Your Ultimate Guide to Impairment of Goodwill

Goodwill Impairment, Explained: Goodwill arises when a company is acquired above its market value, while impairment is noted when the acquisition's fair value dips below its book value.

Test Away!: To check goodwill impairment, you need to identify the reporting unit, determine if a qualitative assessment is necessary, and then perform the test.

Staying Ahead: Keep updated on the ASC 350, SEC Staff Accounting Bullet Topic 5, IAS 36, and more to make sure you're notified of any changes in reporting regulations and requirements.

Back when I was an accountant, few topics sparked more confusion—or anxiety—than goodwill impairment. It’s one of those terms that shows up on the income statement and makes even seasoned professionals pause. But behind the jargon is a concept that tells a very human story: a deal that didn’t quite go as planned.

Goodwill impairment isn’t just a regulatory requirement—it’s a signal to stakeholders that the value of an acquisition has dropped. And while it plays a critical role in financial transparency, it often gets looked over in favor of more familiar expenses.

In this guide, I’ll walk you through goodwill and goodwill impairment using insights from my years in the field. Whether you’re brushing up or starting fresh, you’ll learn what it is, how it’s accounted for, and how to calculate an impairment loss—without getting lost in accounting speak.

Need expert help selecting the right tool?

With one-on-one help, we guide you to your top software options. Narrow down your software search & make a confident choice.

What Is Impairment of Goodwill in Accounting?

Goodwill impairment occurs when the book value of goodwill (an indefinite-lived intangible asset) in your balance sheet exceeds its fair value and must be written down.

The amount of goodwill is only recorded when a company is acquired for more than its fair market value. It’s never self-generated. In contrast, a potential impairment charge is recorded when the fair value of that acquired reporting unit drops below the book value.

Take AT&T’s acquisition of DirecTV, for example. AT&T acquired DirecTV for $48.5 billion in 2015. However, subsequently, AT&T recorded a $15.5 billion goodwill impairment charge on the acquisition as DirecTV’s fair value declined below its book value.

The Importance of Impairment of Goodwill

There are three perspectives that the importance of goodwill impairment can be viewed from:

- Financial Transparency: Investors see goodwill as a premium you paid to acquire a company that can generate great returns and justify the premium. Impairment is a clear signal that, in its current state, the acquisition is not performing as planned.

- Valuation: Free cash flows from the reporting unit are factored into your company’s value. An impairment changes an investor’s estimate of growth and future cash flows from the reporting unit, potentially leading to a decline in your company’s value.

- M&A Discipline: Both GAPP and IFRS require companies to test for goodwill impairment at least annually. If you’re acquiring a company and thinking about paying a premium, the thought of justifying the impairment to investors later may force you to reconsider. That’s why impairment provisions are a great way to highlight overpriced deals to investors.

