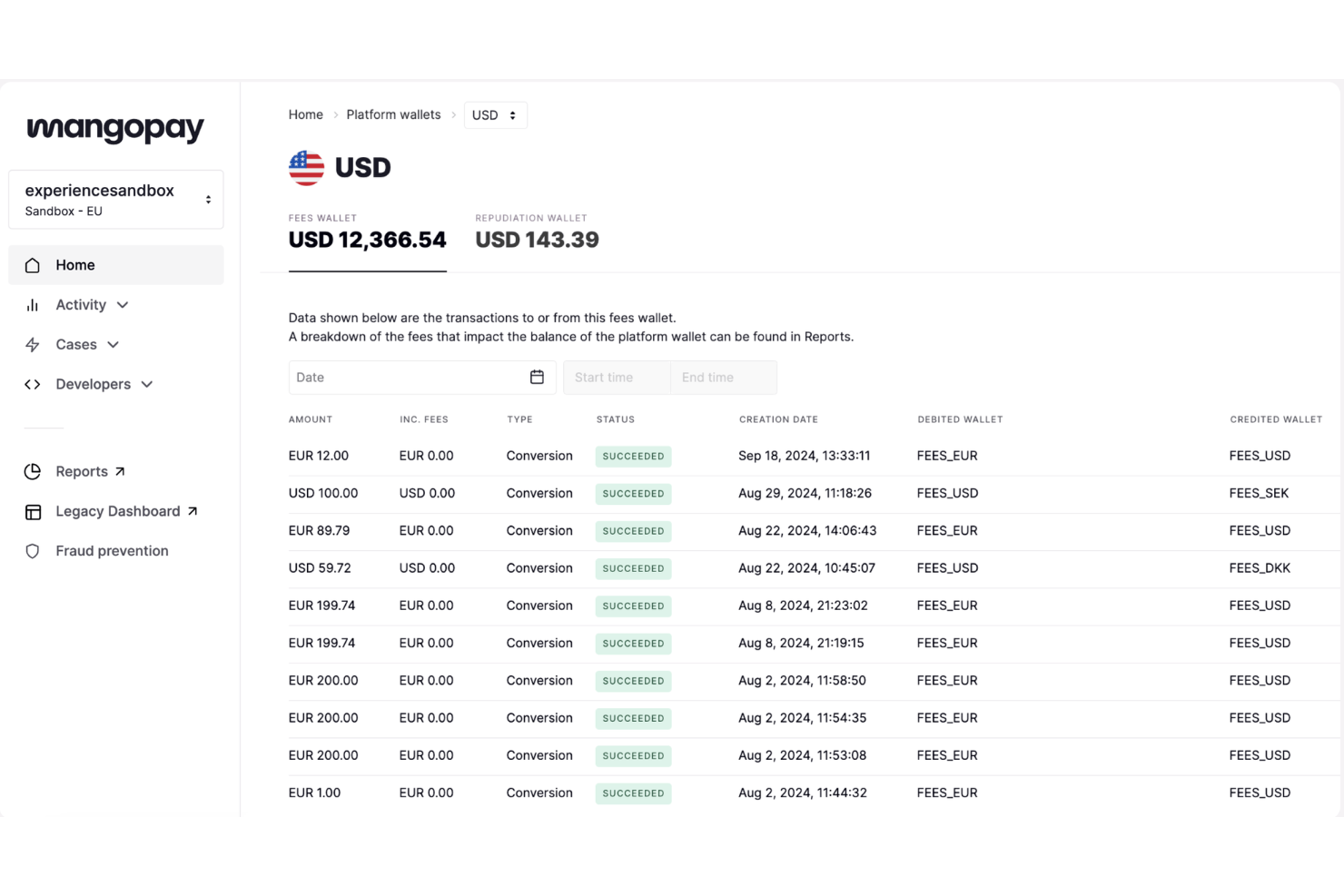

MANGOPAY is a wallet-based payment infrastructure platform built for multi-party platforms and marketplaces, covering pay-ins, wallet management, FX, virtual IBANs, identity verification, fraud detection, and global payouts.

Who Is MANGOPAY Best For?

MANGOPAY is a strong fit for platform and marketplace businesses in fintech, lending, crowdfunding, and the gig economy that need modular, API-first payment infrastructure.