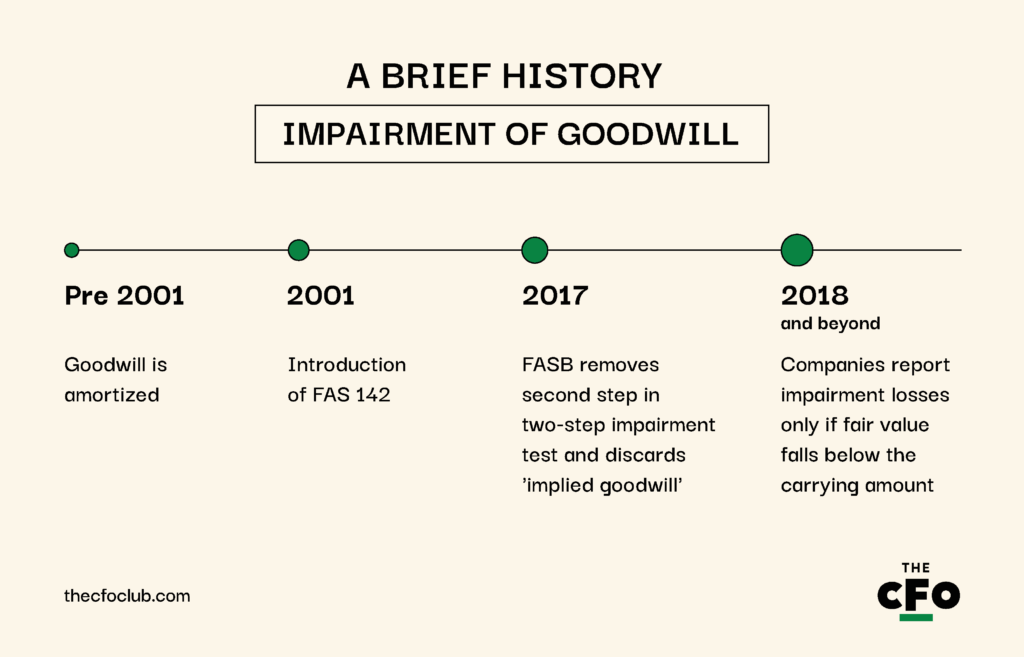

A Brief History: Impairment of Goodwill

Goodwill impairment provisions have evolved significantly over time. Before 2001, companies could amortize goodwill. The problem? Once the goodwill was fully amortized, there was no way to highlight overpriced acquisitions.

All of this changed in June 2001 when FASB introduced FAS 142, which eliminated goodwill amortization and introduced annual impairment testing.

Since then, the goodwill impairment test has been considerably simplified. In 2017, FASB eliminated the second step in the two-step impairment test and discarded the concept of “implied goodwill” through ASC 350-20.

The two-step test included the following steps:

- Step 1: Compare the fair value of the reporting unit and carrying amount. If the fair value exceeds the carrying amount, no loss is recorded. If the fair value is lower than the carrying amount, move to step two.

- Step 2: Compare fair value and implied goodwill. Companies must perform a hypothetical purchase price allocation (PPA) to estimate the implied goodwill as if the reporting unit were acquired at its current fair value. If implied goodwill was lower than recorded goodwill, an impairment loss was recognized for the difference.

Under the new simplified procedure, companies are required to recognize impairment losses only if a reporting unit’s fair value falls below the carrying amount.

An exemption was added later with the Accounting Standards Update (ASU) 2014-02 that allowed private companies and not-for-profit entities to amortize goodwill on a straight-line basis over 10 fiscal years (or a shorter period if they can justify it).

-

Workday Adaptive Planning

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.4 -

Rippling Spend

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.8 -

QuickBooks Online

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4

How to Know When Impairment of Goodwill is Necessary

There are two potential instances during any reporting period when you might realize goodwill impairment is necessary: when a triggering event occurs or when you test for impairment (using the process explained in the previous section).

Let’s look at both of them separately. Here are examples of events that can indicate goodwill impairment:

- Deteriorating Financial Performance: Falling revenue, cash flow, or profitability in the acquired unit suggests goodwill may be impaired.

- Macroeconomic or Industry Shifts: Recessions, regulatory changes, or poor market conditions can lead to goodwill impairment.

- Significant Business Restructuring: If a company divests, reorganizes, or closes a business unit, goodwill allocated to the unit may no longer be justified.

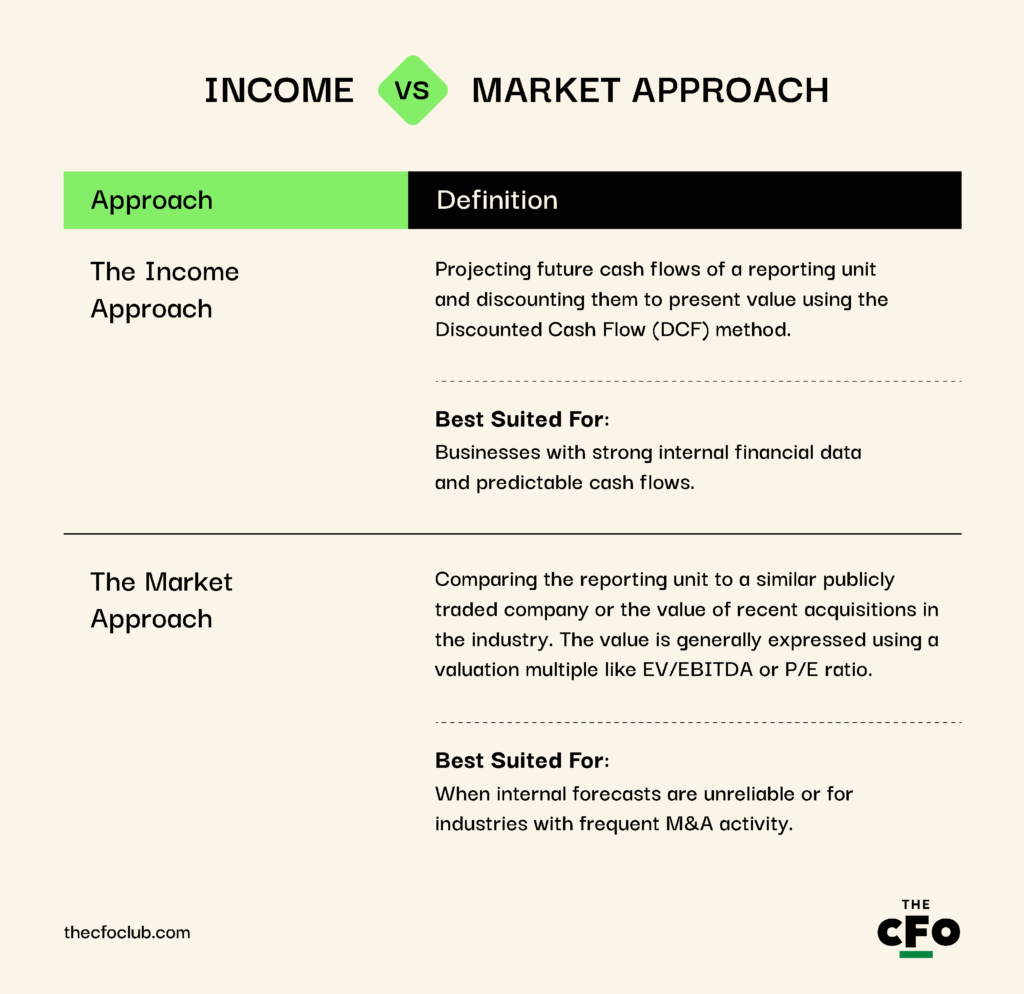

Income vs. Market Approach

The income approach and market approach are methods used to determine a reporting unit’s fair value when testing for goodwill impairment.

GAAP doesn’t prescribe a single valuation method but requires companies to determine a fair value based on the best available evidence, which typically comes from either:

Recording Impairment of Goodwill as a Loss

Once you’ve calculated the reporting unit's fair value and it’s lower than the carrying value, you must record an impairment charge as a non-cash loss on the income statement.

The journal entry for recording the non-cash loss is:

| Account | Debit ($) | Credit ($) |

| Goodwill Impairment Expense A/C | $10,000 | - |

| Goodwill A/C | - | $10,000 |

The goodwill impairment expense is closed to the profit and loss account, which means impairment reduces your net income. However, your cash flow statement remains unaffected since goodwill impairment is a non-cash expense.

Impairment of Goodwill for Small Businesses

Goodwill impairment isn’t a common problem for small businesses because of:

- Lower Acquisition Activity: Most small businesses grow organically. Without acquisitions, there’s no goodwill on the balance sheet and no impairment expense in the income statement.

- Exemptions: Private companies can amortize goodwill over 10 years (or less if they can justify it), reducing the need for annual impairment tests. They’re also exempt from annual impairment tests.

However, if you’re a small business with significant goodwill from acquisitions on your balance sheet, you still need to monitor for events that trigger impairment. The problem? Goodwill analysis is often an added complexity for small businesses.

When I asked Robert Belsky, CEO at Bob’s Bookkeepers, about things he’d change about current goodwill impairment provisions, he agreed that testing for goodwill impairment is often a stretch for small businesses.

For small companies, running a goodwill analysis takes time and becomes more burdensome as the company grows and acquisition complexity increases.

In his opinion, such complexity is unnecessary for small companies because they have little to no incentive to window-dress their financial statements. While the goodwill impairment test is critical for public company reporting, it’s less so for smaller companies whose acquisitions are typically smaller.

Instead, Robert suggested that for these companies, the rules should mirror those for other depreciating or amortizing net assets: write down and capitalize the goodwill, then amortize it.

A Cautionary Example of Impairment of Goodwill

Before I hop into the process of goodwill impairment, I wanted to provide a cautionary example of how goodwill impairment, when not done correctly, can lead to major problems. Let’s look at what happened with General Electric (GE) in 2018.

In 2015, GE acquired Alstom’s power business for $10.6 billion to strengthen its power division. However, by 2018, the global power industry had declined sharply with lower demand for fossil fuel-based energy solutions.