Why I Picked MANGOPAY

I picked MANGOPAY as one of the best because of how much control it gives you over payment logic at the platform level. What stands out is the wallet-as-building-block model: you can insert wallets at any stage of a payment flow, assign them to specific use cases like escrow, refunds, or FX, and configure fund movement rules per wallet type. I also like that MANGOPAY lets you accept pay-ins from multiple acquirers simultaneously, so you're not locked into a single provider and can switch or combine them without rebuilding your integration.

MANGOPAY Key Features

- KYC/KYB identity verification: Verify individual users and businesses in over 190 countries using live document capture, liveness checks, and real-time data validation against trusted sources.

- AI-powered fraud detection: A built-in fraud engine analyzes behavioural signals, device fingerprints, and darknet data to flag fraud at registration, checkout, and payout.

- Virtual IBANs: Attach multiple IBANs directly to individual wallets to collect funds from external acquirers and automate reconciliation at the wallet level.

- Automated payment reconciliation: Each wallet carries a unique identifier, making transaction-level reconciliation instant without manual matching.

MANGOPAY Integrations

MANGOPAY offers an official connector for Mirakl to automate seller onboarding and split payouts for Mirakl-powered marketplaces. Beyond that, MANGOPAY is primarily an API-first platform with server-side SDKs in Node.js, PHP, Python, .NET, Java, and Ruby, and Zapier support is not clearly documented.

Pros and Cons

Pros:

- EU-regulated with segregated fund handling

- Built-in FX rate locking at checkout

- Programmable wallets for multi-party fund flows

Cons:

- High minimum monthly fees for smaller platforms

- Lacks advanced data export options

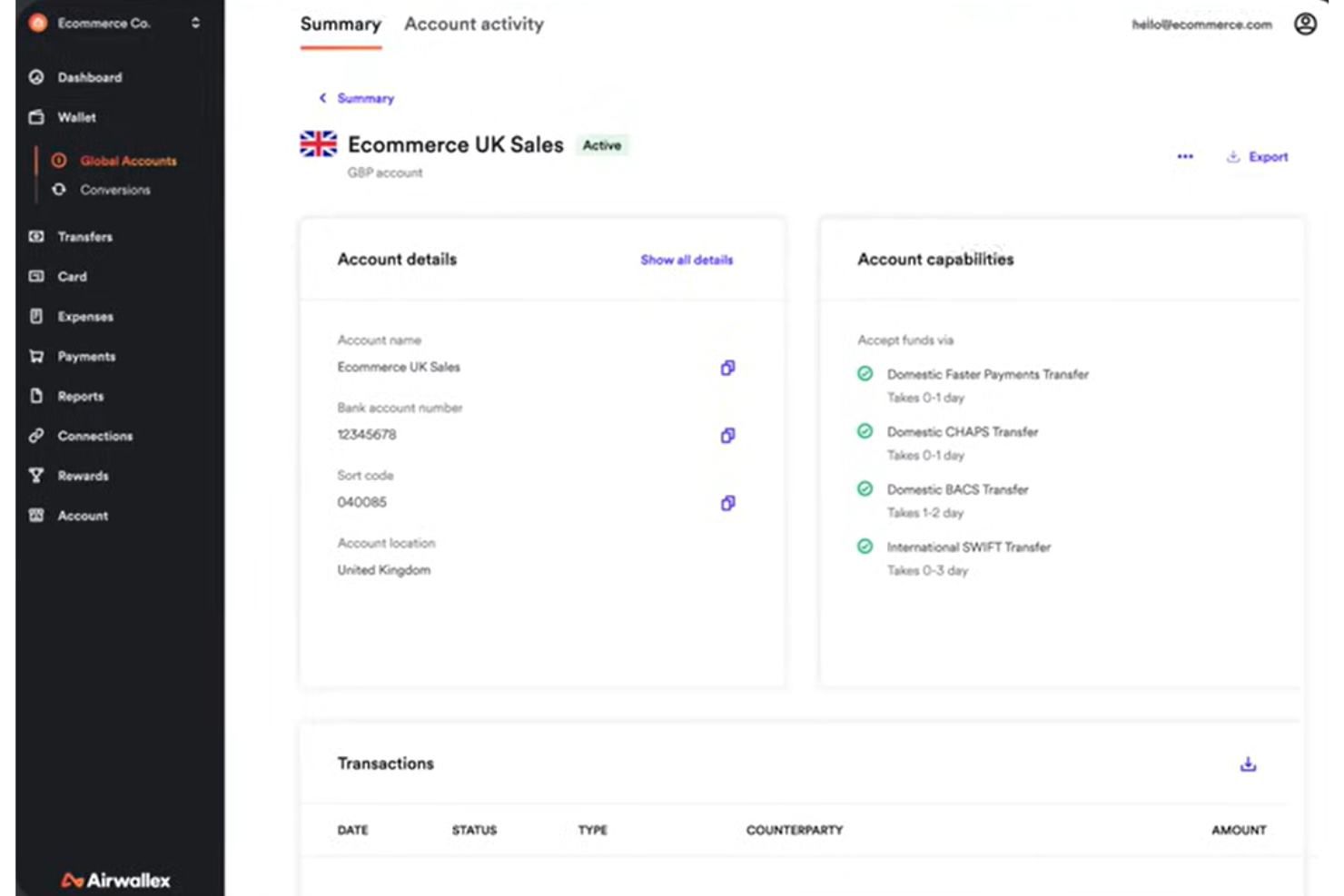

Airwallex is a global payments platform that covers multi-currency pay-ins, like-for-like settlement, local acquiring across 35+ markets, and embedded payment infrastructure for online marketplaces and platforms.

Who Is Airwallex Best For?

Airwallex is a strong fit for scaling marketplaces and platforms that operate across multiple countries and need to collect, hold, and pay out in local currencies.

Why I Picked Airwallex

I picked Airwallex as one of the best for cross-border fund management because its like-for-like settlement feature genuinely solves a problem most marketplace platforms paper over. You collect in GBP, hold in GBP, and pay out in GBP without a forced conversion back to your home currency. That matters if your sellers or suppliers are spread across multiple countries. I also like that local acquiring across 35+ markets reduces cross-border processing fees at the authorization layer, not just at settlement.

Airwallex Key Features

- Connected accounts: Programmatically create and onboard sub-accounts for marketplace sellers or platform users, with compliance handled at the account level.

- Network tokenization: Replaces stored card details with network-issued tokens to improve card acceptance rates and cut processing costs on repeat transactions.

- Subscription management: Handles simple and hybrid multi-frequency subscription pricing models, including billing cycle logic and recurring payment execution.

- AI-powered fraud engine: Flags suspicious transactions and reduces chargebacks using an ML-based fraud detection layer built directly into the payment flow.

Airwallex Integrations

Airwallex offers native integrations with Xero, QuickBooks, NetSuite, Shopify, WooCommerce, Magento, Amazon, Shopee, Salesforce Commerce Cloud, and Microsoft Dynamics 365 Business Central, and it connects with Zapier. An API is also available for custom integrations.

Pros and Cons

Pros:

- Automates multi-currency payouts to marketplace sellers

- Multi-currency accounts replace bank setups

- Well-documented API for multi-currency workflows

Cons:

- Frequent compliance account holds

- KYC onboarding rejections lack detailed explanations

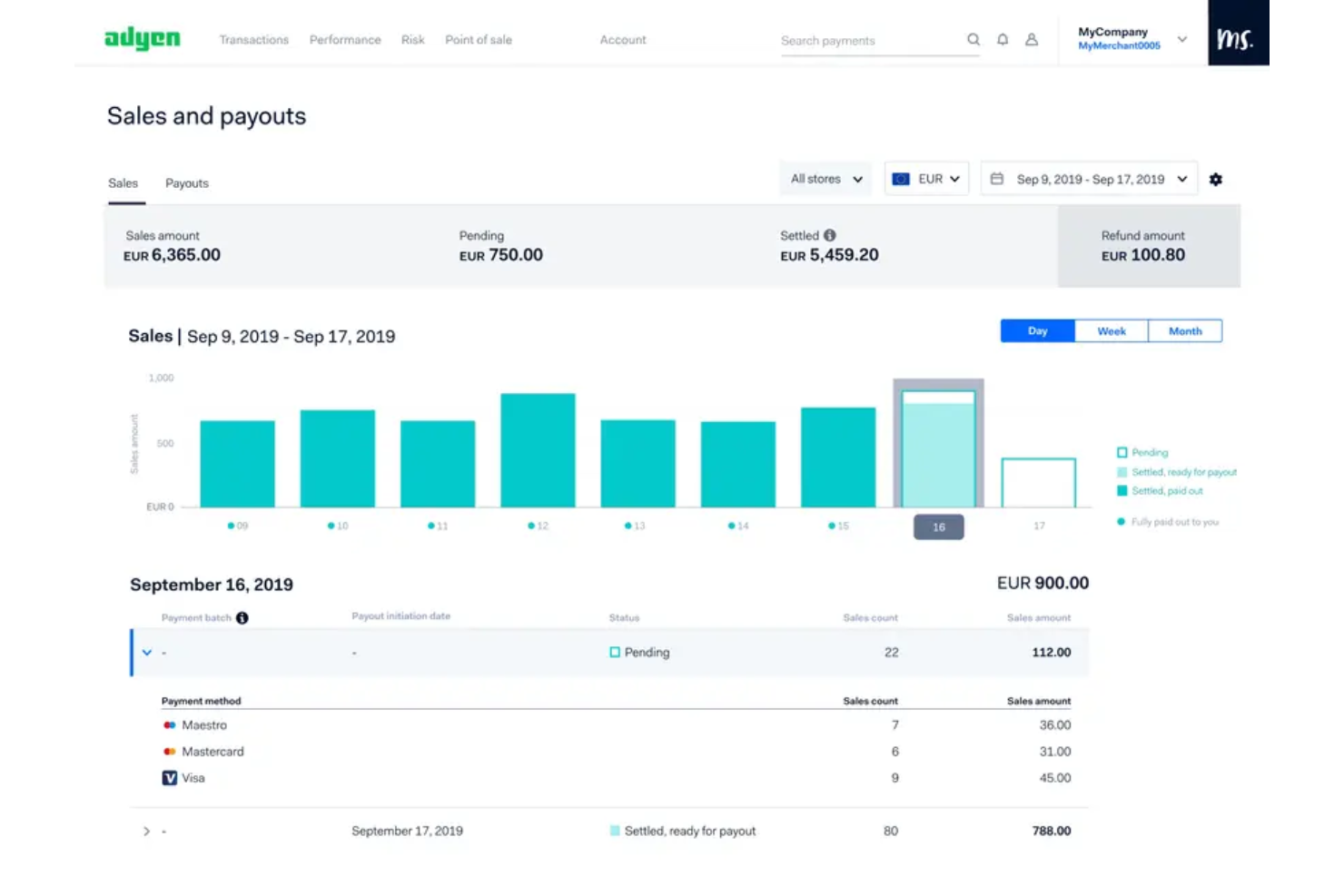

Adyen is a global payments platform purpose-built for SaaS platforms and marketplaces, combining payment acceptance, multi-currency settlement, automated payouts, and embedded financial products in a single API.

Who Is Adyen Best For?

Adyen is a strong fit for enterprise-scale platforms and marketplaces operating across multiple countries that need unified payment infrastructure and local settlement capabilities.

Why I Picked Adyen

Adyen earns its spot on my shortlist because of how it handles cross-border settlement at scale. It holds local acquiring licenses in 40+ countries, so transactions are processed in-market rather than routed through a single hub, which directly improves authorization rates. I also like that Adyen for Platforms handles payouts to vendors in their local currency automatically, removing the manual FX reconciliation that trips up most multi-region marketplace operators.

Adyen Key Features

- Split payments: Automatically divide a single transaction across multiple sellers or service providers at checkout.

- Balance accounts: Assign individual digital wallets to each sub-merchant for fund management and controlled disbursements.

- RevenueProtect: A built-in risk engine that applies customizable fraud rules at the transaction level across all connected sellers.

- Local payment methods: Accept 100+ local payment methods, including digital wallets and bank transfers, tailored by market.

Adyen Integrations

Adyen offers native plugins for major platforms like Adobe Commerce, Salesforce Commerce Cloud, and Oracle. Partner-built plugins extend connectivity to Shopify, WooCommerce, BigCommerce, Microsoft Dynamics 365, and others. An API is available for custom integrations.

Pros and Cons

Pros:

- ML-based fraud engine with smart transaction routing

- Split payments across multiple sub-merchants

- Local acquiring improves cross-border authorization rates

Cons:

- Advanced menu setups need heavy technical work

- Enforces standardized platform architecture

Stripe Connect is a marketplace payment infrastructure platform that lets you build multi-party payment flows, manage seller onboarding, and configure custom payout logic across connected accounts.

Who Is Stripe Connect Best For?

Stripe Connect is a strong fit for developer-led teams building marketplace or platform products that need granular control over payment routing and seller account management.

Why I Picked Stripe Connect

Stripe Connect is one of my top picks because I love how granular the payout configuration gets. Using the API, I can set custom payout schedules per vendor, define split logic across multiple recipients on a single charge, and choose between destination charges or separate transfers depending on how funds need to flow. The Connect account model also gives me control over how much of the payment experience each seller sees.

Stripe Connect Key Features

- Hosted onboarding: Pre-built KYC and identity verification flows let sellers complete account setup without custom development.

- Stripe Radar: Machine learning-based fraud detection screens payments across all connected accounts using configurable rules.

- Multi-currency settlement: Accept payments in 135+ currencies and settle connected accounts in their local currency.

- 1099 tax form generation: Automatically generate and file 1099 forms for US-based sellers directly from the dashboard.

Stripe Connect Integrations

Stripe Connect offers hundreds of marketplace integrations through the Stripe App Marketplace, including QuickBooks, Xero, DocuSign, Mailchimp, Intercom, Salesforce, and Slack. It's also available on Zapier and provides a well-documented API for custom integrations.

Pros and Cons

Pros:

- Built-in seller onboarding and KYC verification

- Supports 135+ currencies natively

- Highly flexible API for custom payment flows

Cons:

- Requires manual claim investigation

- Requires developer resources to implement fully

PayPal Enterprise Payments is a payment processing platform for large-scale businesses and marketplaces, covering pay-ins, payouts, fraud protection, and multi-currency transactions across PayPal, Venmo, and major card networks.

Who Is PayPal Enterprise Payments Best For?

PayPal Enterprise Payments is a strong fit for large ecommerce platforms and global marketplaces that already operate within the PayPal and Braintree ecosystem.

Why I Picked PayPal Enterprise Payments

PayPal Enterprise Payments earns its spot on my shortlist because of the sheer breadth of its built-in ecosystem. I like that a single integration gives you access to PayPal, Venmo, Fastlane, Pay Later, and local payment methods simultaneously, without separate contracts or technical builds for each. The payment orchestration layer also lets you work across multiple acquirers, vaulting, and tokenization from one platform, which is a level of pre-wired infrastructure most marketplace-focused tools don't offer out of the box.

PayPal Enterprise Payments Key Features

- Fraud Protection Advanced: A machine learning-based fraud scoring tool that evaluates every transaction and lets you set custom rules to block, allow, or review payments.

- Mass payouts via Hyperwallet: Send bulk disbursements to marketplace sellers, gig workers, or partners across 200+ markets in local currencies.

- Split payments: Divide a single transaction across multiple parties, such as a seller and a platform fee, at the time of checkout.

- Dispute and chargeback management: A built-in resolution center for handling buyer disputes, chargeback responses, and refund tracking across transactions.

PayPal Enterprise Payments Integrations

PayPal Enterprise Payments connects with ecommerce platforms like WooCommerce, BigCommerce, Shopware, Shopify, and Magento through its partner directory, which also covers accounting, recurring payments, and POS categories. It connects with Zapier and offers REST APIs and SDKs for custom integrations.

Pros and Cons

Pros:

- Handles multi-country transactions at scale

- Sandbox testing for marketplace developers

- Accepts PayPal, Venmo, and cards together

Cons:

- Account reviews can freeze fund access

- Support tickets prioritize large accounts

Other Marketplace Payment Solutions

Here are some additional marketplace payment solutions options that didn’t make it onto my shortlist, but are still worth checking out:

- Online Payment Platform (OPP)

For compliance-driven platform operations

- Hyperwallet

For payee prepaid card options

- Payoneer

For global vendor onboarding support

- Fondy

For single-account multi-currency split

- Checkout.com

For modular API-driven payment infrastructure

- Mollie

For fast onboarding of European merchants

- Nium

For embedded fintech payouts to bank accounts

- Razorpay Route

For automated split payments in India

{kind=link}

How I Evaluate Marketplace Payment Solutions

I split my evaluation into two layers: the baseline capabilities a platform needs to handle multi-party splits and seller KYC, and the factors that set one apart.

Core Functionality (Table Stakes for This List)

When I'm selecting tools for my list, I rank each one on a scale from 0 (does not offer the functionality) to 5 (excels in this area) for each core functionality listed below. Then, I calculate the tool's total score as a percentage. Each tool needs to achieve a minimum total score of 65% to be considered for inclusion.