GE’s power division struggled, which compelled the company to reassess the fair value of goodwill for the entire power segment (which included Alstom and units from other deals).

The result? GE took a $22.1 billion impairment charge, as reported in the company’s 10-K—one of the largest in history. This impairment charge effectively erased all the goodwill associated with the Alstom acquisition.

This was a key event that initiated GE’s downfall and led to CEO John Flannery’s removal months later.

Process and Tips for Calculating and Testing Impairment of Goodwill

We discussed the process of testing for impairment earlier in this guide, but let’s dive deeper and look at a detailed breakdown of how impairment testing is performed, as well as a few tips to make the test easier.

Step 1: Identify the Reporting Unit

Goodwill is always tested for a specific reporting unit and never at the entity level. A reporting unit is an operating segment or a component of an operating segment that:

- Has discrete financial accounting information available, and

- Is managed separately for performance evaluation

In a company with multiple reporting units—such as power, aviation, and healthcare divisions in the case of GE—each unit with allocated goodwill must be tested separately.

For example, if you acquire a company that offers cloud services and on-prem software, split both divisions into different reporting units to minimize potential damage from future impairment.

Of course, the split needs to be GAAP-compliant. You can’t break up reporting units just to minimize impairment loss or constantly change the reporting unit structure to manipulate impairment results. When looking to split, make sure that each reporting unit meets the following criteria:

- It earns revenue and incurs expenses

- It’s managed separately and reviewed by the chief operating decision-maker

- It’s discrete enough to generate its own cash flows

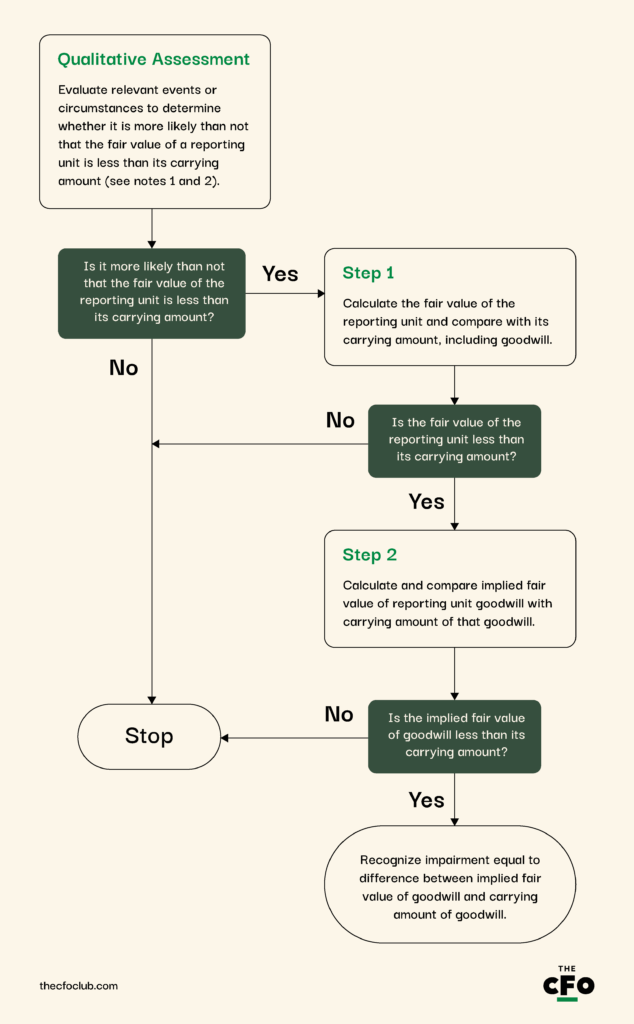

Step 2: Determine If a Qualitative Assessment (“Step Zero”) Is Needed

Once you’ve identified a reporting unit to test, you have the option to take the easier route and perform a qualitative assessment instead of the more extensive quantitative assessment.

ASU 2011-08 gives you the option of a “step zero,” if you will, that allows you to bypass complex fair value calculations in cases where there’s no significant risk of impairment. The update also provides a flowchart that outlines the rest of the process:

A qualitative test involves evaluating macroeconomic, industry, and company-specific factors such as:

- Deterioration in general economic conditions

- Industry-specific downturns

- Declining share price

- Changes in key personnel

- Regulatory or legal challenges

- Negative cash flow trends

If the qualitative assessment suggests that it’s “more likely than not” (more than a 50% chance) that goodwill is impaired, the company must perform a quantitative test explained in step 3. If not, no further testing is needed.