- Split Payments: I look at how each platform divides a single buyer transaction across sellers, platform fees, and third parties like tax authorities or affiliates, and whether split rules can be adjusted in real time.

- Multi-Party Payouts: Payout flexibility matters here, so I evaluate the range of rails supported (bank transfer, card, wallet, instant) and whether the platform can automate scheduled payouts to sellers across regions.

- Seller Onboarding & KYC: I check whether the platform provides built-in KYC/KYB verification and AML screening, including tiered workflows that let low-risk sellers start transacting quickly while flagging higher-risk accounts.

- Multi-Currency & Cross-Border: For marketplaces with international sellers, I evaluate FX handling, local acquiring capabilities, and whether sellers can receive payouts in their local currency and preferred banking method.

- Escrow & Funds Holding: This covers how the platform holds buyer funds until conditions like delivery confirmation or dispute windows are met, which directly impacts chargeback exposure and seller trust.

- Reconciliation & Reporting: I look for transaction-level reporting across all parties in a flow, ledger exports that map to accounting workflows, and whether the platform supports the kind of multi-party reconciliation finance teams need at month-end.

Once I have a list of tools that meet this criterion, I consider what sets each platform apart.

Differentiating Factors (What Sets Vendors Apart)

Here's how I compare and contrast different vendors:

Standout Features

I pay close attention to how each platform handles escrow and delayed payouts, since the ability to hold funds until delivery or dispute resolution directly affects chargeback exposure. Embedded financial services also matter—features like instant payouts or seller cash advances can turn your marketplace into a retention tool. Beyond that, I evaluate how well a split payments engine adapts to complex flows involving multiple sellers, platform commissions, and tax withholding in one transaction.

Beyond Features

Regulatory burden is a major differentiator. I evaluate whether the provider operates as a merchant of record or payment facilitator, since that determines how much licensing and compliance work falls on your team. Pricing transparency also varies widely—I look at how clearly a vendor breaks down transaction fees, FX margins, and chargeback costs, especially for high-volume marketplaces where hidden charges compound fast. Developer experience rounds out my assessment: strong sandbox environments and reliable webhooks mean faster launches and fewer integration headaches during migration.

How to Choose Marketplace Payment Solutions

It’s easy to get bogged down in long feature lists and complex pricing structures. To help you stay focused as you work through your unique software selection process, here’s a checklist of factors to keep in mind:

| Factor | What to Consider |

| Scalability | Can the solution grow with your marketplace as transaction volumes, currencies, and seller count increase? Check for rate limits and roadmap alignment. |

| Integrations | Does the platform connect easily with your ERP, accounting, and CRM tools? Consider the quality of available APIs and support for webhooks. |

| Customizability | Are you able to tailor workflows, payout schedules, reporting, and user roles to your business model and operating markets? |

| Ease of use | How simple is it for finance, support, and ops teams to manage payouts and track issues? Ask to see the actual dashboard and reporting workflows. |

| Implementation and onboarding | What onboarding support and migration resources does the provider offer? Review documentation and roadmaps for getting sellers up and running fast. |

| Cost | Go beyond headline rates—model transaction and payout fees, FX margins, and possible hidden costs for edge cases or international transactions. |

| Security safeguards | Assess controls for payment data, KYC, access management, and fraud monitoring. Check for certifications and regular security audits. |

| Compliance requirements | Does the vendor’s legal/compliance model reduce your own regulatory burden? Ask about KYC, AML, tax form generation, and cross-border money movement. |

What Are Marketplace Payment Solutions?

Marketplace payment solutions are specialized payment platforms designed to automate and manage payments between buyers, sellers, and platform operators within multi-party marketplaces. These solutions combine split payments, seller onboarding, compliance checks, multi-currency support, escrow services, and reconciliation tools, helping you handle complex marketplace transactions while reducing manual work and regulatory risk.

Features of Marketplace Payment Solutions

When selecting marketplace payment solutions, keep an eye out for the following key features:

- Split payments: Automatically allocate funds from a single buyer transaction to multiple sellers, platform fees, and tax accounts without manual calculation.

- Multi-party payouts: Disburse funds to various sellers or vendors using preferred payment methods like bank transfer, card, or digital wallets across different regions.