Step 3: Perform the Quantitative Impairment Test

A quantitative test involves measuring the reporting unit's fair value using the income approach, the market approach, or a combination of the two and comparing it to the carrying value.

Suppose your company acquired a small company called Company A five years ago for $100 million. You’re running your annual impairment test, and the DCF model shows the reporting unit’s fair value to be $75 million.

According to your test, goodwill is impaired and needs to be written down by $25 million.

-

Workday Adaptive Planning

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.4 -

Rippling Spend

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4.8 -

QuickBooks Online

Visit WebsiteThis is an aggregated rating for this tool including ratings from Crozdesk users and ratings from other sites.4

Step 4: Record the Goodwill Impairment Loss

Recording impairment is simple. Create a new expense account for goodwill impairment, debit that account, and credit the goodwill account to reduce its value on the balance sheet.

Always Remember...

Even though the impairment charge is recorded as an expense on the income statement, it’s not tax deductible. The IRS only allows a fixed, straight-line deduction for goodwill over 15 years, regardless of whether an impairment occurs. This also means the impairment may affect your deferred tax asset or deferred tax liability balance.

Benefits of Impairment of Goodwill

Goodwill and goodwill impairment may seem abstract, but they’re critical for various reasons. Here are some benefits of goodwill impairment for stakeholders:

- Improves Financial Transparency: Impairment tests force companies to align values with actual economic value. Regular tests ensure that overstated assets don’t mislead investors or analysts and reduce the risk of accounting distortions that could artificially inflate financial health.

- Protects Stakeholders: Impairment signals management is aware of deteriorating business conditions and taking corrective action. That’s why impairment provides valuable insights into a company’s strategic challenges and prompts investors to reassess risk.

- Encourages M&A Discipline: The thought of having to justify an impairment charge reduces the incentive for aggressive deal-making. It forces companies to rethink their acquisition strategies, especially in industries with high goodwill balances.

Disadvantages of Impairment of Goodwill

There are also various downsides to goodwill impairment, such as:

- No Direct Tax Benefit: A goodwill impairment charge doesn’t reduce your taxable income. It just creates a temporary book-tax difference (called deferred tax).

- Negative Market Perception: Large goodwill impairments can sometimes trigger investor panic and cause the stock price to decline. It can damage your company’s reputation, especially if impairment signals failed acquisitions or poor business performance.

Impairment of Goodwill: Additional Resources

We’ve covered quite a bit of ground in this guide, but if you’re looking for more resources, try the following:

| Resource | Why You Need It |

| ASC 350 | ASC 350 is the primary U.S. GAAP standard governing goodwill impairment testing. It covers annual testing requirements, private company election for goodwill amortization, and the one-step impairment test update from 2017. |

| SEC Staff Accounting Bullet (SAB) Topic 5 | The SAB offers SEC staff interpretations on recording and disclosing impairment charges. |

| IAS 36 | IAS 36 is the global counterpart of ASC 350, relevant for multinational companies following IFRS. |

| ASC 820 | This is where you’ll find guidelines for calculating a valid fair value (used in step one of the impairment testing process). |

| AICPA Goodwill Impairment Guide | AICPA offers practical guidance on valuation methods, key assumptions, and industry-specific considerations for impairment testing. |

| Accounting Software | Gives you access to real-time data. The best accounting systems on the market can also build DCF models based on your assumptions. This dramatically reduces the time needed for analysis and helps you focus on making smarter decisions. |

Impairment Impacts Every Financial Statement

Except for cash flow, goodwill impairment impacts all financial statements:

- The impairment charge reduces the net income on your income statement. Remember that goodwill impairment is usually classified as “impairment loss” under operating expenses.

- The lower net income translates to lower retained earnings in the statement of retained earnings

- The impairment charge reduces the balance in the goodwill account that appears on the balance sheet

Put simply, impairment isn’t good news for any part of your financial reporting. That’s exactly what regulators want.

The need to disclose the poor performance of an acquisition forms the basis for introducing the concept of impairment, and that’s why you need to give impairment a thought when closing an acquisition deal.

Ready to compound your abilities as a finance professional? Subscribe to our free newsletter for expert advice, guides, and insights from finance leaders shaping the tech industry.

{kind=link}