- Seller onboarding and KYC: Built-in verification tools for quick, compliant onboarding of individual and business sellers, including identity checks and AML screening.

- Escrow and funds holding: Temporarily hold and release funds based on conditions like delivery confirmation or dispute resolution, reducing fraud and chargeback risks.

- Multi-currency support: Accept payments and make payouts in a wide range of currencies, allowing for international expansion and seller flexibility.

- Automated reconciliation: Generate transaction-level ledger entries and export them for easy syncing with accounting or ERP systems, enabling accurate reporting.

- Configurable fee structures: Set and manage commission rates, service fees, and tax withholdings specific to your marketplace model and regulatory requirements.

- Regulatory compliance tools: Manage KYC, AML, and tax reporting needs, including forms generation and audit trails to help satisfy local and international regulations.

- Customizable payment workflows: Tailor payout schedules, hold periods, and approval processes to fit different business models and operational needs.

- Advanced fraud detection: Use machine learning or rules-based monitoring to flag suspicious transactions, set risk thresholds, and automate responses to protect your marketplace.

Benefits of Marketplace Payment Solutions

Implementing marketplace payment solutions provides several benefits for your team and your business. Here are a few you can look forward to:

- Simplified multi-party settlements: Automate split payments and payouts, so your team avoids manual calculations and complex reconciliations.

- Faster seller onboarding: Built-in KYC and verification tools speed up onboarding, letting new sellers start transacting with minimal friction.

- Improved global reach: Multi-currency support and local payout options help attract and retain sellers and buyers across borders.

- Stronger compliance posture: Integrated KYC, AML, and tax reporting features help you keep up with changing regulations and reduce legal risks.

- Reduced fraud and chargebacks: Escrow, advanced fraud tools, and conditional payout workflows protect your business and sellers from losses.

- Smooth financial reporting: Transaction-level data, ledger exports, and configurable reports make accounting and month-end close much more efficient.

- Better seller experience: Customizable payout schedules and embedded financial services—like instant payouts—help boost seller loyalty and retention.

Costs and Pricing of Marketplace Payment Solutions

Selecting marketplace payment solutions requires an understanding of the various pricing models and plans available. Costs vary based on features, team size, add-ons, and more. The table below summarizes common plans, their average prices, and typical features included in marketplace payment solutions:

Plan Comparison Table for Marketplace Payment Solutions

| Plan Type | Average Price | Common Features |

| Free Plan | $0 | Limited split payments, basic seller onboarding, transaction caps, and minimal support. |

| Personal Plan | $20-$50/month | Split payments, simple onboarding and KYC, basic reporting, transaction limits, and email support. |

| Business Plan | $100-$400/month | Advanced split payments, enhanced KYC, multi-currency support, payout customization, and analytics. |

| Enterprise Plan | $1000+/month | Custom workflows, dedicated account management, advanced compliance, API access, and premium support. |

Marketplace Payment Solutions FAQs

Here are some answers to common questions about marketplace payment solutions:

How do marketplace payment solutions manage split payments?

Marketplace payment solutions use split payment engines to automatically distribute funds from a single transaction between multiple sellers, the platform, and any required taxes or fees. This helps process payments quickly, eliminates manual calculations, improves cash flow, and reduces the risk of reconciliation errors.

Can marketplace payment solutions help with tax compliance?

Yes, many all-in-one options offer built-in tools for 1099-K, VAT, or GST form generation, as well as automated tax withholding and reporting features. This payment service supports compliance for both domestic and international transactions, reducing the burden on your finance team.

What security safeguards do these platforms provide?

Most providers include PCI DSS compliance, fraud prevention, access controls, and regular security audits to ensure secure payment. Some also offer advanced tools like 3D Secure, machine learning-based fraud monitoring, strong user authentication, and secure onboarding processes to protect both your business and your users.

Are there options for international payouts?

Yes, leading marketplace payment gateway solutions typically support multi-currency transactions and local payment options, so you can pay sellers in their preferred currencies and regions. This flexible payment processor setup allows you to optimize international operations. Look for platforms with wide country coverage, real-time notifications, and clear FX fees.

How do these solutions support seller onboarding?

Many solutions offer onboarding tools with built-in KYC and AML screening, allowing sellers to register, verify their identity, and begin taking mobile payments quickly. This improves the overall user experience so they can accept a credit card, debit card, or Google Pay for both digital and in-person transactions without creating extra manual work for your team.